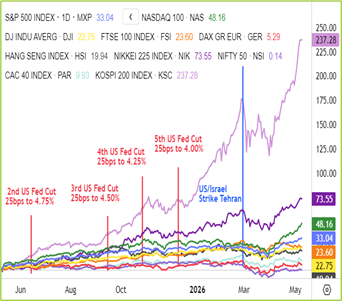

Global Indices

Currencies, Crypto & Commodities

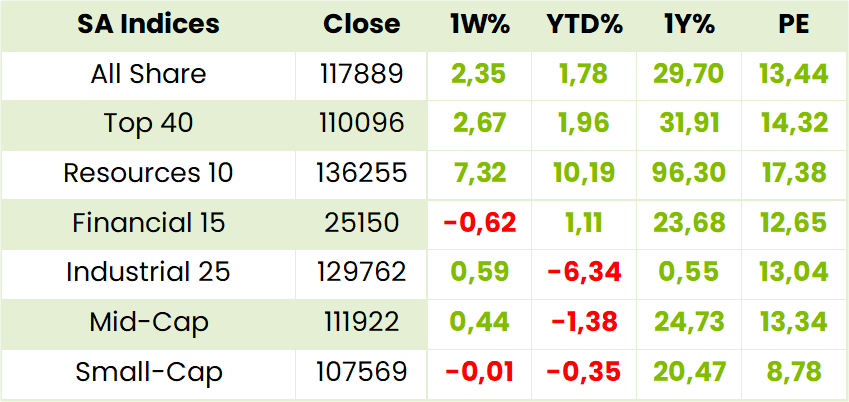

SA Indices

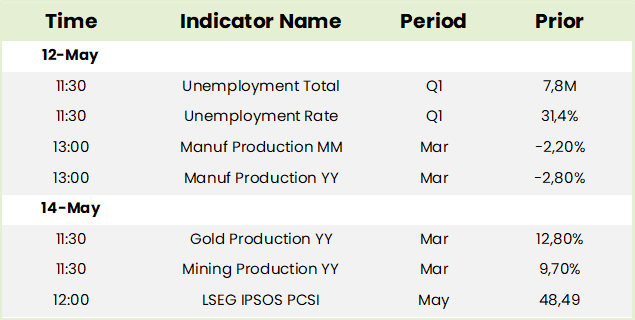

SA Upcoming Indicators & Dividends

Global Equity

*Constituent of Finova Global and GRANOLAS portfolio

Novo Nordisk (NOVOb.CO; NVO) Q1 Results Mar 26 (290.30 DKK; $46.07)

HEPS/EPS: US$1.03 (+18% YoY). Operating profit: DKK 59.6bn (+65% YoY). Revenue: DKK 96.8bn (+32% YoY; vs consensus DKK 71.3bn). Gross margin: 80.6% (vs 83.5% FY25).

Forward P/E: ~13–14x on consensus FY26 EPS (vs ~20x a year ago), below sector median (~17x), reflecting stronger earnings growth expectations led by obesity care.

Dividend Sustainability & Guidance: Dividend paid: US$11.11/share in Q1 ’26 (~3.8% yield). Progressive dividend policy reaffirmed; strong cash generation and net debt/EBITDA <0.2x support dividends and buybacks alongside R&D/international expansion, despite U.S. diabetes pricing pressure.

GLP 1 Contribution: GLP 1 therapies (Wegovy, Ozempic) contributed ~70% of Q1 turnover. Obesity care delivered ~45% of operating profit; Wegovy pill exceeded 1.3m prescriptions in Q1 (fastest GLP 1 launch in U.S. history), supporting raised FY26 guidance and offsetting diabetes margin compression.

Obesity care sales grew +22% with Wegovy pill at 1.3m prescriptions; international ops rose 6%, offsetting an 11% decline in U.S. diabetes sales from pricing pressure. Adjusted sales fell 4% on lower realised prices, yet operating margin held ~47%. Milestones: six regulatory approvals, 10+ trial initiations, and DKK 22bn invested in R&D/commercial launches. Etavopivat showed positive Phase III sickle cell results (27% reduction in vaso occlusive crises); improving haemoglobin response, with regulatory submission planned for Q4 ’26.

