Global Indices

Currencies, Crypto & Commodities

SA Indices

SA Upcoming Indicators & Dividends

Global Equity

NVIDIA (NVDA) Q1 FY27 Results Highlights ($215,33)

EPS: $1.87 (+85% YoY, forecast $1.77)

Revenue: $82bn (+85% YoY, +20% QoQ, forecast $79.2bn)

Gross Margin: 74.9%

Free Cash Flow: $49bn (+40% QoQ)

Data Centre Revenue: $75bn (+92% YoY)

Dividend: Raised to $0.25 per share (from $0.01)

Share Buyback: $80bn new authorisation

NVIDIA delivered record Q1 FY27 results, driven by surging AI and hyperscale demand. Data centre revenue rose 92% YoY, with Blackwell GPUs achieving the fastest ramp in company history. Free cash flow hit $49bn, enabling $20bn shareholder returns and a major buyback programme. New Vera CPUs and Rubin GPUs open a $200bn TAM, positioning NVIDIA as a leader in agentic AI. Outlook guides Q2 revenue of $91bn, with continued acceleration in AI infrastructure spending.

“Our record-setting results reflect our ability to deliver innovative solutions to our customers…Demand for AI infrastructure has gone hyperbolic” – Jensen Huang, CEO

Richemont* (CFR) Financial Results for FY26 (326218c)

HEPS: EUR 6.132 (‑3% from FY25)

EPS: EUR 5.926 (+26% from FY25)

Operating Profit: EUR 4.492bn (+1% from FY25)

Revenue: EUR 22.420bn (+5% from FY25)

Gross Profit: EUR 14.438bn (+1% from FY25)

Dividend: CHF 3.30 per share (+10%); special dividend CHF 1.00

Sales grew 11% at constant rates, driven by double‑digit growth in Jewellery Maisons and Americas. Profit rose 27% to EUR 3.484bn, aided by non‑recurrence of prior YNAP write‑downs. Jewellery Maisons delivered a 30.5% margin, while Specialist Watchmakers returned to growth in H2. Net cash strengthened to EUR 8.5bn. Management highlighted continued investment in craftsmanship, heritage, and footprint expansion. Outlook emphasises resilience despite currency headwinds and raw material costs.

“Richemont’s Maisons continue to build on their heritage and creativity, delivering sustainable growth while investing in long‑term value creation.” – Johann Rupert, Chairman.

Comment: ZAR Heps of 122.9 places the stock on a 26.5X PE which is close to its average. Sales at constant rates were up 11% led by the Americas at 17%, Europe up 9%, EMEA 13%, Japan 9% and ASIA PACIFIC 8% including China at a low 3% almost, but not quite, pooping the party (maybe because they’re turning to homegrown brands)

Astral Foods (ARL) Interim Results for 6M Mar ’26 (23992c)

HEPS: 2 318c (+467% from 409c 6M Mar ’25)

EPS: 2 321c (+392% from 472c 6M Mar ’25)

Operating Profit: R1.21bn (+348% from R271m 6M Mar ’25)

Revenue: R11.94bn (+11% from R10.72bn 6M Mar ’25)

Dividend: 1 160c per share (interim)

Revenue grew 11% to R11.9bn, while profit before interest and tax surged 348% to R1.21bn. Earnings rebounded sharply, with HEPS up 467% and EPS up 392%, reflecting recovery in poultry operations and improved cost management. Profit for the period rose to R896m, supported by stronger margins. Total equity increased 26% to R5.98bn, strengthening the balance sheet. The Board declared an interim dividend of 1 160cps, payable on 15 Jun ’26.

Sector peers: RCL Foods (RCL), Tiger Brands (TBS), AVI (AVI).

Comment: “the stars aligned” to produce “amaizing” results with global maize prices well down and poultry sales up. The resultant trailing 5.7X PE and 8.8% DY is unlikely to repeat this year with fuel price hikes looming and the risk of bird flu hovering. The latter risk will be mitigated by vaccinating 30% of the chickens and prevention of contact with wild birds. Further ahead the maize price, although likely to remain low for the current year, may well be a boosted if, as seems likely, we have a recurrence of El Nino next year. The share price has adjusted to a sensible assessment of possibilities and, with an ungeared balance sheet, could be a HOLD for the yield and for investors prepared to take their chances and watch developments.

