Finova Investor Digest

Global Indices, Currencies, Crypto & Commodities

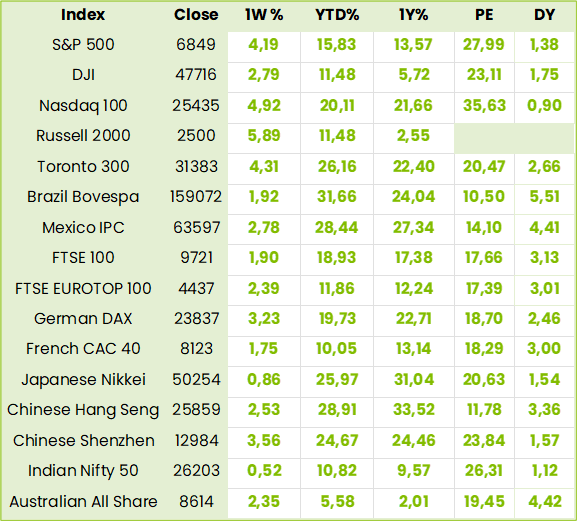

Global Indices 1 year to Date

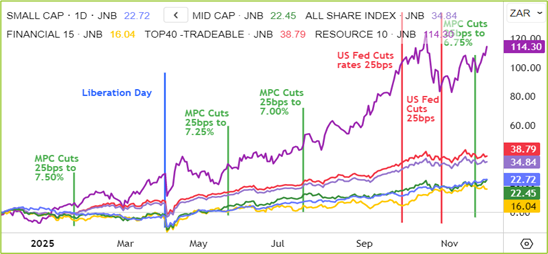

SA Indices

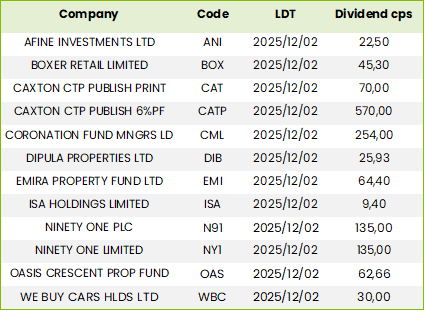

SA Upcoming Indicators & Dividends

SA Equity

Naspers (NPN) Interim Results for 6M Sep 25 (107006c)

Results reported in USD and converted to ZAR at an exchange rate of 17.30.

HEPS: 3 715c (↑13% from 3 287c)

EPS: 5 197c (↑22% from 4 259c)

Operating Profit: R3.07bn (↑>100% from R605m)

Revenue: R71.2bn (↑20% from R59.5bn)

EBITDA: R7.49bn (↑96% from R3.83bn)

Operating profit and EBITDA more than doubled, driven by strong ecommerce growth across Latin America, Europe, and India, alongside Tencent’s equity-accounted contribution. Improved cost discipline and share repurchases amplified earnings leverage.

Naspers advanced its AI-first strategy, expanding lifestyle ecommerce ecosystems across LatAm, Europe, and India. iFood, OLX, and PayU delivered strong growth, while acquisitions of Despegar, La Centrale, and Just Eat Takeaway.com (JET) strengthened regional portfolios. Free cash flow rose to R22bn, supported by Tencent dividends and operational improvements. The share repurchase programme reduced Prosus free float by 30%, creating US$63bn in value since inception. Divestitures included Udemy, Remitly, and Meituan, generating US$1.2bn in proceeds.

Management expects ecommerce revenue to reach US$7.3–7.5bn and EBITDA US$1.1–1.2bn by FY26, excluding JET, Integration of which is a priority, with focus on reigniting growth and margin expansion.

Comment: factors contributing to the negative reaction to the results include concerns as to the sustainability of the share buybacks, continued dependence on Tencent dividend and the fact that NPN’s own ecommerce operations, albeit turned around, still have a long way to go contribute meaningfully to earnings.

So, in way, it is a race against time, in which Fabricio Bloisi has to integrate and grow JET and as well as existing operations. His performance so far makes for a BUY at these levels. (See comment on Prosus below)

Prosus (PRX) Interim Results for 6M Sep 25 (106283c)

Results reported in USD and converted to ZAR at an exchange rate of 17.30.