Outlook: FY26 outlook raised on obesity care momentum (including Wegovy HD launch) and international rollouts. Management flagged disciplined SG&A, telehealth partnerships, and continued pipeline expansion across obesity, diabetes, and rare diseases.

Caterpillar (CAT) – Q1 FY26 Results (Mar 26) 897.45

Financial & performance highlights: EPS/HEPS US$5.54 (+30% YoY; Q1 FY25: US$4.26); operating profit US$3.1bn (+20% YoY); revenue US$17.4bn (+22% YoY; vs forecast US$16.5bn). Dividend US$1.30/share (quarterly, +8% YoY).

Valuation & capital return: Forward P/E is estimated at 40.3X based on FY26 consensus EPS of ~US$22.60 and current share price of US$ 912 This is based on analysts’ consensus forecasts of 18.6% HEPS growth which, albeit very robust, does not justify a PEG ratio of 2.1x. Dividend sustainability is supported by US$600m free cash flow in Q1 and a payout ratio of ~35%. Management reaffirmed its progressive dividend policy alongside US$5bn in buybacks. Nevertheless, although the stock is likely to maintain HEPS CAGR in the mid-twenties, it is overbought for now and liable to pull back.

Backlog & segment performance: Backlog surged to US$63bn (+79% YoY), driven by Power & Energy demand for large gensets and turbines linked to data centre expansion. Construction Industries grew 38% YoY, while Resource Industries lagged (+4% YoY) due to delivery timing.

Management commentary: “Our first-quarter results demonstrate the strength of our diversified portfolio and our ability to navigate complex market dynamics. We remain committed to delivering value to our shareholders while investing in growth opportunities.” – Joe Creed, CEO

Outlook: Management raised full-year sales and revenue guidance to low double-digit growth. Record backlog (US$63bn, +79% YoY) supports multi-year visibility, with large-engine capacity expansion expected to triple 2024 levels by 2030.

Growth drivers:

• Power & Energy: data centre build-outs linked to cloud computing and generative AI; healthy oil & gas demand (including gas compression).

• Construction: resilient North America activity supported by infrastructure programmes/Infrastructure Investment and Jobs Act (IIJA) and data centre investment.

• Resource Industries: mining demand (notably copper and gold).

• Aftermarket: ageing fleet and expanding services opportunities.

Comment: as above mentioned, the stock is currently overvalued and overbought so is likely to pull back indicating that long term holders should not be overweight at this stage.

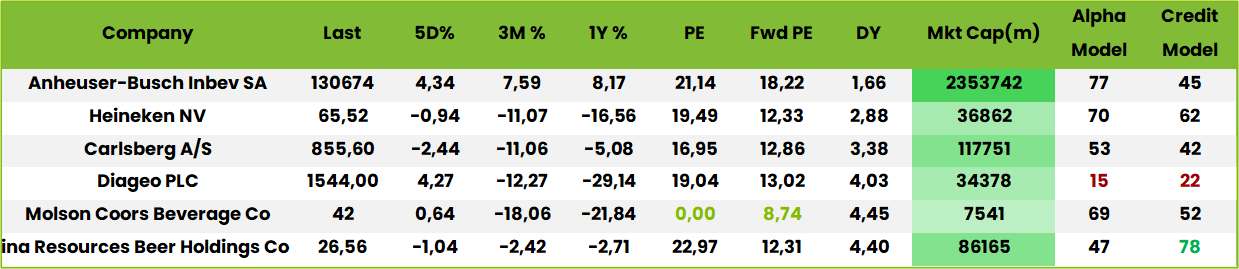

Anheuser-Busch InBev (ANH) Q1 26 Results (131148c)

HEPS: 0.97 USD (+20.8% from 0.81 USD)

