Finova Investor Digest

Global Indices, Currencies, Crypto & Commodities

Global Indices 1 year to Date

SA Indices

SA Upcoming Indicators & Dividends

SA Equity

Optasia (OPA) Initiation Note (2100c)

Revenue: FY25E $261m → FY26E $338m (+29%)

EBITDA: FY25E $99m → FY26E $132m (+33%)

Explanation: Revenue and EBITDA growth >90% in FY25E H1, with forecast CAGR of 28% and 25% (FY22A–FY25E). FY26E earnings momentum expected >40%, supported by FX tailwinds and new deployments.

Founded in 2012, Optasia is a unique AI-powered fintech platform monetising the underbanked across 38 emerging markets, serving >121m monthly active users. Growth is driven by micro-loans and airtime credit solutions via MNO partners, with FY25E revenue forecast at $261m and EBITDA at $99m. Expansion into new verticals and geographies underpins long-term growth prospects, while FX tailwinds support FY26E earnings momentum above 40%. Risks include regulatory changes and potential competition, though Optasia retains a strong first-mover advantage.

Comment: based on the FNB comment on the FPE at the time of listing in October the FPE at 2118c would be 21.8x. Given the FY 22-25 CAGR of 28% and the FY26E earnings momentum of >40% the stock remains very much a BUY.

Operating Updates & Trading Statements

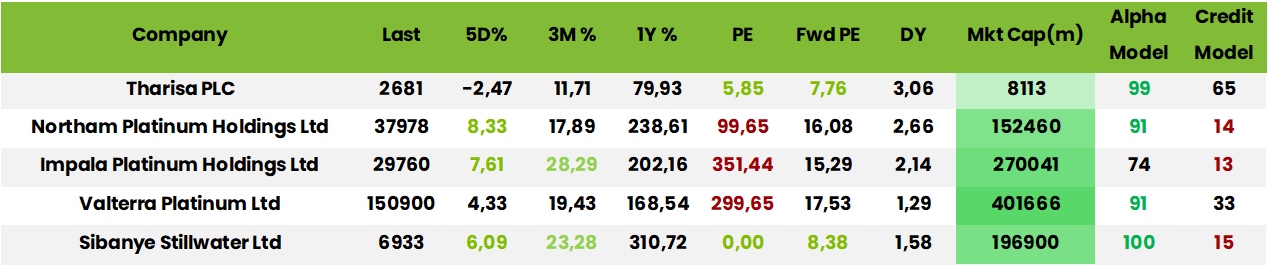

Tharisa (THA) Production Report Q1 FY09/26 (2681c)

PGM recoveries rose to 78.8% (Q1 FY25: 61.7%) and chrome recoveries to 70.3% (Q1 FY25: 65.7%). PGM prices averaged US$2 208/oz, up from US$1 615, while chrome concentrate averaged US$276/t. Net cash stood at US$47m (Sep ’25: US$68.6m) after debt reduction. Safety performance was strong, with LTIFR at 0.02 at Tharisa Minerals and 0.00 at Karo Platinum. Underground development advanced, supporting operational flexibility, while Karo’s progress aligned with capital availability. “We remain constructive on the PGM price outlook and expect current price levels, and potentially higher levels, to persist in the months ahead.” – Phoevos Pouroulis, CEO. Guidance for FY26: 145–165 koz PGMs and 1.50–1.65 Mt chrome concentrates.

Comment: FY09/25 heps of USD27.5c (ZAR 497.5c) puts the stock on a PE of 5.4x. At the results presentation on 1 December the CEO Phoevos Pouroulis commented that on a valuation on spot basis the stock was at a 4.4x PE whereas its peers were on multiples three times higher. One of the reasons is that PGM production declined from 138.3koz in FY22 to 179.2 in FY25. Another is that the company plans $547m capex in SA over 10years as it transitions to underground mining which will make for a 50 year LOM. In Zimbabwe its Karo project, also long life, expects first production in 1Q 27 and will have been funded with equity of $178m and $240m via debt. By 2033 combined production will have risen from c.170koz pgms and 1.7mt chrome concentrate in FY25 to c. 200koz and c. 2mt respectively. As is often the case with companies embarking on substantial capex, however, market recognition may lag valuation until closer to fruition.