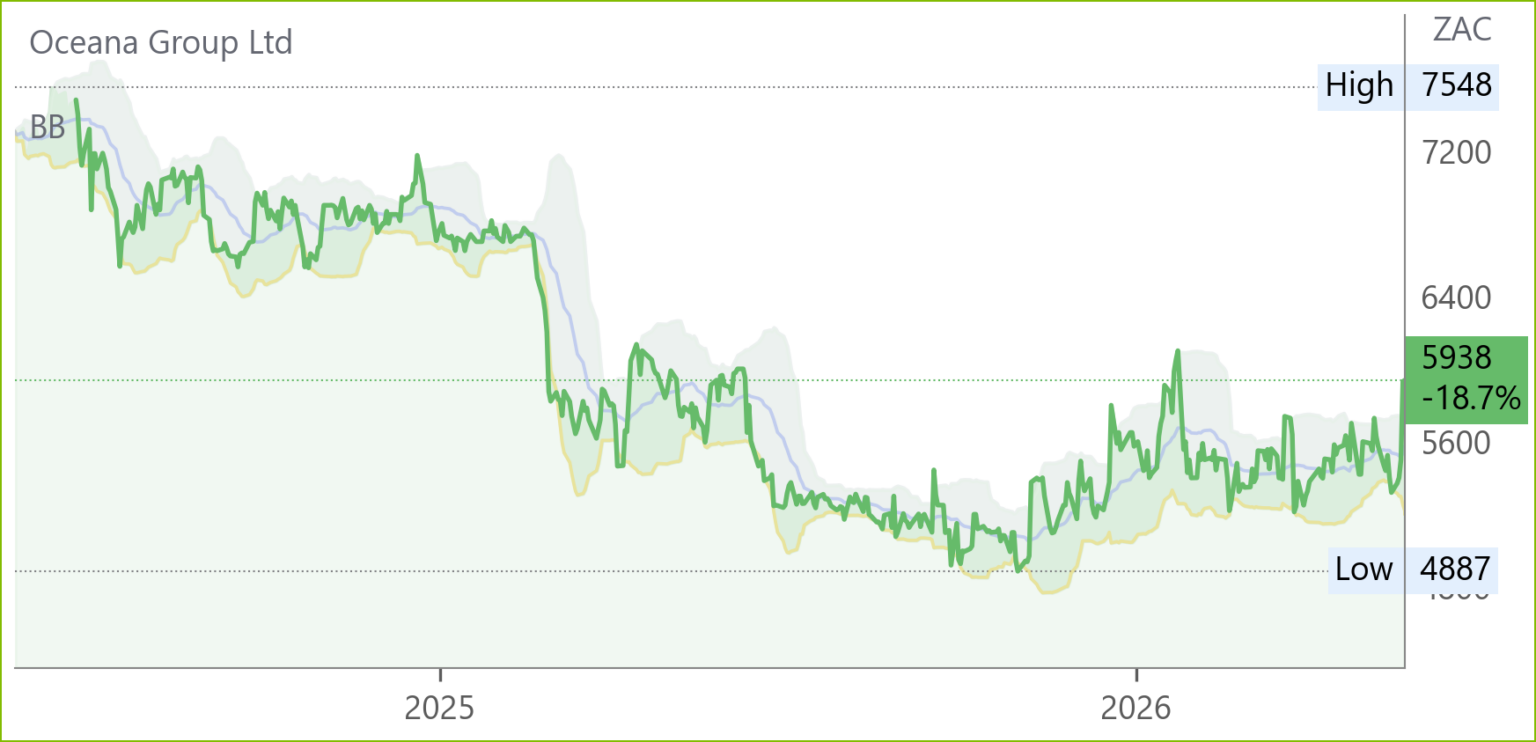

Oceana (OCE) Interim Results for 6M Mar ’26 (5938c)

HEPS: 349.8c (+7.7% from 324.9c)

EPS: 352.6c (+9.1% from 323.2c)

Operating Profit: R665m (‑1.6% from R676m)

Revenue: R4.88bn (‑6.0% from R5.19bn)

Gross Profit: Margin 28.1% (+0.3pp from 27.8%)

Dividend: 110c per share (interim, unchanged)

Revenue fell 6% due to weaker fishmeal and fish oil volumes and pricing, though Lucky Star foods grew 4.4% and Wild caught seafood rose 19.1%. Operating profit dipped slightly, offset by lower overheads and fuel hedging gains. Net debt halved to R1.73bn, improving leverage to 1.1x EBITDA. Cash generation surged to R1.41bn, aided by reduced working capital. Outlook highlights stronger pilchard biomass in SA and Namibia, higher anchovy TAC, and firm seafood demand, though rising fuel and freight costs may weigh on margins. A dual‑purpose vessel will enhance fleet versatility from Jan ’27.

