Finova Investor Digest

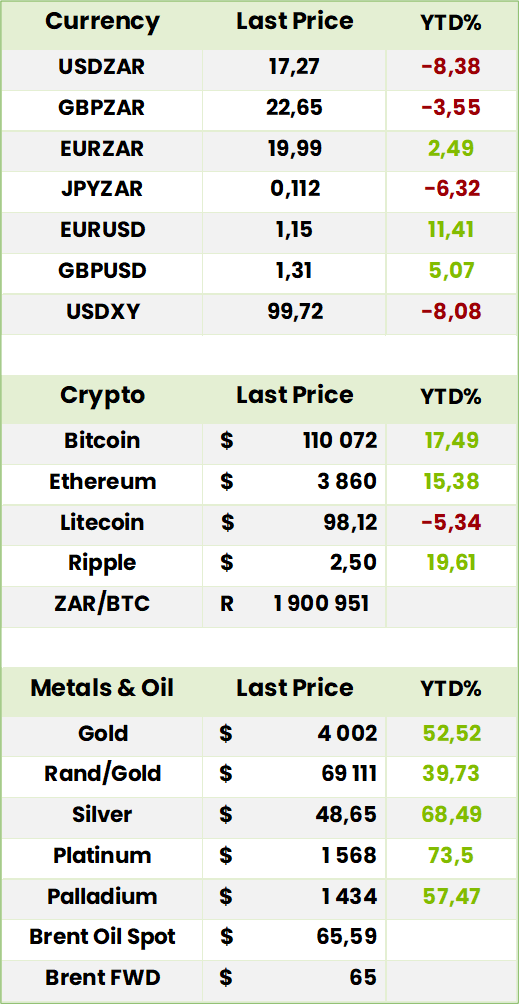

Global Indices, Currencies, Crypto & Commodities

Global Indices 1 year to Date

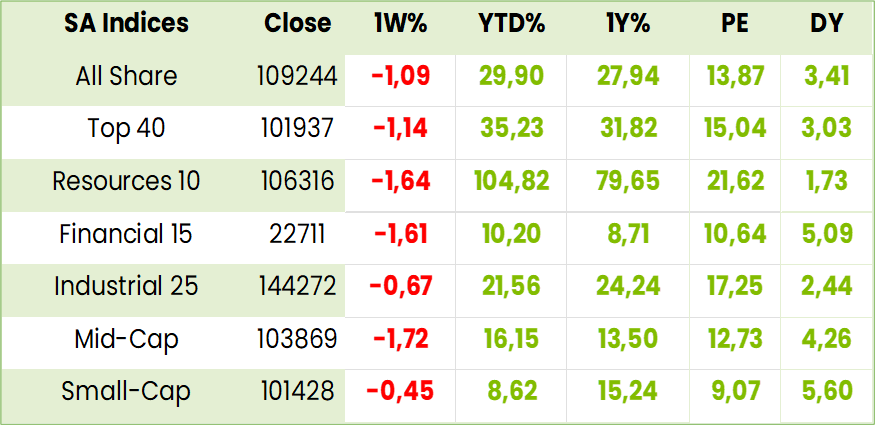

SA Indices

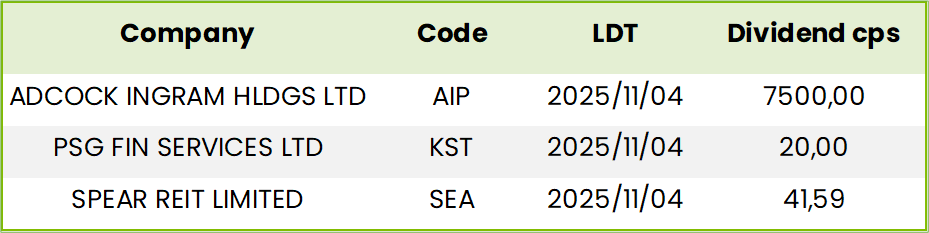

SA Upcoming Indicators & Dividends

SA Equity

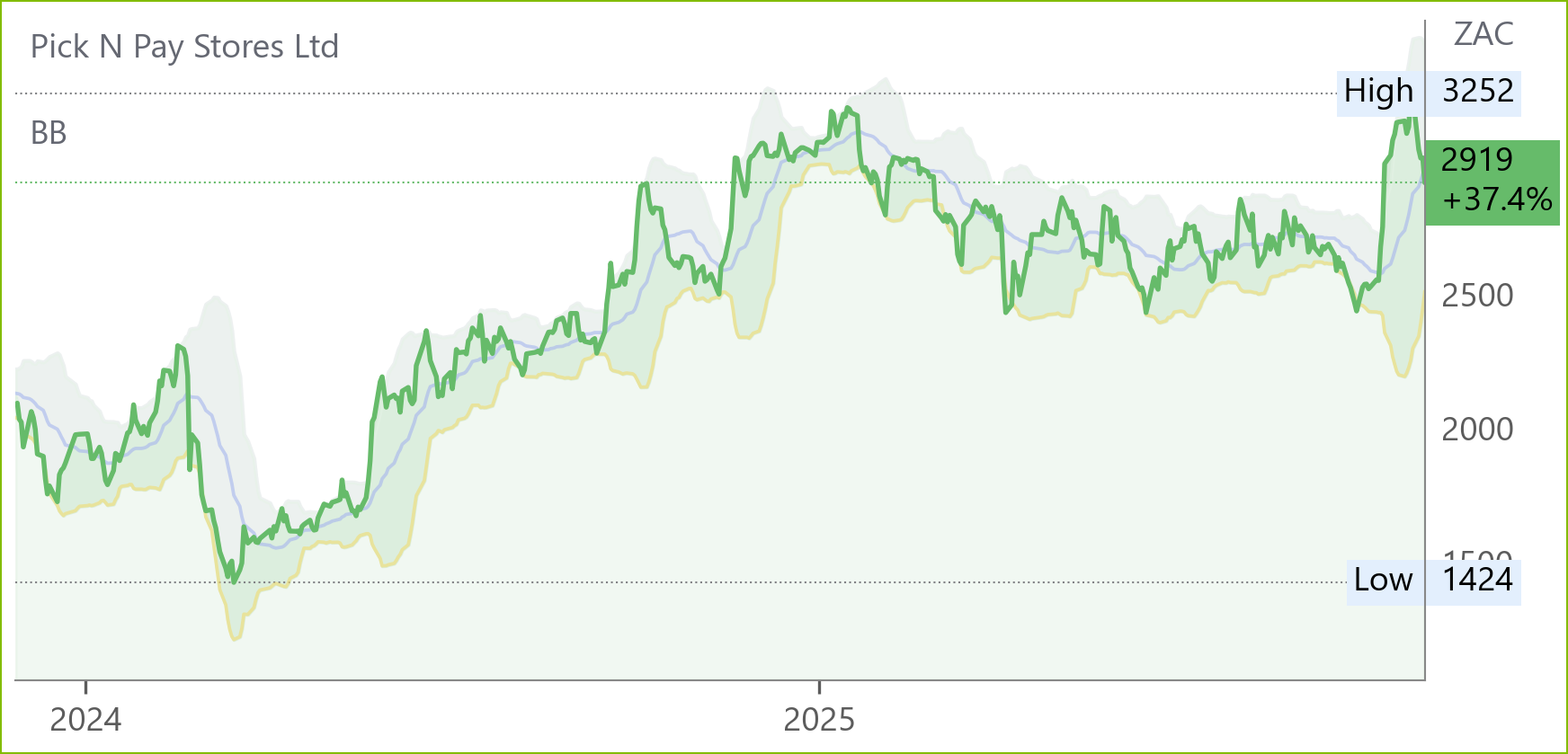

Pick n Pay (PIK) Interim Results for 26W FY26 (2830c)

HEPS: (59.77c) (↑56.2% from H1 FY25)

EPS: (67.53c) (↑52.0% from H1 FY25)

Operating Profit: R310m (↑273.5% from R83m)

Revenue: R58.8bn (↑4.9% from R56.1bn)

HEPS and EPS losses narrowed significantly due to a R227m increase in trading profit and a R537m improvement in net funding costs, reflecting the benefits of the FY25 recapitalisation. Boxer’s trading profit rose 16.2% to R931m, while Pick n Pay’s trading loss improved 13.5% to R621m.

Boxer delivered 13.9% turnover growth, reinforcing its position as South Africa’s leading grocery discounter. Pick n Pay’s like-for-like sales rose 4.8% in company-owned stores, with gross margin recovering 0.4%. The group closed or converted 65 loss-making stores, while Pick n Pay Clothing expanded to 400 stand-alone outlets, achieving 12% turnover growth. Online sales posted double-digit growth. Group loss before tax narrowed 69.9% to R317m. Net finance costs fell 44.8% to R627m.

Boxer will continue its aggressive store rollout, capitalising on structural growth opportunities. Pick n Pay’s recovery remains in progress, with full-year trading losses expected to mirror FY25 as investments in retail capabilities continue. “We are rebuilding and energising the Group for a prosperous future,” said Sean Summers, CEO. The Group remains focused on restoring Pick n Pay to profitability through methodical execution of its strategic plan.

Comment: CEO Summers opened the results presentation by saying that in the 15 months since the plan was launched it had proven to be exactly what was needed. “Are we on track? Absolutely! Are we where we want to be? Hell no! But we’ve bought our tickets, we are in the cable car at the bottom of Table Mountain and are on the way to the top.” Investments in retail capabilities includes “finding and training great bakers and butchers and training retailers which has to be in house as they don’t come out of universities. We’re building a long term business and there are no short cuts.”

Among the many actions are the reinvigoration of Pick and Pay’s erstwhile reputation for fresh quality food and substantial closure of dud stores. The Springbok franchise is taken very seriously as a symbol of success through cooperation and carried through to CSI level.

