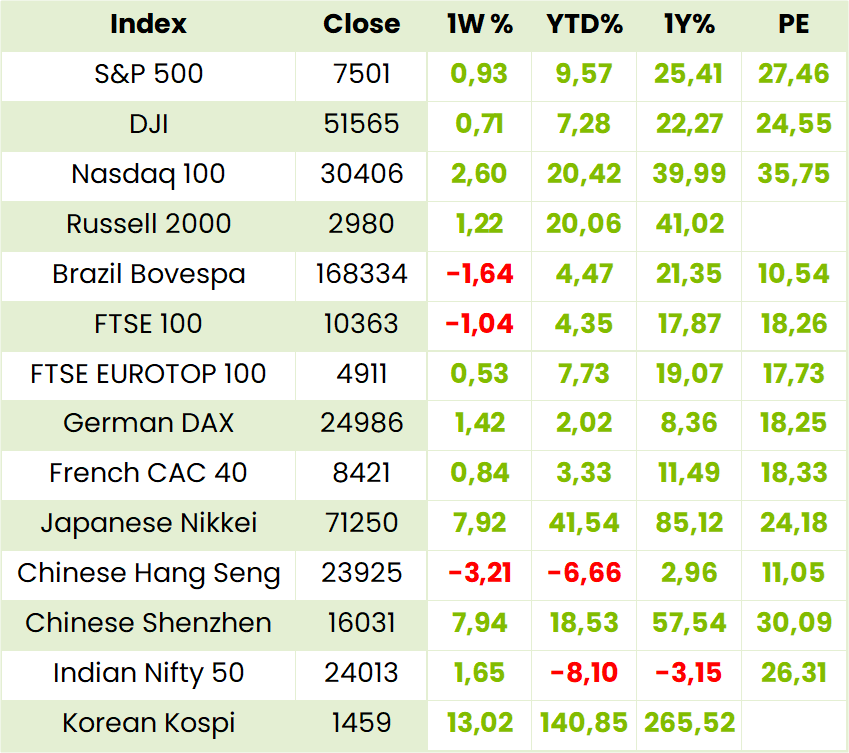

Global Indices

Currencies, Crypto & Commodities

SA Indices

SA Upcoming Indicators & Dividends

*holding in a Finova portfolio

Premier (PMR) Financial Results for FY26 (19050c)

HEPS: 1204c (+27.7% from FY25)

EPS: 1192c (+27.4% from FY25)

Operating Profit: R2.4bn (+23.2% from FY25)

Revenue: R21.2bn (+6.6% from FY25)

EBITDA: R2.8bn (+18.2% from FY25)

Dividend: 341c per share (final dividend 182c declared)

Premier delivered strong FY26 growth, with headline earnings per share (HEPS), earnings per share (EPS), operating profit and EBITDA all increasing ahead of revenue. Performance was supported by growth in Millbake and Groceries & International, including the benefit of the RFG acquisition. Margins improved as lower maize input costs supported volumes, while the commissioning of the Aeroton bakery strengthened inland bread capacity. The balance sheet also improved, with net debt reduced and leverage remaining low. Management’s outlook focuses on integrating RFG, extracting synergies and driving further efficiency gains, alongside modest price increases to offset rising input costs.

CEO JJ Gertenbach noted: “Investment in our infrastructure is translating into measurable benefits supported by our core principles which include a relentless focus on quality, service delivery and agile execution.”

Comment: the RFG Holdings acquisition was completed at a value of R6.5 billion, as the Premier share price increased 12% from the reference price of R154.00 per share at announcement to R172.78 at implementation. In anticipation of a nearly full year’s contribution from RFG (its results were only consolidated from 11 March 2026) and the benefits of the Aeroton commissioning, the share price gained a further 8%. Management quite rightly, however, warns that a Super El Nino (worst ever) is now forecast from November which in our view could (more than?) reverse the 31% decline in the white maize spot price since March 2025. At best a Hold for now.