Quantum Foods (QFH) Interim Results for 6M Mar ’26 (1059c)

HEPS: 86.5c (+16% from 74.8c)

EPS: 90.4c (+21% from 74.5c)

Operating Profit: R232m (+13% from R205m)

Revenue: R3.43bn (‑5% from R3.60bn)

Dividend: 22c per share (interim, vs nil HY25)

Quantum Foods reported stronger profitability despite a 5% decline in revenue, reflecting improved efficiencies and cost management. Operating profit rose 13% to R232m, while HEPS and EPS increased 16% and 21% respectively, supported by better margins in eggs and feed. Outlook highlights cautious optimism, with management focusing on operational resilience amid volatile input costs and consumer demand pressures.

WeBuyCars (WBC) Interim Results for 6M Mar ’26 (3559c)

– HEPS: 119.7c (-1.7% from 6M Mar ’25)

– EPS: 119.5c (-1.6% from 6M Mar ’25)

– Revenue: R14.2bn (+7.8% from 6M Mar ’25)

– Dividend: 33c per share (interim, +10% from 6M Mar ’25)

Unit sales rose 2.3% to 93,519, with record monthly volumes of 17,209 in Mar ’26. Buying volumes reached 95,328, supported by disciplined inventory strategy and three new supermarkets in Pretoria North, Cape Town and Witbank, expanding capacity by 2,980 bays (+23.6%). Market share improved despite deflationary used car prices and margin pressure from competitively priced Asian brands. A 49% stake in GoBid was acquired for R376.8m, strengthening digital auction capabilities. Outlook remains positive with plans to open Bloemfontein and Centurion facilities, targeting 23,000 monthly transactions by FY28.

Comment: the much publicised surge in sales of Asian new vehicles trimming some used car category margins and Heps as well as two directors selling R866m of shares at R46.27ps in February combined to affect WBC price and investor sentiment. As against that WBC market share has grown from 8.3% in 2023 to around 11% at present and the SA vehicle parc has grown by 7% from 10 million over the past 10years. WBC is therefore well on its way to achieve monthly vehicle sales of 23000 by 2028 and will not be repeating, but will benefit from, recent R600m capex, mainly for the three new supermarkets. Its state of the art technology, such as Inspectify, will facilitate both pricing accuracy as well as transactions at scale. After all, Asian vehicles, now that used vehicle pricing has been corrected, merely swell the SA car parc! So, expect recovery and growth in Heps for a change although the market may well take a “seeing is believing” attitude until FY 26 finals.

Nutun (NTU) Interim Results for 6M Mar ’26 (98c)

HEPS: -8.1c (loss, improved from -17.2c in 6M Mar ’25)

EPS: -8.1c (loss, flat vs -8.2c in 6M Mar ’25)

Revenue: R1.61bn (+9% from 6M Mar ’25)

EBITDA: R790m (+28% from 6M Mar ’25)

Nutun South Africa delivered strong collections growth, with Purchased Book Debt collections up 28% to R773m and RTC revenue up 27%. EBITDA rose 36% to R710m, supported by cost optimisation and portfolio acquisitions. Nutun International faced margin pressure from Rand strength and FX volatility, with EBITDA down 15% to R80m despite 20% growth in billable seats. AI-driven solutions in collections and BPO operations are already enhancing efficiency and profitability. Management remains focused on short-term profitability and long-term sustainable growth.

