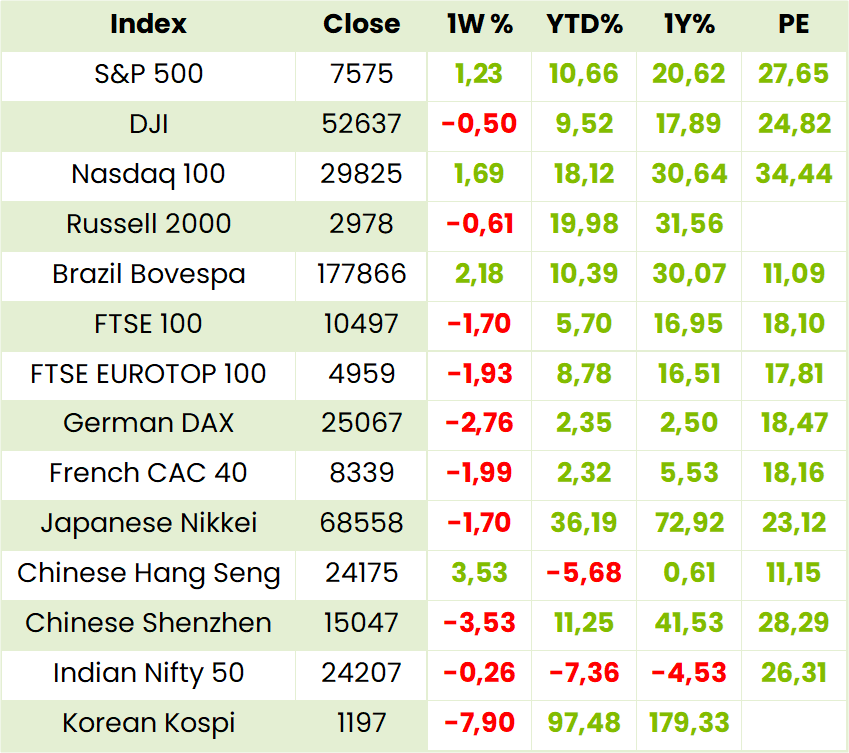

Global Indices

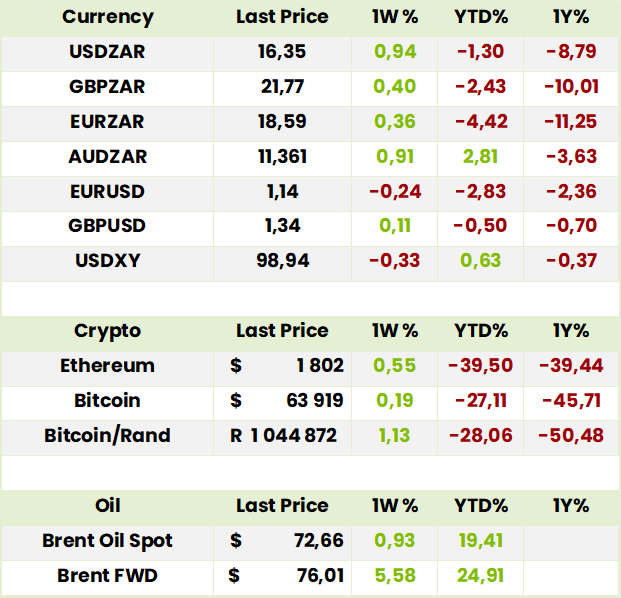

Currencies, Crypto & Commodities

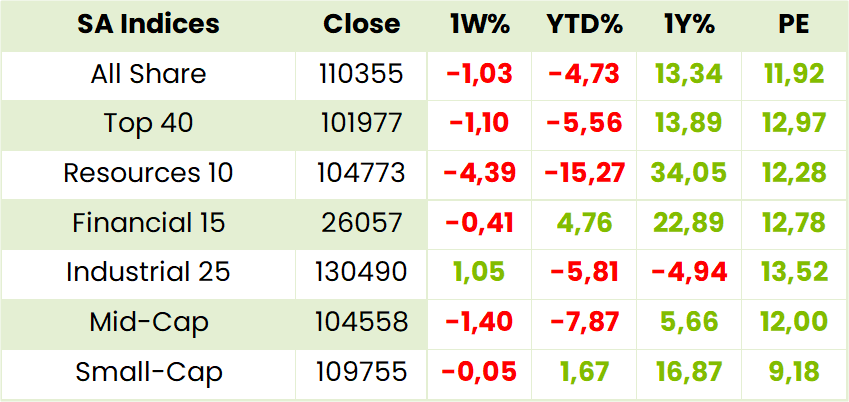

SA Indices

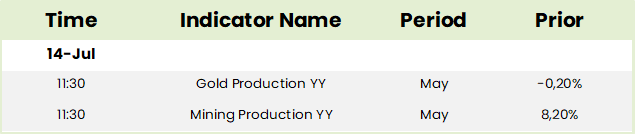

SA Upcoming Indicators & Dividends

*holding in a Finova portfolio

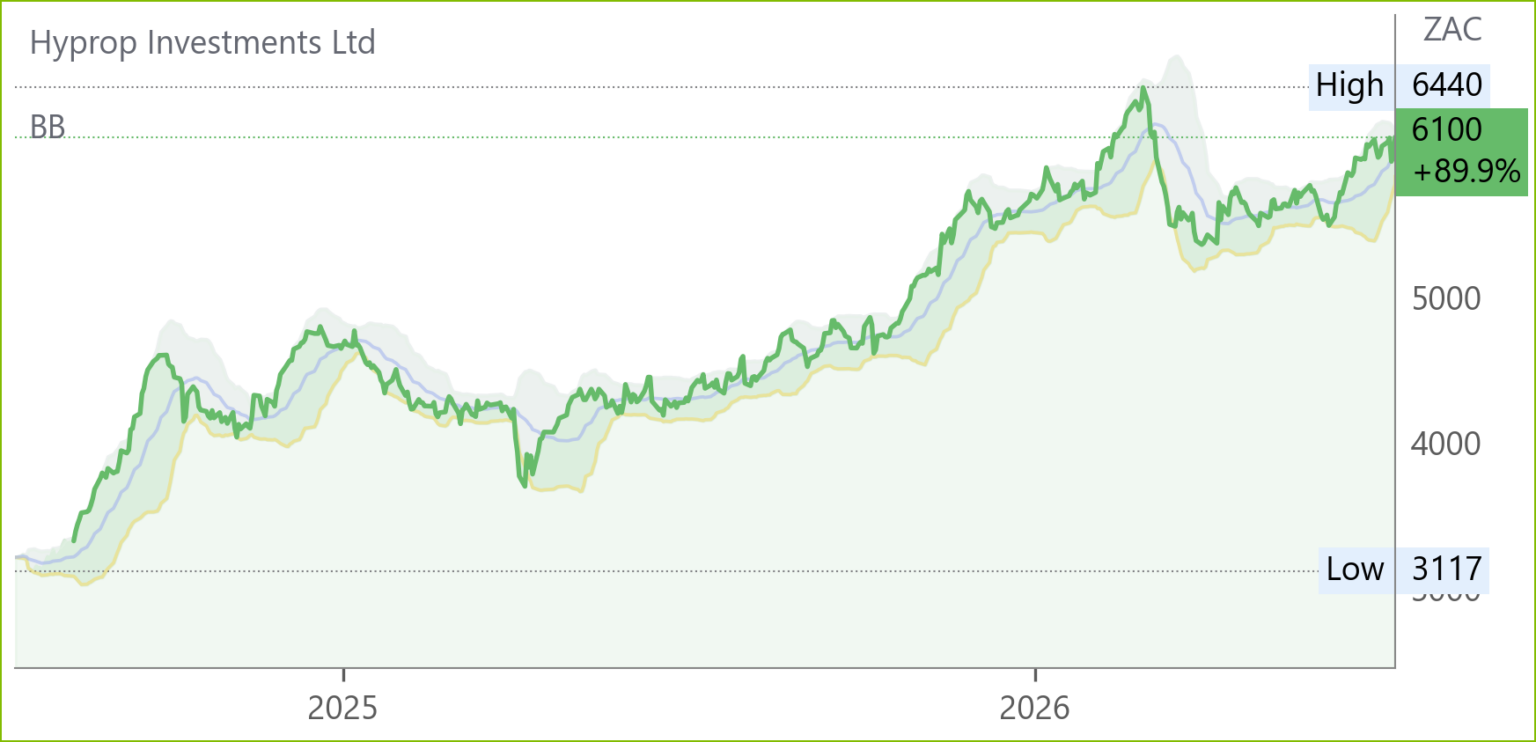

Hyprop (HYP) Capital Raise Update (6100c)

Hyprop has successfully raised over R500m through a bookbuild, strengthening its balance sheet and providing additional liquidity for debt reduction and portfolio optimisation. The raise was well supported, reflecting investor confidence in the REIT’s strategy. Proceeds will be directed towards lowering loan-to-value (LTV) ratios and enhancing financial flexibility.

The capital raise bolsters Hyprop’s ability to manage refinancing risk and positions it to pursue selective growth opportunities. Management emphasised that the transaction supports long-term sustainability of distributions. The REIT continues to focus on stabilising South African retail assets while expanding exposure to Eastern European centres.

Comment: some of these, such as Rosebank Mall, are anything but stable, as thefootfall continues its multiyear growth thanks to the the ongoing and susbstantial increase in the number of affordable housing projects within walking distance not to mention office developments such as the new Valterra HQ.

Balwin (BWN) Buyout and Delisting Update (418c)

Balwin has received a R2.26bn buyout offer from a consortium led by the Public Investment Corporation (PIC) and founder-linked investors, valuing shares at R4.35 cash apiece. The offer represents a 41% premium to the 180-day average price and 35% above the 90-day average. Shareholders holding 63.5% of shares have already backed the deal, which will see Balwin delist from the JSE and A2X if approved.