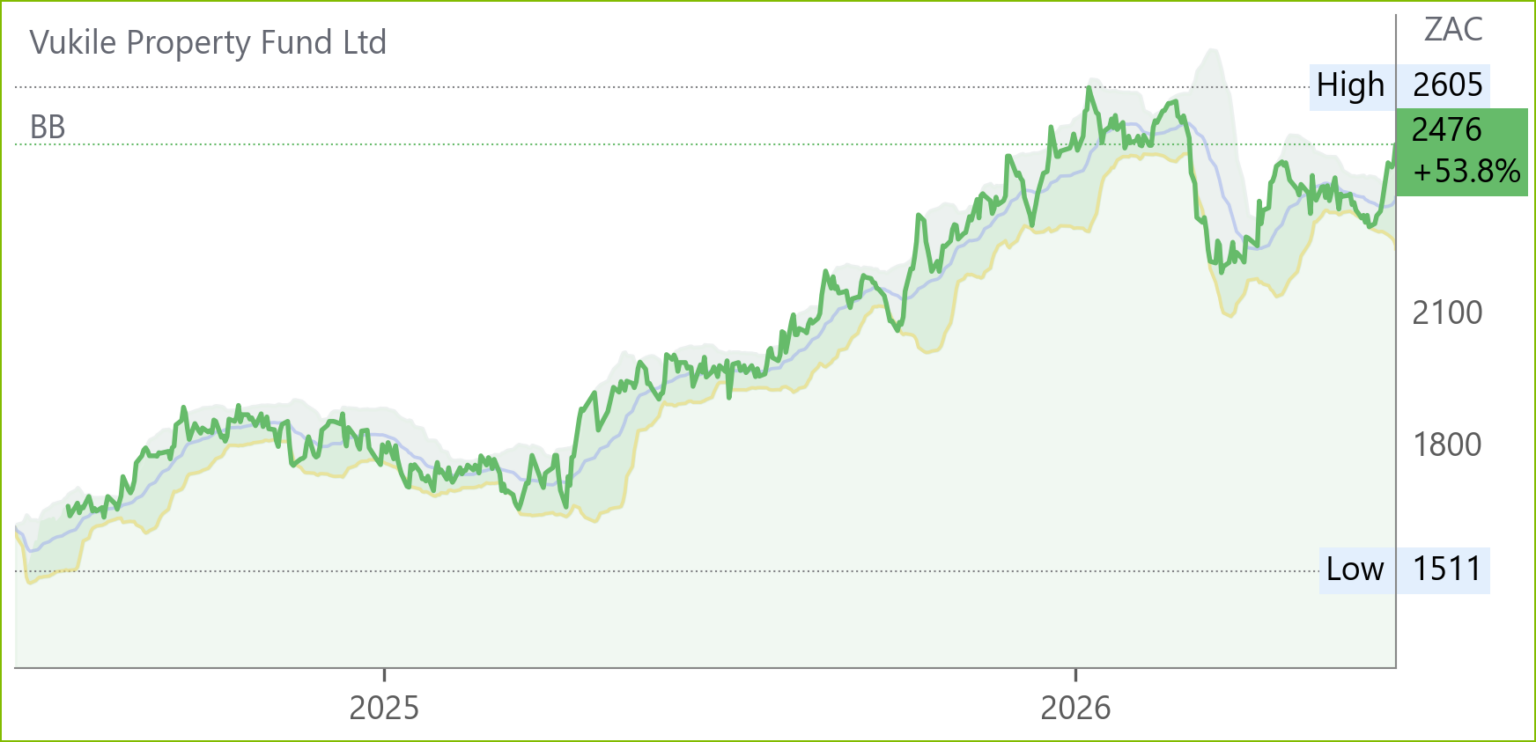

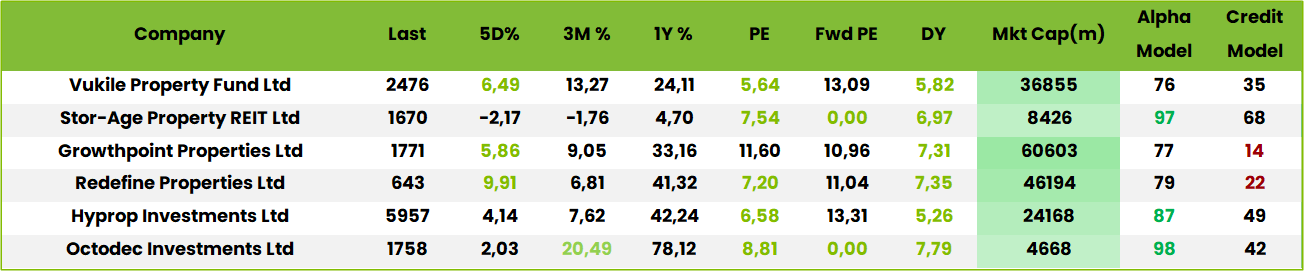

Vukile (VKE) Financial Results for FY26 (2476c)

HEPS: 180c (+13.2% from FY25)

EPS: 442c (+63.2% from FY25)

Operating Profit: R3.6bn (+9.8% from FY25)

Revenue: R5.8bn (+32.8% from FY25)

Dividend: 144c per share (final dividend 83.8c declared)

LTV: 38.4% (down from 39.5% FY25)

NAV: R25.03 per share (+11.8% from FY25)

Vukile exceeded FY26 guidance, with funds from operations (FFO) and dividends both up 9.3%. EPS jumped 63% on full-year Castellana contributions and property valuation gains, while revenue rose 33% due to acquisitions. Liquidity improved materially, supported by strong cash reserves, undrawn facilities and an oversubscribed equity raise. Portfolio rotation strengthened its Iberian position and increased exposure to South Africa’s township and rural retail segments. The group expanded into Italy after year-end, adding to its growing European footprint, which now accounts for nearly 70% of total assets. Management guides FY27 FFO growth of 8–10% and dividend growth of 10–12%.

Comment: strategic capital allocation and asset rotation and, of course , shopping centre management, are what Vukile is good at if not excels in. It seems almost as though management is saying that, having cleaned up in Iberia, it is moving in on Italy. Similar considerations apply to its South African township and rural