EPS: 2 563m USD (+19.3% from 2 148m USD)

Operating Profit: 1 923m USD (+19.8% from 1 606m USD)

Revenue: 15 267m USD (+12.0% from 13 635m USD)

EBITDA: 5 437m USD (+5.3% from 5 162m USD)

Revenue growth was driven by megabrands, notably Corona (+16% outside its home market), and strong expansion in no-alcohol (+27%) and Beyond Beer (+37%). BEES Marketplace GMV surged 55% to USD 1.1bn. Volumes rose 0.8%, with beer up 1.2% and non-beer down 1.9%Current page. Outlook guides EBITDA growth of 4–8% in FY26, capex of USD 3.5–4bn, and a normalised ETR of 26–28%.

“Corona and our Beyond Beer portfolio continue to resonate strongly with consumers worldwide, reinforcing our strategy of broadening choice and driving sustainable growth.” – Michel Doukeris, CEO.

Comment: while Big Tobacco has much greater health concerns to contend with in coaxing smokers and others to the likes of vaping, Big Booze has much less of a problem to deal with despite the CEO noting that younger people in the US were drinking less beer. Moreover, they seem more easily persuadable to imbibe healthier non-alcoholic beverages. In addition, there are many African countries that haven’t even started yet (Kenya 12 kg per capita versus Germany 90 and SA 60). AbInBev struggled after swallowing the python SAB nearly 10 years ago and the share price dwindled from c. R1800ps to c. R1100ps just prior to covid when it collapsed. Now, however, after trading around R1050ps for four years it seems finally to be getting into its stride. On a forward PE of 18x it is not wildly cheap but can be bought by those that believe the oldest beverage known to mankind has a long way to go yet.

Combined Motor Holdings (CMH) Financial Results FY26 (3871c)

HEPS: 536.4c (+33.0% vs FY25)

EPS: 530.8c (+31.7% vs FY25)

Operating Profit: R748.6m (+17.1% vs FY25)

Revenue: R15.7bn (+18.6% vs FY25)

Dividend: 222cps declared, payable Jun ’26 (‑46.9% vs FY25)

NAV: 2 118c (+11.9% vs FY25)

Cash resources rose 20% to R1.15bn, strengthening liquidity. Profit and comprehensive income grew 29.7% to R391m, with return on shareholders’ funds improving to 27.1%. Dividend payout was reduced to preserve cash despite strong earnings growth. AGM scheduled for 3 Jun ’26 at Umhlanga Ridge. Outlook highlights continued resilience in consumer demand and disciplined capital allocation.

Comment: CMH has a big focus on Foton, China’s biggest manufacturer of commercial vehicles, which rose rapidly to become its fourth largest seller in FY26 behind Suzuki, Ford and Toyota and way ahead of the other 14 brands it sells. On a 7.3x PE and 5.6% DY (cum div until 12 June) it would be even more attractive on a normalisation of fuel prices.

Sappi (SAP) Interim Results for Q2 Mar 26 (1470c)

Results reported in USD

HEPS: (22) USc (N/M from Q2 Mar 25: (3) USc)

EPS: (68) USc (N/M from Q2 Mar 25: (3) USc)

Revenue: US$1,334m (‑1% from Q2 Mar 25)

EBITDA: US$52m (‑51% from Q2 Mar 25)

Sales volumes rose YoY, but lower selling prices, weaker dissolving wood pulp (‑12% YoY), and forex impacts drove losses. Net debt increased 18% YoY to US$1,964m, with leverage covenant suspended until Mar ’27. North American paperboard volumes grew 27% on Somerset Mill ramp‑up, while European profitability benefited from cost savings. Impairments of US$276m hit graphic paper assets.

Outlook remains cautious amid geopolitical tensions, higher oil and chemical costs, and structural decline in graphic papers. DWP demand is expected to stay strong, with prices rising to ~US$880/t, supporting Q3 margins.