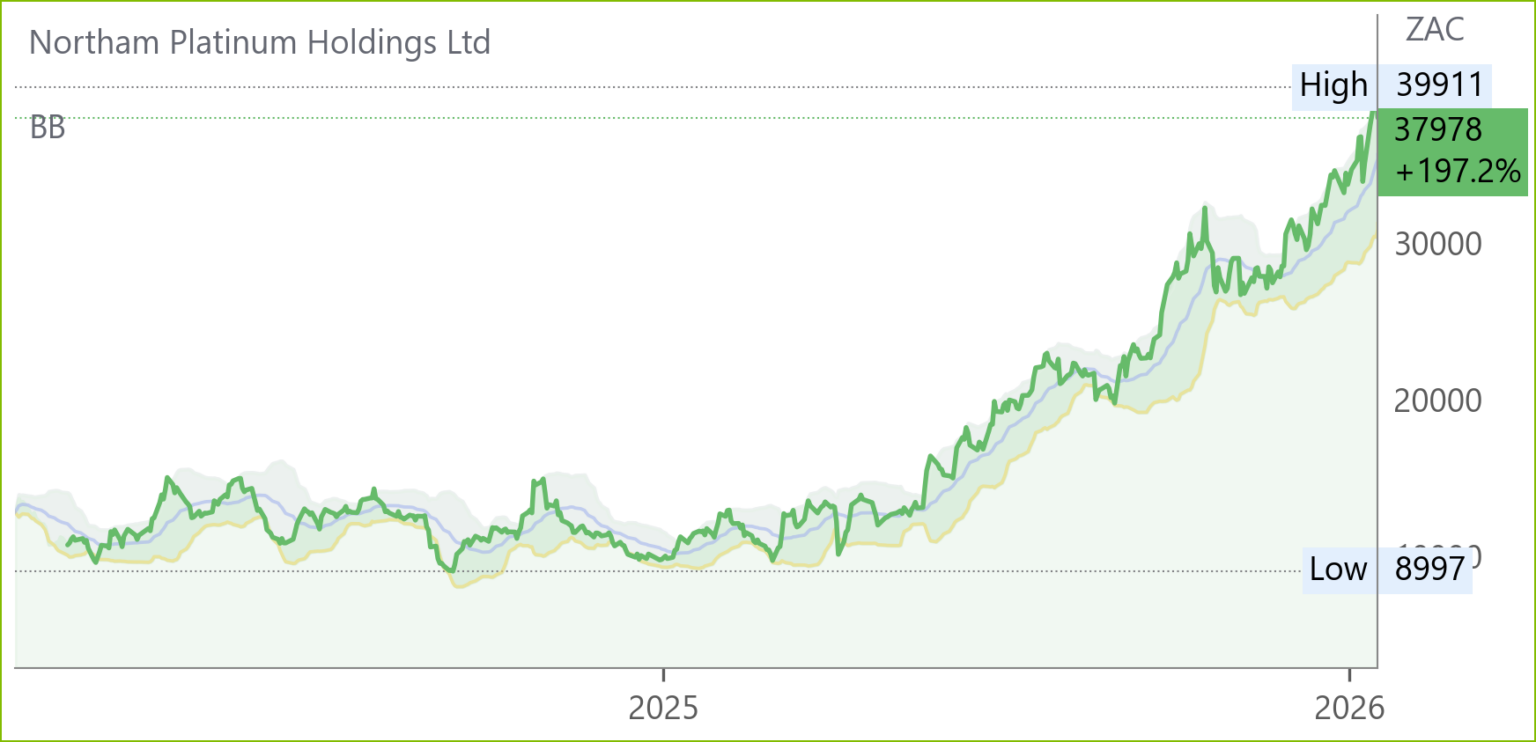

Northam (NPH) Voluntary Production Update for 6M Dec ‘25 (37978c)

PGM output rose 3.7% to 467 818 oz 4E, with Zondereinde up 3.1%, Booysendal 1.7%, and Eland 19.6%. Chrome concentrate production increase $247 med 14.8% to 822 759 tonnes, driven by a 44.7% surge at Eland. Third‑party refined PGMs climbed 39.7% to 83 448 oz 4E. Operational highlights include logistics improvements at Zondereinde, efficiency gains at Booysendal, and ramp‑up progress at Eland. Shaft developments at Zondereinde and ventilation upgrades at Eland underpin future productivity. Metallurgical upgrades, including a new slag concentrator, are delivering benefits. Results due 3 Sep ‘26.