retail operations. There is no reason to believe that management won’t have similar success in Italy. On a FDY of 6.6% there is no reason why it cannot be added to portfolios for steady income growth and geographic diversification.

Stor-Age (SSS) Financial Results for FY26 (1670c)

HEPS: 117.11c (+16.0% from FY25)

EPS: 227.90c (−22.7% from FY25)

Revenue: R1.39bn (+5.4% from FY25)

Dividend: 116.36c per share (final dividend 56.62c declared)

LTV: 26.7% (down from 27.5% FY25)

NAV: 1792.68c per share (+3.9% from FY25)

Stor-Age delivered a resilient FY26 performance, with headline earnings per share (HEPS) up 16.0% despite a decline in earnings per share (EPS) as prior-year valuation gains were not repeated. Revenue increased 5.4%, supported by stronger South African rental income and growth in the joint venture portfolio, while occupancy remained healthy across both markets. The group continued to expand through acquisitions and development projects in South Africa and the UK. A R500m equity raise at a premium to net asset value (NAV) further strengthened the balance sheet. Management guides 5% growth in distributable income per share for FY27, while maintaining a 90% payout ratio.

Chairman GA Blackshaw emphasised: “FY26 demonstrated the strength and resilience of our operating model, with high-quality assets and disciplined capital allocation positioning us for long-term value creation.”