HEPS: 3 095c (↑24% from 2 493c)

EPS: 4 377c (↑35% from 3 246c)

Operating Profit: R4.33bn (↑>100% from R1.04bn)

Revenue: R62.6bn (↑22% from R51.3bn)

EBITDA: R7.32bn (↑99% from R3.68bn)

Operating profit and EBITDA nearly doubled, supported by strong ecommerce margin expansion, iFood and OLX growth, and Tencent’s equity-accounted earnings. Free cash flow rose meaningfully, aided by Tencent dividends and operational improvements. Strategic acquisitions of Despegar, La Centrale and Just Eat Takeaway.com strengthened Prosus’s regional ecosystems, while divestitures of Udemy, Remitly and Meituan generated US$1.2bn. The share repurchase programme reduced free float by 30%, creating US$63bn in value. CEO Fabricio Bloisi stated: “We are only just beginning to build Prosus into a global tech leader. Relentless focus on results, innovation, and people will unlock substantial long-term value.” – Fabricio Bloisi, CEO.

Comment: while core headline earnings was up 13% the 24% increase in Core Heps was facilitated by the sale of Tencent shares and the ongoing buyback which has reduced the discount to NAV by 25% since inception in 2022. Not long ago the outgoing CFO was not able to say to an analyst when Prosus’ ecommerce investments would stop losing money but now, not only have they turned the corner but the new CFO, who has made it clear that boosting Free Cash Flow (FCF) is his priority, was able to point to 1H 26 ecommerce FCF of $59m from a negative $873m in 1H23. Prosus accordingly now values its three regional ecommerce systems at around $13bn for Latam, $17bn for Europe and $9bn for India. While, at around $39bn these are dwarfed by Tencent at $169bn, CEO Fabricio Bloisi is super bullish about the continuing execution of the AI driven strategy and growing inter company business. Together with Tencent going from strength to strength there is little doubt that SA investors need to be on full weight in PRX/NPN.

Tiger Brands (TBS) Financial Results for FY25 (35932c)

HEPS: 2 141c (↑31% from 1 631c)

EPS: 2 662c (↑50% from 1 776c)

Operating Profit: R3.8bn (↑35% from R2.8bn)

Revenue: R34.4bn (↑2.7% from R33.5bn)

Gross Profit: R10.8bn (↑10% from R9.8bn)

Dividend: 1 229cps final ordinary (↑79.7% from 684cps); 2 710cps final special dividend

EPS rose sharply (+50%) due to disposals and portfolio optimisation, while HEPS grew at a slower pace (+31%). Operating profit increased strongly (+35%) on volume growth and efficiency gains.

Disciplined operational excellence delivered earnings growth despite muted consumer spending. Value engineering, logistics optimisation and factory efficiencies lifted margins, while portfolio optimisation saw disposals of non‑core assets including Carozzi. Cash generation improved, with R3.2bn closing cash and R1.5bn share buybacks. A refreshed corporate brand and purpose were unveiled, emphasising affordable, quality foods. Interim relief payments were made in the ongoing listeriosis class action.

“We are deliberate about the active role we play in creating positive and sustainable outcomes across our value chain.” – TN Kruger, CEO.

Comment: These results confirm that the recovery, rejuvenation and rebranding continues apace with ongoing cost savings to come, not least of which will be the super bakery which commissions in late 2026. Brand recovery now stands at the #1 spot volume wise in 12 out 16 key focus brands. Long term guidance for ROIC has moved from “exceed WACC” in the short term in FY25 to 25% and operating margin from “exceeding single digits” to 15%. The share is cum the 3939cps special and final dividend until the 13 January LDT. Net of the dividend it is on a 14.7x PE and some judicious order placing in the holiday period could make it even more attractive. BUY

Astral Foods (ARL) Financial Results for FY25 (25225c)

– HEPS: 2,193c (+14% from 1,920c FY24)

– EPS:2,276c (+16% from 1,959c FY24)

– Operating Profit: R1,247m (+11% from R1,125m FY24)

– Revenue: R22.6bn (+10% from R20.5bn FY24)

– Dividend: 1,100cps (Final dividend 880cps, Interim dividend 220cps, up 112% YoY)

Astral Foods delivered a strong interim performance, with dividend per share more than doubling on improved cash generation and profitability. Operational efficiencies, higher poultry volumes and easing input costs supported earnings growth, despite persistent feed and energy cost pressures. Strategic investments in production facilities enhanced efficiency, while biosecurity measures mitigated avian influenza risks. Sustainability initiatives in water conservation and renewable energy advanced, alongside expanded employee development programmes. Market share gains were achieved through stronger distribution and customer engagement. Management remains cautiously optimistic, highlighting stable poultry demand and improved cost structures, with feed milling expansion and renewable energy investment expected to support margins.