Comment: despite numerous negatives (we lost count around 18!) the positives are significant. As mentioned above, dissolving wood pulp demand is increasing and North American paperboard demand is healthy which bode well for when the Somerset Mill ramp up completes. Also worth a mention is the likely JV with UPM-Kymmene to bring about much needed rationalization in the overtraded and declining graphic papers market. There is, however, no need to buy the stock yet.

Trading Statements & Updates

Vodacom* (VOD) Trading Statement FY26 (14616c)

HEPS: 1 028–1 071c (+20–25% from 857c)

EPS: 1 031–1 074c (+20–25% from 859c)

EBITDA: Guided double-digit growth ambition

Vodacom anticipates strong earnings growth aligned with its Vision 2030 strategy, targeting sustained double-digit EBITDA expansion. The trading statement signals resilience across operations and confidence in execution. Results due 11 May ’26

Sibanye Stillwater (SSW)* Operating Update Q1 Mar 26 (5480c)

EBITDA: R19.4bn (+371% from Q1 Mar 25)

SA PGM production rose 2% to 383koz, driving EBITDA up 393% to R12.4bn on an 87% higher basket price. SA gold EBITDA surged 160% to R4.7bn, supported by a 49% higher gold price. US PGM EBITDA rose to R777m despite higher AISC, aided by 88% stronger prices. Recycling EBITDA jumped 817% to R1.6bn on 138% higher volumes. Keliber lithium project construction completed, with ramp-up underway. Century zinc EBITDA improved to R467m despite lower output.

“Consistent operational delivery and disciplined cost management amplified exposure to improved metal prices, delivering a significant improvement in financial performance.” – Richard Stewart, CEO

Anglo American (AGL) Production Report Q1 Mar ’26 (86272c)

Copper: 170kt (+1% vs Q1 ’25)

Premium Iron Ore: 15.2Mt (‑2% vs Q1 ’25)

Manganese Ore: 759kt (+118% vs Q1 ’25)

Diamonds: 7.1Mct (+17% vs Q1 ’25)

Steelmaking Coal: 1.5Mt (‑31% vs Q1 ’25)

Nickel: 9.1kt (‑7% vs Q1 ’25)

Copper output benefited from Los Bronces’ second plant restart and stronger recoveries at Collahuasi, offsetting lower grades at Quellaveco. Iron ore volumes dipped slightly, while manganese surged after cyclone‑related disruptions in 2024. Diamond production rose on higher volumes from Venetia and Gahcho Kué, though realised prices fell 19%. Coal output was constrained by weather and prior incidents, while nickel declined due to maintenance. Portfolio optimisation continues, with coal and De Beers divestments progressing and the Teck merger expected to close between Sep ’26 and Mar ’27.

“We’ve delivered a strong start to the year across both Copper and Premium Iron Ore, tracking well to our mine plans.” – Duncan Wanblad, CEO.

Kumba* (KIO) Production & Sales Q1 Mar ’26 (32360c)

Production: 8.8Mt (‑2% vs Q1 ’25)

Sales: 9.3Mt (+3% vs Q1 ’25)

Finished stock: 7.2Mt (‑4% vs Dec ’25)

Realised FOB price: US$93/wmt (‑5% vs Q1 ’25), 8% above benchmark

Safety performance improved with TRIFR down to 0.49 despite higher hours worked. Sishen output rose 5% to 6.3Mt, offsetting Kolomela’s 15% decline to 2.6Mt due to planned stock drawdowns ahead of Transnet’s May shutdown. Logistics resilience supported higher sales, aided by port equipment availability. Kolomela achieved a 72% reduction in scope 2 carbon emissions via renewable wheeled power. Export routes to Asia and Europe remain secure despite Middle East conflict disruptions. FY26 guidance of 31–33Mt production and 35–37Mt sales is maintained, with UHDMS tie‑in scheduled for H2 ’26.