Calgro M3 (CGR) Financial Results FY26 (425c)

HEPS: 156.76c (-8.5% from FY25)

EPS: 167.36c (-2.5% from FY25)

Revenue: R942m (-14% from FY25)

Dividend: 8.64c per share (final)

NAV: R16.46 per share (+10.8% from FY25)

Revenue mix shifted significantly, with 70% of units transferred from non-core projects such as Scottsdene, La Vie Nouvelle and Jabulani. Bankenveld District City commenced infrastructure rollout, expected to deliver 20,000 housing opportunities, with 6,000 serviced sites over five years. Net debt-to-equity increased to 0.74. Share buybacks of 1.3m shares (1.17% of issued capital) will benefit FY27 EPS.

Ben Pierre Malherbe, CEO of Calgro M3, based on the current announcement:

• Focused on selling non core assets, including Scottsdene, to free capital and resources for new developments

• Strategic priority: Bankenveld District City (20 000 units), with R280m bulk infrastructure spend alongside Eris Property Group

• Core projects: Fleurhof (16 000 units, 10 000 completed) and South Hills (5 800 units remaining)

• Market recovery driven by bulk rental sales; election cycle uncertainty acknowledged.

• Memorial Parks revenue up 26% to R86m (gross margin up 54.9%), with over 100 000 grave sites, providing diversified risk profile.

Comment: HEPS rose from 106c in FY22 to 189c in FY24 when Bankenveld was bought together with Eris Properties and declined to 157c in FY26. TNAV, however, rose from 662c in FY22 to 1479c for a 72% discount in FY26. In addition to the abovementioned Bankenveld, Fleurhof and South Hills the other core property is Belhar next to the University of the Western Cape with 2200 units and 3600 beds to go. While construction of Bankenveld infrastructure is in the early stages and 15 years to sales completion is a long way off, the site is ultra strategic and the discount may well tempt some value investors as seems to be happening now in the case of Balwin.

Spear REIT (SEA) Financial Results FY26 (1313c)

HEPS: 89.45c (+3.26% from FY25)

EPS: 210.94c (+15.01% from FY25)

Revenue: R853.2m (+23.39% from FY25)

Dividend: 44.57c per share (final, reinvestment option available)

LTV: 22.94% (down from 27.08% in FY25)

NAV: R12.91 per share (+5.82% from FY25)

Distributable income rose 46% to R369m, supported by strong industrial and retail acquisitions including Maynard Mall. Occupancy across the portfolio remained high at 97–99%, with industrial assets driving 67% of GLA. Western Cape-only focus continues to underpin resilience, aided by semigration and infrastructure investment. The company is in negotiations to acquire a Western Cape property and associated letting enterprise, constituting a Category 2 acquisition under JSE rules. “Spear successfully concluded FY2026 in a mission statement aligned manner and enters FY2027 from a position of strength and positive forward momentum.” –Quinton Rossi, CEO.

Comment: Spear continued its steady, well defined and conservative progress in the Western Cape including commencing development on an industrial site opposite George Airport in which many prospective tenants have expressed interest. Management expects HEPS and DPS growth of between 6 and 8% for FY27.

Famous Brands (FBR) Financial Results FY26 (5015c)

HEPS: 583c (+12.1% from FY25)

EPS: 600c (+9.8% from FY25)

Operating Profit: R955m (+4.5% from FY25)

Revenue: R8.74bn (+5.6% from FY25)

Dividend: 382c per share (final, +10.7% from FY25)

\Revenue rose 5.6% to R8.7bn, supported by resilient demand across the Leading Brands portfolio. Operating profit increased 4.5% to R955m, maintaining a margin of 10.9%. Free cash flow declined 9% to R662m, reflecting higher investment activity. Supply Chain revenue grew 7% to R6.2bn, with operating profit up 14% to R504m, aided by in‑sourcing initiatives. International operations remained under pressure, with losses in the UK and AME regions. A share buyback programme of R54m was initiated, and debt refinanced at lower cost. “Our strategy remains resilient and flexible in a constrained operating environment, underpinned by agile franchise partners and disciplined capital allocation.” – Darren Hele, CEO.