Comment: the consensus 7.3x FPE implies a 51% increase in Heps which is certainly

possible but the industry is as renowned for its vulnerability to maize price fluctuations,

unpredictable outbreaks of bird flu and dumping of unwanted chicken parts from abroad as it is for the certainty of ongoing growth in demand for what is more affordable and by far the largest source of animal protein in South Africa. In our view, however, this is adequately discounted by post results price action.

Oceana (OCE) Financial Results FY25 (5291c)

HEPS: 564.8c (↓38.4% from 917.6c)

EPS: 562.4c (↓38.9% from 920.9c)

Operating Profit: R1.25bn (↓23.2% from R1.63bn)

Revenue: R9.99bn (↓0.7% from R10.06bn)

Gross Profit: R2.78bn (↓12.6% from R3.18bn)

EBITDA: R1.69bn (↓15.0% from R1.99bn)

Dividend: 285c per share (final dividend 175c, interim dividend 110c)

HEPS and EPS fell nearly 40% as global fish oil prices halved following Peru’s anchovy recovery, compounded by higher net interest costs and tax rates. Lucky Star expanded canned meats to 10% of sales, boosted local production by 24%, and maintained strong demand. Wild caught seafood rebounded, with hake delivering record earnings and horse mackerel returning to breakeven. A new squid vessel was launched, while lobster remained steady. Management expects fishmeal and fish oil prices to recover, supported by aquaculture demand. CEO Neville Brink stated: “Oceana is well positioned to capitalise on cyclical improvements and stronger pricing.” – Neville Brink, CEO.

Comment: Operating profit declined 23% largely due to the 54% decline in Fishmeal and Fishoil (USA) prices. A strong recovery in Wild Caught Seafood from a negative contribution to 18% of operating profit mitigated the effect of the recovery in Peru’s anchovy catch. This is generally attributed to the El Nino effects which some sources believe could begin to subside between January and March 2026. The FPE of 6.8x consensus implies a 39% growth in HEPS which may in turn include expected recovery in fishmeal oil prices as a result of this. CEO Brink says he doesn’t know when the negative factors will reverse but he knows they will and he is particularly confident in the general state of the business. Investors holding the stock should continue to do so while others could possibly watch for signs of reversal in this very particular aspect of climate change.

Quantum Foods (QFH) Financial Results FY25 (900c)

HEPS: 134.4c (+67.1% from 80.4c)

EPS: 137.8c (+72.3% from 80.0c)

Operating Profit: R361m (+55.3% from R232m)

Revenue: R7 147m (+12.9% from R6 332m)

Dividend: 34.0c final (net 27.2c after tax)

EPS rose 72.3% while HEPS increased 67.1% reflecting disposal-related gains excluded from headline earnings. Operating profit growth of 55.3% highlights strong margin recovery despite input cost pressures.

Revenue growth was driven by improved poultry and feed volumes, with operating profit boosted by efficiency gains. Headline earnings surged on stronger trading conditions. A final dividend was declared, marking a return to shareholder payouts. Outlook remains constructive, with management emphasising resilience in food security and cost management.

Stefanutti (SSK) Interim Results for 6M Aug 25 (451c)

HEPS: 34.54c (+161% from 13.23c Aug 24)

EPS: 28.96c (+1,594% from 1.71c Aug 24)

Operating Profit: R161m (+22% from R132m Aug 24)

Revenue: R3.66bn (+1% from R3.63bn Aug 24)

EBITDA: R232m (+40% from R166m Aug 24)

EPS surged due to settlement gains and improved operating performance, while HEPS rose 161% on stronger margins. EBITDA increased 40% reflecting efficiency improvements. Order book expanded to R13.4bn, with R4.2bn outside South Africa. “We are focused on disciplined execution and strengthening our balance sheet to deliver sustainable shareholder value.” – Willie Zeeman, CEO.