Gold Fields (GFI) Operational Update Q1 Mar 26 (74391c)

Revenue: US$4,855m (+67% from Q1 Mar 25)

Dividend: Final US$1,234m paid 16 Mar 26

Attributable gold-equivalent production rose 15% YoY to 633koz, supported by Salares Norte’s strong ramp-up (+245% YoY to 173koz). AISC increased 13% YoY to US$1,829/oz, while AIC rose 10% to US$2,046/oz, reflecting higher royalties, consumables and inflationary pressures. Net debt fell 34% YoY to US$1,304m, with leverage reduced to 0.19x EBITDA. Strategic milestones included Damang’s safe transition to Ghana’s government, progress on Tarkwa lease renewal, and advancement of the Windfall project toward final EIA approval. Sustainability commitments were extended to 2035, with St Ives’ renewable project 94% complete.

DRDGOLD (DRD) Operating Update for Q3 Mar 26 (4948c)

Operating Profit: R1,854m (+19% from Q2 Dec 25)

Revenue: R2,963m (+6% from Q2 Dec 25)

EBITDA: R1,813m (+21% from Q2 Dec 25)

Dividend: Interim R433.6m paid 16 Mar 26

Gold production rose 6% to 1,219kg on higher throughput and yield, while revenue benefited from a 13% increase in the average Rand gold price. Cash operating costs rose 5% but unit costs fell 4% to R960,270/kg. Growth capex decreased 16% to R693m as FWGR and Ergo projects neared completion. Liquidity strengthened to R2.3bn, debt-free, with facilities available. DRDGOLD remains on track to meet FY26 guidance of 140–150koz at ~R995,000/kg. A final dividend is under consideration for Aug 26.

Merafe (MRF) Production Report Q1 Mar ’26 (117c)

Ferrochrome production: 92kt (‑7% vs Q1 ’25)

Chrome ore production: 235kt (‑5% vs Q1 ’25)

Sales volumes: 101kt (‑9% vs Q1 ’25)

Output was impacted by planned maintenance and power supply constraints, though operational efficiencies limited the decline. Sales volumes fell due to weaker European demand and logistical bottlenecks at ports. Cost pressures from electricity tariffs and transport inflation persisted, but management noted improved furnace stability. The company continues to focus on cost containment and operational resilience amid challenging market conditions. Outlook highlights cautious demand recovery in Asia and ongoing volatility in ferrochrome pricing.

“We remain committed to disciplined cost management and operational excellence to navigate market headwinds.” – CEO Zanele Matlala.

Jubilee Metals (JBL) Operational & Production Update 9m FY26 (64c)

Saleable copper output rose 28.7% to 2,177t, driven by Roan’s 112% increase to 1,999t and Sable Refinery’s 27% rise to 957t cathodes. Molefe Mine mined 250,162t ore, with 20,064t dispatched at 1.84% Cu grade. Commissioning of Roan’s expanded dewatering circuit is near completion, targeting 110–120tpm of contained Cu, supported by a 14,000t stockpile. Molefe’s accelerated stripping programme to integrate Pits 2 and 3 is progressing, with completion expected Jul ’26, enabling ore delivery to rise above 30,000t per quarter.

“We continue to make strong progress in delivering our Zambia copper strategy, with Roan sustaining targeted production rates and Molefe expansion highlighting our transition towards a resource-backed copper producer.” – Leon Coetzer, CEO

MC Mining (MCZ – Formerly Coal of Africa) Activities Report Q3 FY26 (420c)

MC Mining advanced construction of the Makhado hard coking coal project, with commissioning of the coal handling and preparation plant scheduled for May ’26 and a 14km power line completed in Apr ’26. Uitkomst Colliery operations were temporarily suspended from 1 Mar ’26 to stem losses, with strategic options under review. Cash and facilities rose to US$5.4m, aided by US$19m in share subscription payments from Kinetic Development Group, which increased its stake to 51% in Apr ’26. Premium steelmaking coal prices averaged US$231/t, up from US$186/t in Q3 FY25. Christine He, CEO, noted: “Construction work and operational readiness activities are ongoing, with hot commissioning activities and start‑up of the Coal Plant expected to commence during May 2026.”