Comment: CEO Hele says the investments in efficiencies and cost saving should make themselves felt in FY27 and most of the brands grew outlet numbers at a healthy rate viz. Debonair Pizza had 710 outlets and grew a net 22, Steers 652 (19), Mugg & Bean 254 (31) Milky Lane 102 (19) with Wimpy the exception 458 (-1). Given that FBR doesn’t compete in the chicken space and beef consumption in SA per capita is c.16.75 kg as against c. 40 kg of chicken Famous Brands might do better competing with its own brand against the likes of KFC and Chicken Licken as opposed to venturing into yet another offshore territory, this time into Malaysia. In brief, while the share has tracked sideways for 5 years it is priced accordingly on the 8.6xPE and 7.6% DY. Holders could stay to enjoy the yield and see how the expansion plans work. Sad to say, however, logistics is a significant component of company costs and might also cause customers to cook and stay at home if the Straits stay closed.

Afrimat (AFT) Financial Results for FY26 (3224c)

HEPS: 95.8c (+32.5% from 72.3c)

EPS: 80.0c (+27% from 63.0c)

Operating Profit: R523.7m (+9.6% from R477.7m)

Revenue: R10.0bn (+20.3% from R8.3bn)

Dividend: 33c per share (final, +32%)

Revenue rose 20% on strong aggregates and iron ore volumes, while cement losses narrowed after R271.6m in remedial maintenance. Cash generation improved to R831m, aided by asset disposals, with debt restructured into a R1bn medium-term loan. Nkomati anthracite suffered losses due to ferrochrome smelter shutdowns, offset by higher exports. Glenover rare earths and phosphate ramp-up positions Afrimat for battery minerals demand. Outlook highlights debt reduction, margin improvement, and strategic alternatives for cement. AGM scheduled for 29 Jul ’26.

Comment: Aggregates (R695m) and Iron Ore (R605m) made up the bulk of FY 26 PBIT of R524m with Shared Services -R450m and Cement -R127m. Aggregates and Iron ore will continue to improve (albeit it could take a few years before Transnet hits target delivery) and substantial savings have been made in Shared Services. Anthracite will benefit if Eskom does indeed facilitate ferrochrome production while cement is turning around but, more important, some kind of corporate action is under way which will facilitate Afrimat’s focus on mining. The Glenover rare earths project in Limpopo is probably a year or two away as studies and international partnerships are looked at but is of significant interest. On a 34xPE and 1% DY the stock is already discounting an early doubling or trebling of earnings and the Q & A session revealed a high level of interest from analysts keen no doubt to figure out how long it will take before Heps return to, and grow from, the 442c to 567c levels of the FYs 22 to 24 era. There is probably no rush to buy but some accumulation at these levels won’t go amiss.

Tharisa (THA) Interim Results for 6M Mar ’26 (2895c)

HEPS: US 16.6c (+472% from US 2.9c)

EPS: US 15.8c (+532% from US 2.5c)

Revenue: US$359.4m (+28% from US$280.8m)

EBITDA: US$104.3m (+138% from US$43.8m)

Dividend: US 2.5c per share (interim, +67%)

Revenue climbed 28% to US$359.4m, supported by robust demand for PGMs and chrome. EBITDA surged 138% to US$104.3m, while NPAT rose 468% to US$46.6m, reflecting operational leverage and favourable commodity prices. Underground development at Tharisa Mine advanced, enhancing ore access and production flexibility. Progress at Karo Platinum in Zimbabwe underscores diversification and growth potential, with commissioning milestones on track. Beneficiation initiatives delivered efficiency gains, reinforcing resilience against market volatility. The interim dividend of US 2.5c per share, up 67%, highlights confidence in cash generation and balance sheet strength.

(NPH)”Our strong financial and operational results are testament to the effectiveness of our integrated business model.” – Phoevos Pouroulis, CEO.

Comment: Tharisa is currently by far the lowest cost producer in the sector although this will change as it progresses from open pit to underground operations in SA. It is currently significantly undervalued relative to peers with size being a factor. Development at Karo Platinum in Zimbabwe proceeds steadily and is well within the capability of its strong balance sheet.