Comment: the receipt of R580m following the final resolution of the Eskom dispute will reduce the financial liabilities as at 31 August from R1215m to R635m which would still be way in excess of Capital and Reserves of R69m. In addition, Current Liabilities of R4.4bn were R1.2bn in excess of current assets of R3.2bn. The directors accordingly said, “These circumstances continue to indicate that a material uncertainty exists that may cast doubt on the group’s ability to continue as a going concern.” While annualizing 1H Heps to 69c would put the stock on a notional 6.6x PE dividends would still be a long way off and investment high risk.

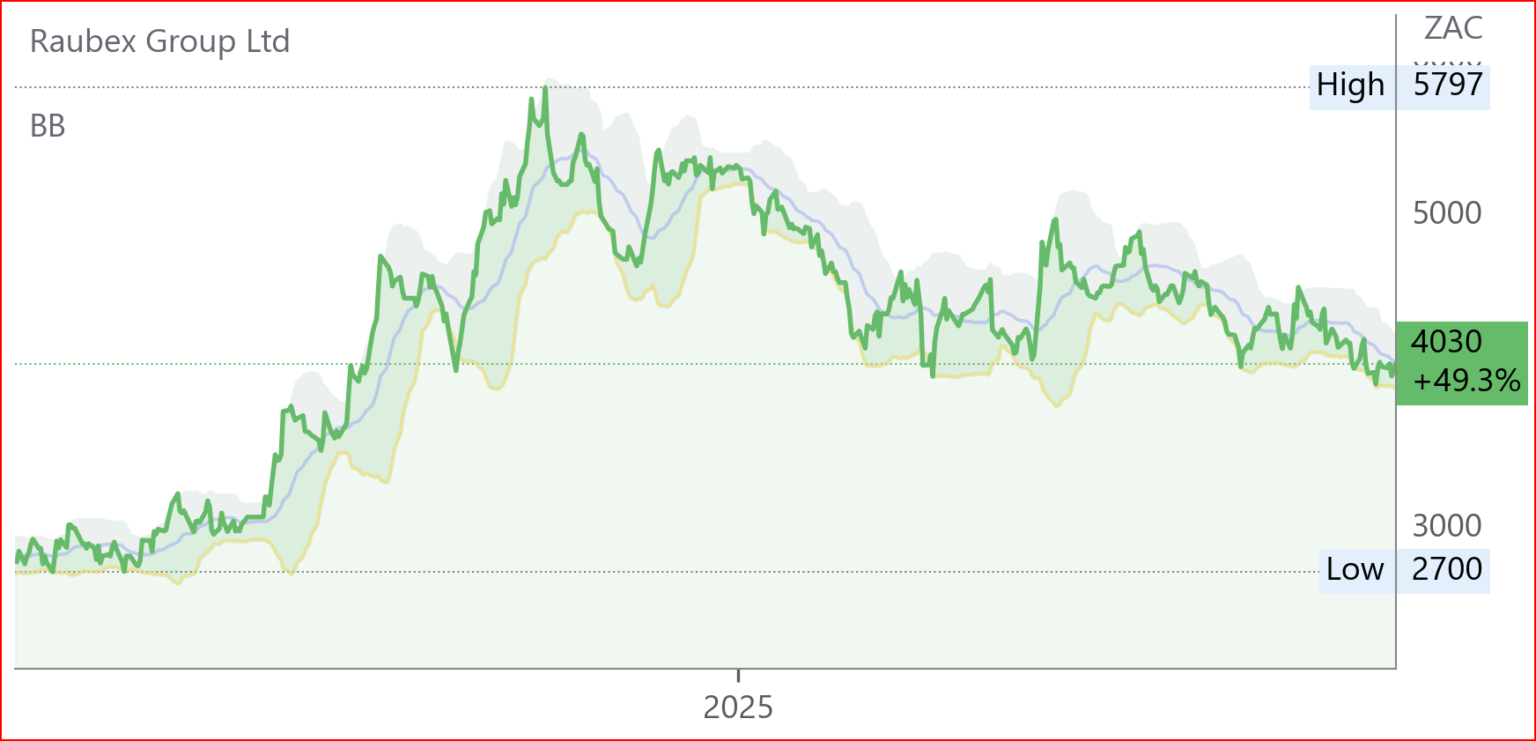

Raubex (RBX) Interim Results for 6M Aug 25 (4030c)