Comment: the market was understandably unimpressed by the 5.1% growth in DPS as well as the lagging performance of the UK portfolio where rental income increased by 1.1%, occupancy was a low 81.6% and net property income fell 0.8%. In SA, on the other hand, rental income increased 10.5%, net property operating income rose 11.1%, while occupancy was a much higher 93.4%. It seems the “long term value creation” will take longer than some of its peers.

Brait (BAT) Financial Results for FY26 (216c)

HEPS: 34c (+47.8% from FY25)

EPS: 34c (+47.8% from FY25)

EBITDA: Virgin Active +37% (£110m), Premier +18% (R2.8bn), New Look >100% (£37m)

NAV: 327c per share (+7% from FY25)

Debt reduced from R7bn in Mar ’20 to R1.7bn, aided by Premier monetisation (R1.8bn proceeds). Virgin Active raised £175m to cut debt, lowering Net Debt/EBITDA to 2.0x and saving £21.5m in annual interest. Premier delivered R21.2bn revenue (+7%) and EBITDA margin of 13.1%, supported by Aeroton bakery and RFG integration. New Look achieved EBITDA of £37m, boosted by digital transformation and loyalty programme scaling to 1m members.

Outlook focuses on optimising Virgin Active for listing, completing New Look disposal, and unbundling remaining assets. A R2.5bn rights offer at R1.51/share (25% discount to TERP) will fund bond redemption and Virgin Active capital raise.

Comment: despite the three key holdings improving it is no wonder former CEO Antonie de Beer left for Reunert after the watching the paint dry exercise as Brait reduced debt from R7bn in 2020. Current shareholders should follow their rights to avoid dilution: others can wait and see.

Trading Statements & Updates

Prosus (PRX)* Trading Statement FY26 (73280c)

HEPS: 258 USc (↑6.7%–15.7% from FY25)

EPS: 519 USc (↓2.6%–6.4% from FY25)

Revenue: US$7.3bn (↑strong growth)

EBITDA: US$1.1bn (Ecosystem, ↑profitability)

Core headline earnings per share rose 19%–28%, outpacing headline earnings due to exclusion of Tencent fair value losses. EPS declined modestly, impacted by fewer Tencent share sales and higher unrealised FX losses. All ecosystems are now profitable, with free cash flow (ex-Tencent) growing. Prosus has completed its transformation into an AI-driven lifestyle operator across LatAm, Europe and India. Outlook highlights continued profitability and expansion of consolidated businesses and equity-accounted investments, notably Tencent. Results due 29 Jun ‘26.

Naspers (NPN)* Trading Statement FY26 (82884c)

HEPS: 306 USc (↑8.3%–15.3% from FY25)

EPS: 620 USc (↓1.3%–↑5.7% from FY25)

Revenue: US$7.3bn (↑strong growth via Prosus)

EBITDA: US$1.1bn (Ecosystem, ↑profitability)

Core headline earnings per share rose 20.8%–27.8%, outpacing headline earnings due to exclusion of Tencent fair value losses. EPS growth was muted, reflecting fewer Tencent share sales and higher unrealised FX losses on euro bonds. All ecosystems are profitable, with free cash flow (ex-Tencent) expanding. Naspers has completed its transformation into an AI-driven lifestyle operator across LatAm, Europe and India. Outlook highlights sustained profitability and growth from consolidated businesses and equity-accounted investments, notably Tencent. Results due 29 Jun ‘26.

BHP* (BHG) Infrastructure Monetisation Update (68900c)

Asset rotation: Potential US$1.5bn Chilean power transmission sale, lifting identified monetisation to c.US$7.8bn of BHP’s up to US$10bn target.

Press reports indicate BHP is preparing to sell US$1.5bn of Chilean power transmission lines, extending its infrastructure and non-core asset monetisation programme. Prior transactions include a US$2bn Western Australia power network agreement and a US$4.3bn Antamina silver stream. Capital demands remain elevated, with capex guided at US$11bn in FY26 and FY27, and US$10bn medium term, as Chilean copper, Vicuña and Jansen potash require investment. Net debt was US$14.7bn at H1 FY26, against a revised US$10–20bn target. Monetisation proceeds should support capex, preserve balance sheet flexibility and help maintain the minimum 50% dividend payout policy, although future infrastructure access costs may rise.