Southern Sun (SSU) Financial Results for FY26 (1009c)

HEPS: 90.1c (+19% from 75.6c)

EPS: 92.2c (+21% from 76.4c)

Operating Profit: R1.24bn (+21% from R1.02bn)

Revenue: R7.19bn (+9% from R6.61bn)

EBITDA: R2.43bn (+12% from R2.17bn)

Dividend: 30c per share (final, +20%)

Trading momentum strengthened in H2, supported by international conferences such as the G20 in Gauteng and improved transient demand in SA. Offshore hotels saw strong demand after Paradise Sun’s reopening, though the Middle East war in Mar ’26 dampened performance. Occupancy rose to 62.9%. Management highlighted resilience despite fuel cost uncertainty, with a strong balance sheet enabling development initiatives and potential share buybacks. “Our financial flexibility preserves optionality for shareholder returns while maintaining resilience through the cycle.” – Board statement

Sector peers: City Lodge Hotels (CLH), Tsogo Sun Hotels (TSH), Sun International* (SUI)

Comment: CEO Marcel von Aulock says the 2H momentum has continued into April and May and includes KZN where the Ethekwini municipality has gradually succeeded in cleaning up the beaches thus making for an 84% occupancy over December January.

That said, von Aulock says there will be no escaping the Middle East macro developments which have already diminished Middle East patronage at the newly refurbished Seychelles hotel. Otherwise, with a strong balance sheet and successful strategy of strongly upgrading the winners in its portfolio the group is well placed with occupancies nudging toward 64% albeit well below the 68% needed to make things really hum. On an 11.3x PE and 2.9% DY the stock is adequately priced for now and should only be bought when the ME conflict threats abate.

Trading Statements & Updates

Harmony Gold* (HAR) Operational Update for 9M Mar ’26 (27456c)

Gold and copper revenue rose 34% to R68.4bn, supported by a 39% increase in the average gold price to R2.02m/kg. Group gold production fell 3% to 33,393kg, though Q3 output rebounded 5% to 10,871kg. Underground recovered grade averaged 5.85g/t, above guidance. Copper production from CSA reached 9,596t, with grades of 3.49%. All-in sustaining cost increased 14% to R1.17m/kg. Free cash flow rose 87%, enabling a return to net cash of R1.3bn. A record interim dividend of 530cps was paid in Apr ’26. CEO Beyers Nel emphasised delivery of guidance for the 11th consecutive year, underpinned by operational discipline and strong margins.

Santam* (SNT) Operational Update for 3M Mar ’26 (38007c)

Gross written premium grew 9%, with strong contributions from MiWay and Santam Direct, though Santam Re was impacted by FX translation differences. Net underwriting margin remained above the 5–10% target despite R430m in weather‑related claims from flooding and wildfires. Investment returns were suppressed by weaker fixed‑interest markets, offset by FX gains. The ART segment delivered steady fee income, while capital cover stayed within the 145–165% range. Santam’s new Lloyd’s Syndicate wrote US$55m of business by May ’26, expected to accelerate premium growth later in the year, though a R300m operational loss is anticipated. A reinsurance branch licence was granted in India’s GIFT City, supporting FutureFit 2030 ambitions. Results for 6M Jun ’26 due 7 Sep ’26.

