It is well known that Retirement is a huge challenge for many South Africans, and that less than 6% of South Africans can retire comfortably by age 65.

Now, increasing consideration is being given to a relatively new “Hybrid approach” because it can benefit by combatting multiple risks at once.

In a recent study published on the South African Journal of Economic Management Sciences (SAJEMS), researchers concluded that instead of choosing either a living or life annuity, a “hybrid-approach” increases the likelihood of a successful retirement for South Africans who withdraw less than 8% from their living annuity, accounting for more than 50% of the population.

So, what is a hybrid approach?

When you retire, you must invest at least two thirds of your compulsory retirement savings into a compulsory annuity. There are two types of post-retirement annuities:

- A Life Annuity: which pays a guaranteed fixed or increasing amount for the remainder of your life.

- A Living Annuity: which is market-linked, and incomes vary due to changes in valuation and annual changes to the income rate.

Most advisors typically select one or the other, however a “hybrid-approach” make use of both annuities to extract the benefits of each and deliver a solution that has a higher probably to success.

Each of these solutions come with their own pros and cons so to understand why this can be a preferable approach we need to unpack the risks and benefits of each, as tabled below:

| Life Annuity | Living Annuity | |

| Longevity Risk | Risk to insurer – income is paid for as long as you live. | Risk to retiree – if capital is exhausted due to high withdrawals or poor returns, income stops. |

| Volatility Risk | Risk to insurer – retiree doesn’t face any income variation. | Risk to retiree – portfolio performance directly affects the sustainability of income. |

| Inflation Risk | Risk to retiree unless structured as escalating or inflation linked income. | Risk to retiree – inflation protection must be built into the investment strategy through inflation linked solutions. |

| Bequest Risk | High risk to retiree – income ceases on death | Low risk to retiree – any remaining capital passes to beneficiaries tax-free within the policy. |

Understanding the risks that the individual retiree faces, based on their personal financial position will usually determine what type of solution that best addresses their requirements. This is a crucial step in your retirement assessment, electing the wrong solution can have detrimental effects.

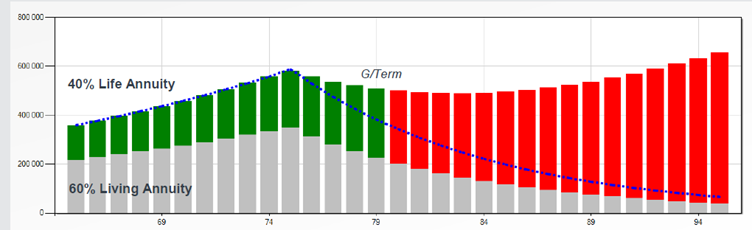

The impact of a hybrid solution is illustrated in this chart from Glacier:

A 40% Life Annuity allocation provides certainty of income, which is increasingly significant in cases where the retiree continues to draw an income well into retirement

How can Finova help?

Finova Capital has always been a strong advocate of segregated portfolios in Living Annuities. Within this structure a fixed allocation to bonds can be held to replicate the yield of a Guaranteed Life annuity, typically with a higher income rate. Although this introduces interest rate risk, it also means the assets remain in your estate and will pass to the appointed beneficiaries.

Importantly, as an independent financial advisor we review all solutions, and they compare this approach to a Guaranteed Life annuity. It all starts with a thorough risk assessment and financial review.

If you would a FREE retirement consultation, Book a meeting with one of Finova’s advisors using this link; “Retirement Consult” and secure the optimal retirement for you and your family.