HEPS: 243.5cps (↓14.4% from 284.3cps)

EPS: 245.3cps (↓14.2% from 286.0cps)

Operating Profit: R603m (↓28.7% from R846.2m)

Revenue: R10.84bn (↓1.0% from R10.95bn)

Dividend: 81cps per share

Operating profit declined nearly 29% due to divisional trading challenges and cost pressures. HEPS and EPS fell over 14% as margin compression and reduced operational efficiency impacted profitability. Revenue was marginally lower year-on-year.

Raubex maintained strategic momentum despite softer earnings. The order book expanded 8% to R30.44bn, reflecting strong future prospects. Cash generated from operations halved to R762.4m, while capital expenditure fell 23% to R581.4m. Diversification across sectors and geographies helped offset headwinds. Divisions faced operational challenges, but strategic expansion and resilient execution supported performance. The interim dividend of 81cps reflects continued shareholder commitment.

PPC (PPC) Interim Results for 6M Sep 25 (544c)

HEPS: 25c (↑15% from 22c)

EPS: 25c (↑15% from 22c)

Operating Profit: R688m (↑37% from R502m)

Revenue: R5.38bn (↑6.2% from R5.07bn)

EBITDA: R983m (↑23.5% from R796m)

Dividend: US$20m declared in Zimbabwe operations

Operating profit rose 37% on stronger South African margins and cost discipline, with Zimbabwe recovering after a Q1 shutdown. The “Awaken the Giant” strategy drove efficiency gains, logistics savings and improved procurement, lifting net cash inflow 30% to R661m despite RK3 project payments. PPC Zimbabwe declared US$20m dividends and secured a US$30m land disposal, while ROIC advanced to 13.4% from 7.1%. Management anticipates further margin expansion and cash generation, supported by RK3 and operational optimisation. CEO Matias Cardarelli stated: “The ‘Awaken the Giant’ turnaround is redefining PPC’s trajectory, strengthening competitiveness and delivering consistent profitability.” – Matias Cardarelli, CEO.

Mr Price (MRP) Interim Results for 26W Sep 25 (21003c)

HEPS: 513.0c (+6.5% from 482.0c)

EPS: 512.8c (+6.5% from 481.5c)

Operating Profit: R2.1bn (+5.7% from R2.0bn)

Revenue: R18.6bn (+5.4% from R17.6bn)

Gross Profit: R7.4bn (+6.2% from R7.0bn)

Dividend: 323.2c interim dividend (+6.5% YoY)

Mr Price delivered resilient interim results, with HEPS and EPS rising on stronger gross margins and disciplined cost control. Revenue grew 5.4% to R18.6bn, supported by 91 new store openings and omni‑channel expansion. Gross profit increased 6.2% as effective inventory management reduced markdowns, while operating profit rose 5.7% despite a constrained consumer environment. Retail sales advanced 5.5% to R17.8bn, with online sales up 9.7% and Power Fashion achieving its 14th consecutive quarter of growth. Homeware and telecoms delivered solid gains, and the group ended debt‑free with R3.0bn in cash. Management expects gradual improvement in 2026, aided by lower inflation and interest rates.

Pepkor (PPH) Financial Results FY25 (2614c)

HEPS: 161c (+14.8% from 140c FY24, +23.4% normalised)

EPS: 153c (+>100% from 63c FY24)

Operating Profit: R11.1bn (+13.2% from R9.8bn FY24)

Revenue: R95.3bn (+12% from R85.1bn FY24)

Gross Profit: 39.8% margin (+150bps from FY24)

Dividend: 53cps (+9.2% from 48.5cps FY24)

EPS more than doubled due to tax provision adjustments, while HEPS rose 23.4% on a normalised basis. Revenue grew 12% with strong trading momentum, and operating profit increased 13.2% supported by margin expansion. Market share gains were recorded in babieswear, kidswear, schoolwear and prepaid handsets, with 6,000th store opened and 10m new customers added digitally. Flash fintech throughput rose 23% to R60bn. Strategic acquisitions included Choice Clothing, Ayana adultwear, and Cloudbadger fintech.