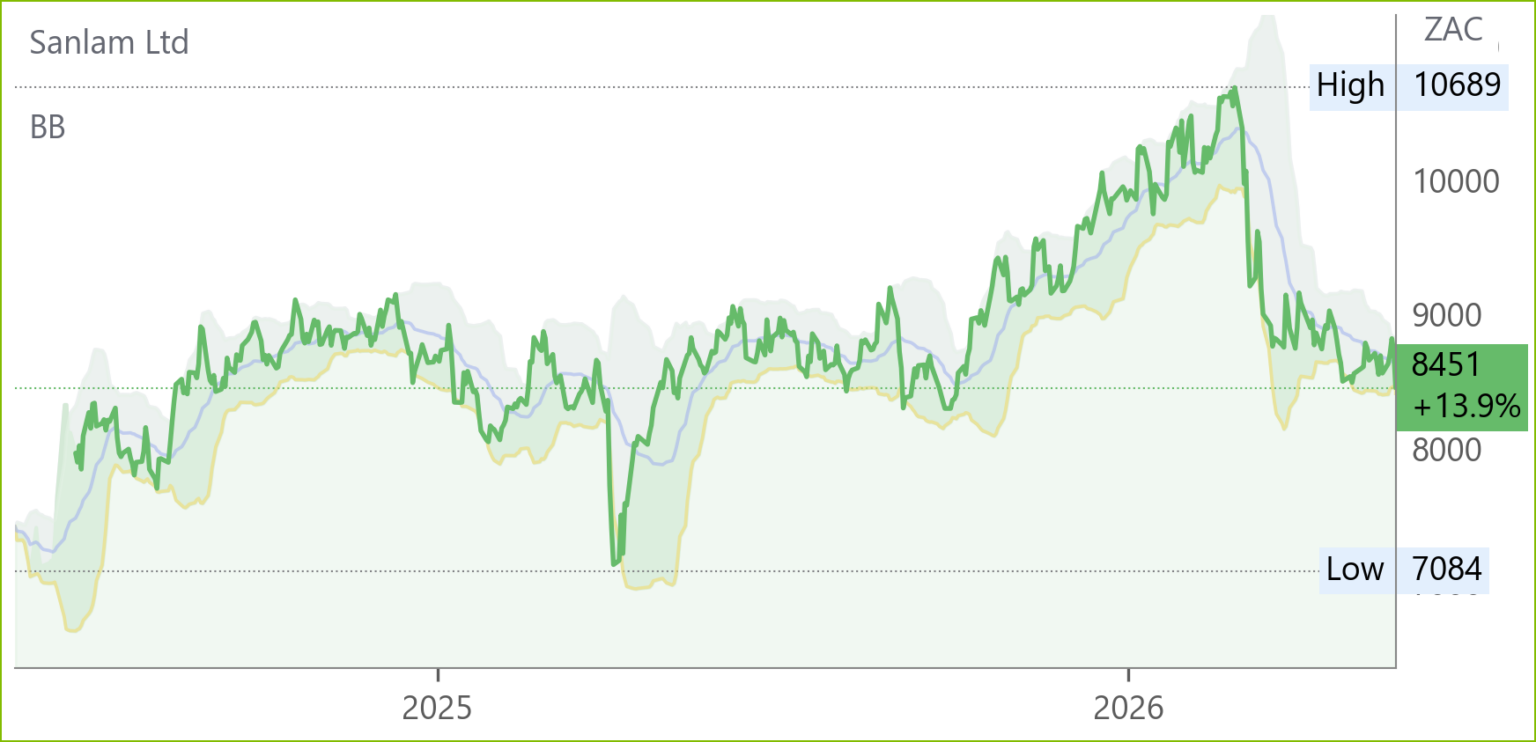

Sanlam* (SLM) Operational Update for 3M Mar ’26 (8451c)

Operating Profit: +8% (comparable basis)

New Business Volumes: +29%

Net Client Cash Flows: R38.6bn (+45%)

Discretionary Capital: R3.2bn (down from R8.1bn Dec ’25)

Sanlam delivered strong momentum with robust new business growth and resilient client activity despite volatile markets, elevated interest rates, and severe weather claims. Strategic execution included completing the Ninety One transaction, expanding Shriram holdings in India, and progressing Assupol integration in SA. Life insurance earnings rose on favourable mortality and fee income, while general insurance was impacted by R195m catastrophe claims. Net inflows surged, supported by Satrix and Glacier. Outlook guides resilient cash generation, margin recovery in SA and India, and medium‑term growth from banking, Lloyd’s Syndicate 1918, and cloud migration.

Pick n Pay (PIK) Trading Statement for FY26 (2422c)

EPS: Loss per share expected between ‑105.46c and ‑94.36c (+5% to +15% vs ‑111.01c FY25)

HEPS: Headline loss per share expected between ‑55.39c and ‑49.23c (+10% to +20% vs ‑61.54c FY25)

Operating Loss (PnP segment): R2.0bn–R2.1bn (vs R1.7bn FY25)

Pick n Pay’s FY26 trading statement reflects narrowing headline losses, supported by Boxer Retail’s strong performance and improved trading momentum in the final month of the year. While the Pick n Pay segment’s operating loss widened to R2.0bn–R2.1bn, EPS and HEPS are expected to show year‑on‑year improvement, signalling progress in stabilisation efforts. Management emphasised disciplined margin management, cost containment, and liquidity preservation. The group highlighted resilience in its core food retail operations despite challenging consumer conditions. FY26 results due 25 May ‘26

Nampak (NPK) Trading Statement for 1H26 (47900c)

Normalised HEPS (continuing ops): 3 900c–4 300c (vs 3 816.6c 1H25, +2%–13%)