Datatec (DTC) Trading Statement FY26 (7510c)

HEPS: 38.5–40.5 USc (+51.0% to +58.8% from FY25: 25.5 USc)

EPS: 38.0–40.0 USc (+47.9% to +55.6% from FY25: 25.7 USc)

EBITDA: Adjusted EBITDA disclosed, excluding restructuring and share-based costs

Westcon International delivered strong performance in H2 FY26, while Logicalis International achieved exceptional growth. Logicalis Latin America improved gross profit and overall results. Underlying EPS, recalculated to exclude share-based payments, is expected at 47.0–49.0 USc, up 31.7%–37.3% YoY. The Board aligned reporting metrics with peers to enhance comparability. Results due 26 May ’26.

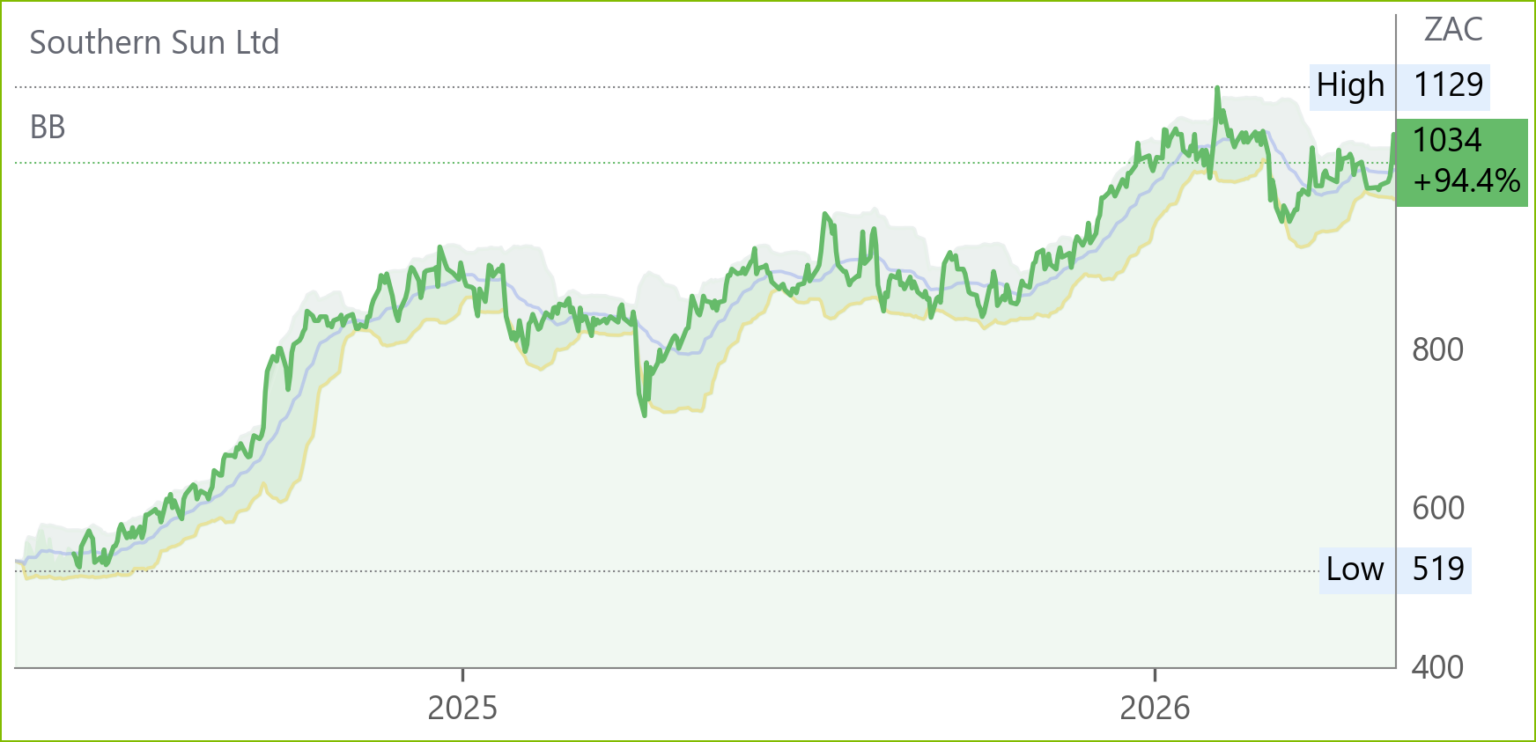

Southern Sun (SSU) Trading Statement for FY26 (1034c)