Outlook guides continued expansion with 250–300 new stores in FY26, integration of acquisitions, and entry into banking. “Record profitability in FY25 has established a solid foundation for FY26, with growth in fintech and financial services a strategic priority.” – Pepkor management.

Southern Sun (SSU) Interim Results for 6M Sep 25 (933c)

HEPS: 24.8c (+2% from 24.3c Sep 24)

EPS: 24.5c (‑1% from 24.7c Sep 24)

Operating Profit: R329m (‑1% from R332m Sep 24)

Revenue: R3.12bn (+5% from R2.97bn Sep 24)

EBITDA: R818m (‑0.5% from R822m Sep 24)

Domestic operations delivered resilient growth, with South African hotels achieving 60.6% occupancy and a 6% rise in average room rates to R1,369. Rooms revenue lifted to R2.0bn, supported by conferencing, events and group travel. Offshore operations posted a R9m loss due to Paradise Sun refurbishment and weaker trading in Maputo and Tanzania. Net debt rose to R481m after refinancing into two‑year revolving credit facilities. October ’25 occupancy peaked at 73.3%, surpassing World Cup levels in 2010.

Tsogo Sun (TSG) Interim Results for 6M Sep 25 (705c)

HEPS: 73.9c (↑7% from 69.1c)

EPS: 64.9c (↓1% from 65.6c)

Operating Profit: R1.7bn adjusted EBITDA (↓3% from R1.77bn)

Revenue: R5.56bn (↓1% from R5.62bn)

EBITDA: R1.72bn (↓3% from R1.77bn)

Dividend: 15cps interim (net 12cps after tax)

HEPS rose 7% while EPS fell 1%, a divergence >30% driven by non‑recurring items and accounting adjustments. EBITDA and revenue declined modestly, reflecting softer trading conditions. Headline earnings increased slightly to R769m, supported by cost management and reduced net debt, which fell to R6.8bn (↓R386m). The net debt/EBITDA ratio improved to 2.01x, strengthening covenant compliance. Management highlighted resilience in hospitality demand despite macroeconomic pressures.

Operating Updates & Trading Statements

Spar (SPP) Trading Statement FY25 (10400c)

HEPS: 748.1–792.9c (↓11.5%–16.5% from 896.0c)

EPS: 375.4–458.9c (↓45%–55% from 895.6c)

Operating Profit: ↑ (FY25 H2 stronger vs FY25 H1, exact value not disclosed)

Revenue: ↑ modestly (FY25 H2 uplift vs subdued FY25 H1)

EPS fell sharply due to once‑off impairments of Southern Africa corporate stores, SPAR Switzerland and AWG totalling R5.2bn, alongside Poland‑related financing costs and tax. Exiting Poland and Switzerland strengthened focus on core markets, reducing net debt 40% to R5.4bn. Southern Africa delivered improved grocery and liquor sales, while Ireland achieved growth despite FX headwinds. Asset values were reassessed, lowering equity, but gearing fell below 2x. Management prioritised supply chain resilience, technology enablement and operational discipline. CEO emphasised: “Our stronger balance sheet and disciplined capital allocation will support the next phase of growth, creating sustainable long‑term value for shareholders.” Results due 8 Dec ’25.

Nutun (NTU) Trading Statement for FY25 (89c)

HEPS: –13.8c to –15.0c (↓31–37% from –21.8c)

EPS: –29.6c to –31.1c (↓75–77% from –126.2c)

HEPS and EPS diverged >30%, reflecting once‑off settlement of obligations under a prior commitment agreement. EPS was heavily impacted by discontinued operations and legacy restructuring costs, while HEPS better reflects continuing operations.

Nutun completed a two‑year restructure, now operating through Nutun South Africa and Nutun International. Both divisions are customer‑centric, with streamlined cost structures and defined target markets. Management emphasised a pivot to profitability and growth from FY26, free of restructuring drag. Results due 1 Dec ‘25

Jubilee Metals (JBL) Operational & Projects Update Q1 FY26 (67c)

Copper production rose 65% to 938t (Q4 FY25: 568t), driven by stable Roan output and Molefe mine’s commencement of high-grade ore deliveries. Improved power supply agreements ensured uninterrupted operations, materially boosting volumes.