HEPS (continuing ops): 3 100c–3 600c (vs 5 683.5c 1H25, ‑37%–‑45%)

EPS (continuing ops): 5 800c–6 600c (vs 6 064.4c 1H25, ‑4%–+9%)

HEPS (total ops): 3 200c–3 700c (vs 6 692.2c 1H25, ‑45%–‑52%)

EPS (total ops): 5 100c–5 900c (vs 35 842.2c 1H25, ‑84%–‑86%)

Nampak flagged mixed interim results for 1H26. Normalised HEPS rose modestly, aided by lower finance costs, but headline earnings fell sharply due to weaker Diversified contributions and Angolan can‑line relocation costs. EPS benefited from a R239m impairment reversal in Beverage Angola, though total EPS plunged on the absence of prior year disposal gains and a R70m impairment in Zimbabwe. The prior period included a R2.5bn profit on disposals, inflating comparatives. Interim results are due 29 May ’26.

Snippets

Anglo American (AGL) agreed to sell its Australian steelmaking coal portfolio to Dhilmar Limited for up to US$3.875bn, comprising US$2.3bn upfront and an earn‑out of up to US$1.575bn over five years. Proceeds will reduce net debt and complete Anglo’s exit from steelmaking coal, following the US$1bn Jellinbah sale, totalling up to US$4.9bn.

CEO Duncan Wanblad said: “This agreement represents another major step in the simplification of our portfolio ahead of completing our merger with Teck.” Completion is expected by Q1 ’27, subject to regulatory approvals.

Orion (ORN) Recent drilling at Flat Mine East delivered 7.88m at 9.24% Cu, including 3.33m at 17.12% Cu, confirming continuity of high‑grade norite‑hosted mineralisation. The intercept lies 36m down‑dip from OFMED154 and 100m along strike from OFMED153, reinforcing scale potential. Mineralisation remains open at depth, with follow‑up drilling (OFMED158) underway to extend the zone. Updated resources stand at 10Mt @ 1.3% Cu, underpinning Okiep’s strategic importance. “Our latest drilling provides a clear path to scale at Flat Mine East.” – Tony Lennox, CEO.

Orion secured firm commitments to raise $15.4m (ZAR181m) via a placement of ~698m shares at 2.2c (ZAR26c) each, with attaching options exercisable at 3.1c (ZAR37c) expiring May ’29. Proceeds will fund early works and development at the Prieska Copper Zinc Mine, optimisation and drilling at Okiep Copper, and working capital while finalising Glencore’s $250m financing facility. Strong support came from South African investors, reflecting Orion’s growing profile as an emerging copper producer.

SPAR (SPP) has entered into an agreement with A.F. Blakemore & Son to dispose of its South‑West England licence, 71 company‑owned stores, warehouse and logistics infrastructure, and related supply agreements. Completion is expected in stages between Jun and Sep ’26. In addition, 63 further stores are being sold to third‑party operators, with transactions at an advanced stage. Gross proceeds are estimated at GBP13m, with net cash broadly breakeven after costs. The disposal enables a clean exit from the UK, eliminating earnings drag and management distraction, while releasing capital to focus on core markets.

Pick n Pay (PIK) Pick n Pay successfully placed 57.3m Boxer shares (12.5% of issued stock) at R82.00 per share, raising R4.7bn. The price represented a 3.2% premium to the 30‑day VWAP. Following settlement, Pick n Pay retains a controlling 53.1% stake in Boxer. Proceeds will fund its turnaround plan, strengthen cashflow, and support growth strategy execution.

Balwin (BWN) Bidco, backed by Volker, Rodna, GRE Africa and the PIC, will acquire all eligible Balwin shares via a scheme of arrangement at R4.35 per share, representing premiums of 23% to the 30‑day VWAP and 41% to the 180‑day VWAP. Once implemented, Balwin will be delisted from the JSE and A2X. The consortium believes delisting will reduce costs and unlock growth flexibility, while shareholders gain liquidity at a premium.

Combined Motor Holdings (CMH) has issued a cautionary regarding a potential acquisition of properties owned by directors. Discussions are underway, but no binding agreement has been concluded. Shareholders are advised to exercise caution when trading CMH shares until full details are released. The proposed transaction could materially impact the company’s financial position and related party disclosures.