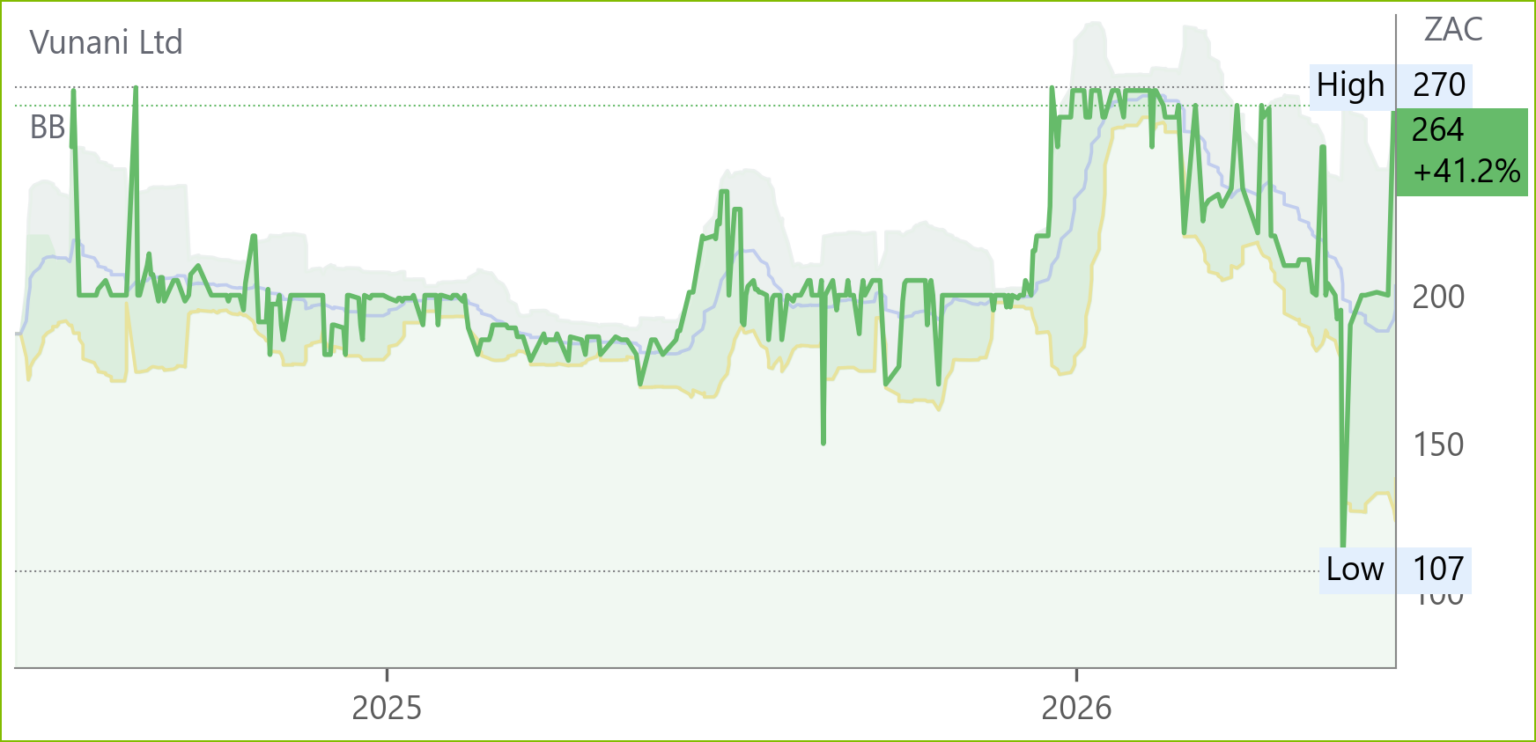

Vunani (VUN) Trading Statement FY26 (264c)

HEPS: 10.9–11.5c (>100% from -2.8c)

EPS: 5.3–6.7c (>100% from -7.1c)

HEPS and EPS reflect a strong turnaround from prior losses, signalling improved profitability across operations. Management highlights resilience in core businesses and expects momentum to continue into FY27. Results due 23 Jun ’26.