Operations in Zambia advanced under Jubilee’s Three-Pillar Strategy:

i) Roan concentrator achieved stable production, supported by expanded filtering capacity.

ii) Molefe mine successfully recommenced operations, delivering high-grade ore to Sable refinery.

iii) The Large Waste Project progressed with independent resource reviews and infill drilling plans.

A potential joint venture for Molefe resource drilling is well advanced, expected to conclude Nov ’25. Lower-grade ore stockpiles exceeded 2Mt, growing at ~70,000t per month.

Copper production guidance for FY26 revised to 4,500–5,100t, more than double FY25’s 2,211t, subject to rainy season impacts. Molefe mine is on track to ramp up to 8,500t per month by Q3 FY26, while Roan targets a 33% throughput increase. CEO Leon Coetzer stated: “It has been a significant year as we become a pure Zambia-focused copper producer. With Roan and Sable fully operational and Molefe expanding successfully, our copper business is stabilising ahead of a new phase of growth.” – Leon Coetzer, CEO.

Growthpoint (GRT) Investor Update for Q1 FY26 (1750c)

Operating Profit: R249.2m development & capex spend (Q1)

Dividend: Guidance for FY26 payout ratio 87.5% (DPS growth 6–8%)

LTV: SA Loan-to-Value ratio remains low, debt reduced to R37.8bn (↓3.3% from FY25)

Vacancies improved to 7.4%, lowest since Jun ‘19, driven by new lettings in office and logistics. Retail trading density rose 5% y/y to R37 020/m², with footfalls up 3%. Strategic disposals worth R391.6m completed, with R3.6bn targeted for FY26. ESG initiatives advanced with solar PV capacity reaching 61.54MWp and rollout of renewable wheeling agreements. “Improved performance is evident across all three domestic portfolios, with the V&A Waterfront exceeding expectations and international investments on track to deliver results in line with guidance.” – Growthpoint Board. Results due 11 Mar ‘26

Fortress (FFB) Trading and Pre‑Close Operational Update FY26 (2576c)

Dividend: Guidance for distributable earnings raised to R2.099bn–R2.129bn for FY26 (↑7.3%–8.8% YoY)

LTV: 39.8% (↓ from 40.2% Jun ’25)

Logistics remains the standout performer, with SA vacancies at 0.3% and CEE vacancies reduced to 9.9%. New developments at Eastport, Longlake and Clairwood are progressing, while acquisitions in Poland and Romania expand the pipeline. Retail assets delivered 3.9% like‑for‑like turnover growth with vacancies at 0.6%. Capital recycling continues, with disposals at a 4.9% premium to book value. Solar PV capacity rose to 35.9MWac, with further installations planned. Liquidity strengthened via new €75m facilities, and cash plus available facilities total R4.6bn.

Accelerate (APF) Trading Statement for 6M Sep 25 (55c)

Distributable earnings improved sharply to R56m–R58m versus a distributable loss of R11.1bn in HY24, reflecting restructuring initiatives and an insurance settlement. No dividend declared, consistent with prior period, as cash flow is prioritised for working capital and capex. Restructuring initiatives and insurance proceeds supported a return to distributable earnings. Management emphasised stabilisation of operations and liquidity preservation. Results due 28 Nov ‘25

Nampak (NPK) Trading Statement for FY25 (53500c)

HEPS: 10 100c – 10 700c (↑>100% from 3 361.1c in FY24)

EPS: 13 200c – 14 500c (↑75–92% from 7 554c in FY24)

HEPS more than tripled while EPS rose c.75–92%, a divergence >30% driven by once‑off items including interest cost reduction, pension fund surplus, and settlement of a Covid‑19 insurance claim. EPS also benefitted from recycling a R2.2bn foreign currency translation reserve.