Balwin’s NAV per share is closer to R10, but management noted that unlocking this value requires years of development and cash collection. CEO Steve Brookes emphasised that private ownership with PIC backing provides “stability and long-term support for the development pipeline” Importantly, management and reinvesting shareholders are staying invested because they believe in the company’s developm…. Analyst Anthony Clark highlighted that the offer gives shareholders a chance to exit at attractive levels, with the share price having more than doubled in 12 months from 180c to current levels.

Comment: while offeree shareholders would benefit on a 12 month basis, the takeout also plays to the theme of high concentration of the JSE in the Top 40 as a result, inter alia, of sub-par economic growth and the 2022 decision to lift the institutional limit from 30% to 45%. This has been strongly criticised but, following an IMF assessment commissioned by the National Treasury, will not be reversed. Instead, as Stuart Theobald has pointed out, the answer is to put policy energy into generating the pipeline of profitable businesses and bankable projects in infrastructure, energy,and logistics, that would make domestic investment the rational choice even when global alternatives are available. In addition it would help to allow investment of equities in tax free saving accounts as well as make it easier for long term pension capital to hold illiquid assets. Meanwhile, Balwin minority shareholders who accept managment’s rationale for not waiting to unlock the 54% discount bewteen 435c and NAV of 977c can consider the even bigger discount on peer Calgro’s 74% discount to 1646c NAV.

Reinet Investments (RNI) (44614c)

Valuation opportunity: Shares have sold off ~25% from May highs, now trading at ~30% discount to NAV, which is largely cash — minimal subjectivity in valuation.

Buyback catalyst: Management has launched a buyback program of up to EUR 500 million, signaling confidence and potential support for the share price.

Permanent capital advantage: Provides Johann Rupert with a permanent capital vehicle — effectively an insurance policy against macro uncertainty.

Optionality and patience: Rupert is effectively being paid (via reduced fees) to sit on cash and wait for the right opportunity, rather than being forced into suboptimal investments.

Institutional mispricing: Market participants often underestimate the strategic value of permanent capital structures, leading to capitulation and undervaluation.

Restructuring debate: While bulls argue for portfolio consolidation or collapse to unlock short-term upside, such moves do little for Rupert’s broader portfolio strategy — explaining past market disappointment.

Risk/reward skew: Current discount offers asymmetric upside if buybacks or eventual deployment of capital are well-timed, with limited downside given cash-heavy NAV.

Global Equity

Samsung Electronics (005930.KS) Analyst Rating Update (285000KW)

HSBC has reaffirmed its Buy rating on Samsung Electronics, maintaining a price target of ₩450,000. The investment bank cited strong momentum in semiconductor demand and resilient smartphone sales as key drivers. The update reflects confidence in Samsung’s ability to sustain earnings growth despite global macroeconomic uncertainties. Analysts highlighted ongoing efficiency improvements and strategic positioning in memory chips as supportive of long-term valuation.

Tencent (0700.HK) Q1 ’26 Results(460.20HKD)

HEPS: RMB7.364 (+12% YoY)

EPS: RMB7.364 (+12% YoY)

Operating Profit: RMB75.6bn (+9% YoY; excl. AI RMB84.4bn, +17%)

Revenue: RMB196.5bn (+9% YoY)

Gross Profit: RMB111.3bn (+11% YoY)

EBITDA: RMB89.6bn (+46% margin)

Revenue grew 9% YoY, supported by evergreen games and cloud services. Gross margin improved to 57%, while free cash flow surged 20% to RMB56.7bn. Net cash rose 63% YoY to RMB146.9bn, strengthening balance sheet resilience. AI initiatives, including Hunyuan 3 and agentic AI tools, gained traction, though monetisation is expected to be gradual. Management flagged substantial AI-related CapEx in H2 ’26 as China-designed ASICs become available. Strong cash flow from core businesses underpins expansion.

The company has sold a $1.5 billion stake in Kuaishou, cutting its holding below 8% as it accelerates its pivot toward artificial intelligence investments. The divestment reflects Tencent’s strategy to streamline non-core assets and redeploy capital into AI-driven growth. Analysts note Tencent looks undervalued on an absolute basis, and if the portfolio unwind continues some estimate that the stock could rise 30%.

Snippets

Capitec (CPI) announced the disposal of its subsidiary, Capitec Rental Finance (CRF), to Sasfin Capital for R201 million. CRF, acquired via Mercantile Bank in 2019, is profitable but non-core. Capitec will extend a R1.6 billion secured credit facility to support CRF’s receivables under Sasfin. The deal awaits regulatory approval and standard conditions.

Sappi (SAP) has revised its third‑quarter FY2026 outlook. Initially expecting weaker results, the company now forecasts Adjusted EBITDA broadly in line with Q2, thanks to stronger‑than‑anticipated North American performance and the ramp‑up of Somerset Mill PM2 sales. This marks an improvement from May’s guidance. Results will be released on 6 August 2026