HEPS: 88.3–91.3c (↑18–22% from 74.8c)

EPS: 90.9–94.0c (↑19–23% from 76.4c)

Dividend: R335m returned via dividends; R359m via buybacks (37m shares)

Occupancy rose to 62.9% (FY25: 60.8%), driven by domestic hotels at 64.3% supported by MICE demand and inbound travel. Offshore recovery was aided by Paradise Sun’s reopening, though impacted by the Middle East war in Mar ’26. Net cash stood at R86m despite higher refurb capex. Trading momentum accelerated in H2, boosted by G20 Gauteng and stronger transient demand. Outlook highlights resilient domestic demand and cautious offshore recovery. Results due 20 May ’26.

Life Healthcare (LHC) Trading Update for 6M Mar 26 (1101c)

HEPS: 50.6–56.4c (>100% from H1 Mar 25: ‑155.8c)

EPS: 48.5–54.2c (>100% from H1 Mar 25: ‑155.2c)

Revenue: +2.2% to +2.6% YoY (c. R130m impact from funder curatorship)

EBITDA: Normalised +4.9% to +5.3%

Revenue growth was achieved despite the curatorship of a major funder, reducing income by c. R130m. Paid patient days declined 0.4%, driven by acute hospitals (‑0.9%), partly offset by complementary business growth (+3.4%). Tariffs rose 3.3%, with surgical activity lifting revenue per patient day by 4%. Occupancy averaged 67.5% (Q2 >70%). Impairments of R38m were recognised in non‑acute businesses. Normalised EPS is expected to rise 6–10% YoY, reflecting operational efficiency and margin improvement projects. Board changes include Adam Pyle’s retirement and Brett Mill’s appointment effective 1 Jun ’26. Results due 28 May ’26.

Astral Foods (ARL) Trading Statement for 6M Mar ’26 (24200c)

HEPS: 2 250–2 331c (+450–470% from 409c 1H’25)

EPS: 2 242–2 336c (+375–395% from 472c 1H’25)

EPS and HEPS surged due to strong recovery in poultry operations and improved feed cost management. The >30% variance between HEPS and EPS reflects once‑off adjustments. Astral highlighted operational efficiencies and favourable market conditions as key drivers. Outlook points to sustained profitability, though management cautions on feed price volatility and consumer demand pressures. Results due 18 May ’26.

Snippets

Reinet Fund’s (RNI) NAV per share rose slightly to €38.55 at 31 Mar ’26, up from €38.47 at Dec ’25, with total NAV at €6 603m. The increase of €13m reflects portfolio revaluations and cash resources. NAV remains subject to audit. Reinet Investments’ consolidated NAV will differ due to parent assets and liabilities.

Metair (MTA) refinanced R3.3bn SA Obligor debt with Standard Bank approval, extending repayment to five years aligned with earnings and capex for FY26. Facility C (R1.6bn) was converted into a senior loan, covenants eased, JIBAR replaced by ZARONIA, and EBITDA hurdles removed, strengthening capital structure and operational flexibility for strategic execution.

Aspen (APN) received SAHPRA approval to commence commercial release of locally manufactured human insulin from its Gqeberha facility, marking a milestone in its contract manufacturing agreement. This strengthens domestic supply capabilities and supports healthcare resilience. Outlook signals continued expansion in sterile manufacturing and contract partnerships, reinforcing Aspen’s strategic positioning in essential medicines.