Asset disposals continued, with several operations classified as held for sale. Significant once‑off gains included R369m interest savings, R47m pension surplus, and R195m insurance settlement. Prior year results were impacted by medical aid gains and other non‑recurring costs. Results due 8 Dec ‘25

Sea Harvest (SHG) Trading Statement FY25 (938c)

HEPS: ≥165c (+200% from 55c FY24)

HEPS is expected to rise at least 200% to 165c, driven by higher catch rates, improved pricing, and efficiency gains in the hake business. Strong operational performance underpinned the turnaround, with further guidance on EPS and HEPS ranges to follow once certainty improves. Year‑end results are scheduled for release on 3 Mar ’26. Ladismith Cheese will be sold to Fairfield Dairy for up to R850m, settling entirely in cash. The sale aligns with its strategy to halve debt within three years by exiting non-fishing assets. Proceeds will reduce long-term debt, while competition approval and lender consents remain key suspensive conditions. Effective date expected early 2026.

Snippets

Harmony (HAR) approved the US$1.55–1.75bn Eva Copper Project in Queensland, Australia, following a positive feasibility study. Expected to produce ~65kt copper and 19koz gold annually in early years, with a 15‑year mine life. Funded through cash flow and debt, the project diversifies Harmony into copper, enhancing resilience and long‑term growth prospects. Harmony’s Eva Copper project, alongside the MAC Copper acquisition, will deliver ~100,000t copper annually, complementing gold output. CEO Beyers Nel highlighted diversification into a Tier 1 jurisdiction, enhancing resilience, margins, and long‑term value through strong cash flows and exposure to robust copper fundamentals.

Pan African (PAN) completed a feasibility study on Soweto tailings, selecting a 600ktpm expansion at Mogale Tailings Retreatment. The project, costing US$160m, targets 30–35koz annual gold output for 15 years, with IRR up to 40% at higher gold prices. CEO Cobus Loots said the circuit will boost production to nearly 100koz/yr and accelerate rehabilitation.

BHP Billiton (BHG) confirmed it will no longer pursue a merger with Anglo American after preliminary talks. While acknowledging strategic merits, BHP emphasised confidence in its organic growth strategy. The statement, issued under UK Takeover Code Rule 2.8, reserves rights to revisit if circumstances change, including third‑party offers or Anglo’s board consent.

Exxaro (EXX) through its subsidiary Cennergi, will acquire Acciona’s majority stakes in the 138MW Gouda Wind Farm and 75MW Sishen Solar Farm, plus the O&M company, for R1.7–R1.8bn. The deal lifts Cennergi’s net operating capacity to 317MW, rising to 497MW with projects under construction, enhancing stable, treasury‑backed earnings via long‑term Eskom PPAs until 2034/35.

Nedbank (NED) announced a confidential settlement with Transnet, ending litigation over interest rate swap transactions from 2015–16. The bank will pay R600m without admission of liability, aiming to preserve its long‑standing relationship with Transnet and support infrastructure investment. Management reaffirmed governance compliance and confirmed FY25 guidance remains on track, excluding this once‑off expense.

Labat Africa (LAB) accepted a R10m offer from 64P Investments for its healthcare subsidiaries, marking a full exit from cannabis activities. Assets include cultivation, R&D, genetics, consulting, CBD products and a dormant entity. Proceeds will reduce debt and fund ICT, logistics and digital platforms. The board said pivoting away from cannabis supports strategic focus and shareholder value.

Remgro (REM) confirmed fulfilment of all conditions precedent for the Vodacom (VOD) acquisition of a 30% stake in Maziv, housing Vumatel and Dark Fibre Africa. Approval by ICASA, including the I‑ECNS licence, clears implementation on 1 Dec ’25. The transaction strengthens Vodacom’s fibre footprint and validates CIVH’s asset consolidation strategy, enhancing long‑term growth prospects for both parties.

Sirius Real Estate (SRE) expanded its German portfolio with two acquisitions: a €31.9m Hamburg business park (89% occupied, €2.15m rent roll, 6.1% yield) and a €43.7m Feldkirchen park near Munich (94% occupied, €3.4m rent roll, 7.8-year WAULT). Anchored by tenants like Excelitas and Bosch subsidiary, these deals strengthen Sirius’s €2.8bn German-UK industrial portfolio, offering “day one income” and long-term growth potential. The acquisitions reinforce its €340m momentum in 2025 and enhance diversification and rental resilience.