Richemont (CFR) Q3 Trading Update to Dec 25 (331300c)

Revenue rose 11% at constant rates, driven by Jewellery Maisons (+14%) and strong regional growth in Americas (+14%), Japan (+17%), and Middle East & Africa (+20%). Retail channel led with +12% growth.

Sales momentum continued with €6.4bn Q3 revenue, supported by double-digit growth in key regions and strong jewellery demand. Specialist Watchmakers advanced 7%, while Fashion & Accessories grew modestly. A robust net cash position of €7.6bn underpins resilience despite currency weakness and rising material costs. Management emphasised ongoing investment to nurture Maisons’ growth in a complex macroeconomic environment. “Richemont remains committed to long-term shareholder value creation through consistent investment and disciplined execution.” — Johann Rupert, Chair

Aspen Pharmaceuticals (APN) Divestment of APAC (12099c)

Divestment of 100% of Aspen APAC (excl. China).

Consideration: AUD 2.37bn (≈ ZAR 26.5bn); no deferrals or provisions.

Valuation: 11× EV / Normalised EBITDA (FY2025), above Aspen’s Group trading multiple (~7–8×).

APAC contribution: 18% of Group revenue and 26% of Group EBITDA (FY2025).

Use of proceeds: Primarily debt reduction to lower financing costs and simplify the lender base.

Timing: Shareholder approval required; completion targeted for May 2026.

Management emphasised that the divestment reflects portfolio focus rather than distress. Australia is one of the world’s largest generic markets, but management noted sustained margin pressure, particularly as the portfolio shifted toward OTC over recent years. Group executive Stephen Saad commented that management in the APAC region had achieved most of what was strategically possible, concluding that the offer represented a compelling realisation of value, consistent with Aspen’s strategy to unlock sum-of-the-parts value that is not fully reflected in the Group’s market valuation.

The transaction materially improves balance sheet flexibility, with proceeds used to deleverage, reduce finance costs, and simplify lender base. This enables sharper execution on Aspen’s core growth drivers: scaling Commercial Pharmaceuticals in emerging markets, accelerating GLP-1 opportunities (including strong Mounjaro momentum in South Africa and generic GLP-1 plans), reshaping China into a profitable and sustainable model. Management also highlighted a disciplined shift toward free cash flow generation, and reducing capex to match depreciation by end of FY27/28.

Snippets

Maputo Port, in which Grindrod (GND) holds a 24.7% indirect stake, achieved a record 32.0m tonnes handled in 2025, underscoring strong operational momentum. The milestone reflects infrastructure investment and efficiency gains, positioning Grindrod for sustained growth in regional logistics. Continued expansion supports shareholder value through increased cargo throughput and strategic port development.

Aveng (AEG) announced the retirement of Group CEO Scott Cummins effective 30 January 2026. David Simpson, an experienced executive in engineering and infrastructure sectors, is appointed Interim CEO to drive performance, growth, and resolve disputes. Cummins will support Simpson during transition. External advisors are assisting in selecting a permanent CEO.

Hyprop (HYP) announced that the disposal of a 50% stake in Hyde Park Corner to Millennium Equity Partners has terminated due to unmet conditions precedent, cancelling the related option transaction. Despite this, Hyde Park Corner’s performance is improving with reduced vacancies, new tenants like Checkers Fresh-X and Al Capone, and an integrated battery and solar PV project boosting future operating income.

Labat Africa (LAB) advises shareholders that it remains in advanced talks with an artificial intelligence and technology company active in the SADC region. The cautionary announcement of 22 December 2025 is renewed, as any resulting transaction could materially impact the company’s share price.