Stadio (SDO) Business Update (1214c)

Student numbers grew 9% to 55 854 by mid-Jun ’26, with distance learning at 47 750 (+8%) and contact learning at 8 104 (+15%). Durbanville campus exceeded 1 300 students and Centurion surpassed 2 300, while Milpark B2B lagged due to Namibia’s free higher education policy. Management confirmed delivery of its prelisting promise of 56 000 students in 2026.

2026 is designated the “Year of Investment”, with two new campuses, 18 new qualifications including Engineering, and continued investment in AI, technology and academic capacity. Shareholder value preservation included repurchasing 7.4m shares worth R81.7m, all cancelled. CEO Chris Vorster reaffirmed ambitions to reach 80 000 students by 2030.

Sephaku (SEP) Trading Statement FY26 (200c)

HEPS: 37.0–38.5c (↑17–22% from 31.52c)

EPS: 39.5–42.0c (↑25–33% from 31.57c)

Revenue: Métier ↑ strongly; Sephaku Cement ↓4%

EBITDA: Sephaku Cement ↓9%

Métier Mixed Concrete delivered robust revenue and profit growth, offsetting weaker performance at Sephaku Cement, which faced deteriorating economic conditions and industry challenges. Cement operations remained resilient in maintaining market share despite pressure on margins. Outlook highlights continued focus on shareholder value through cement and ready-mix concrete production in Southern Africa. Results due 30 Jun ’26.

Marshall Monteagle (MMP) Trading Statement FY26 (2889c)

HEPS: US$25.6c (↑1064% from US$2.2c)

EPS: US$26.2c (↑2520% from US$1.0c)

Profits surged on realised gains and fair value increases in the equity portfolio, supported by favourable currency movements. Results due 26 Jun ’26.

Snippets

Standard Bank (SBK) is planning a major expansion in Kenya, aiming to become the country’s largest lender by 2030 through acquisitions and aggressive capital deployment. Kenya’s role as East Africa’s financial hub, supported by infrastructure investment, digital adoption and regional trade, makes it a prime target. CEO Joshua Oigara stressed that dominance in Kenya equates to dominance in East Africa. However, IMF warnings about debt burdens, currency volatility and geopolitical risks highlight challenges. Rivals like Nedbank and Equity Group are also pursuing cross-border deals.

Afrimat (AFT) secured a legal victory as the North Gauteng High Court dismissed Lungile Mlotshwa’s bid to appeal the transfer of a mining right acquired in May ’25. The ruling affirms Afrimat’s entitlement, with Demaneng mine nearing closure by end-’26 or early ’27. Afrimat holds an 870,000-ton allocation expiring Mar ’27, strengthening its iron ore operations despite looming energy cost pressures.

Reinet (RNI) has lifted its closed period after deciding not to pursue a major investment opportunity, enabling the restart of its share buyback programme. The company plans to repurchase up to €500m of ordinary shares, capped at 16.5m shares, through successive programmes until the 2027 AGM. The initial tranche will cover €75m, limited to 2.5m shares, running from 22 Jun ’26 to 19 Aug ’26. Buybacks will be executed on the JSE by an intermediary, within shareholder-approved limits, including a maximum repurchase price of 110% of the five-day weighted average. The Rupert family has confirmed it will not sell shares during the programme. Outlook emphasises returning value to shareholders and potential use of repurchased shares for acquisitions.