The reversal of the like for like market share decline allows top line growth to cope with skills investment. Management is very happy with its Boxer investment and has no intention of reducing its 65.6% holding. While ultimate success is assured, we think waiting for the FY26 results for a better line of sight as to the resumption of profitability will be worthwhile. Notwithstanding this, Pick n Pay’s holding of Boxer’s 457.407m shares is, at 7765c per Boxer share, worth R38.3bn. Pick n Pay’s own market cap, with its 745.657m shares at 3035cps is, however, only R23.3bn. Simplistically, therefore, the market is ascribing a big negative value to Pick n Pay which, despite the likelihood of lossmaking years ahead is, in our view, overdone making the share a BUY.

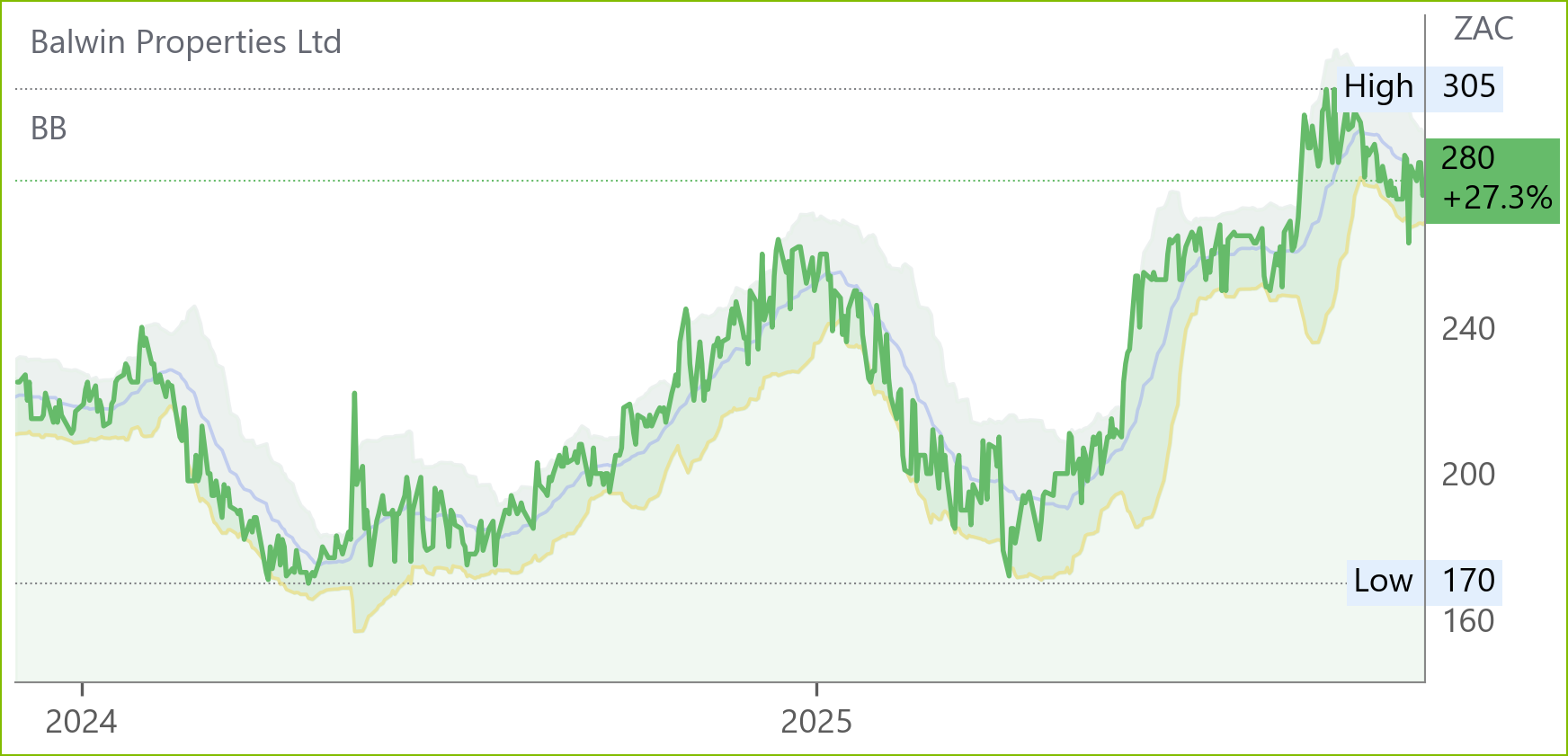

Balwin Properties (BWN) Interim Results for 6M Aug 25 (280c)

HEPS: 20.91c (↑29% from 16.21c)

EPS: 20.91c (↑28% from 16.34c)

HEPS and EPS rose nearly 30% due to a 51% increase in apartment sales and 45% more handovers, supported by improved consumer demand and easing interest rates. Revenue from Balwin Annuity also grew 55%, contributing 8.3% to group revenue.

Apartment handovers rose to 928 units, driving revenue to R1.2bn. Gross margin declined to 29% due to the absence of land sales, though apartment margins held steady at 23%. Balwin Annuity continued its growth trajectory. Cash improved to R303.4m, and the loan-to-value ratio reduced to 39.3%. No dividend was declared as the board prioritises debt reduction. Cost control and operational alignment with sales trends remained key focuses during the period. The board will reassess dividend declaration at FY26 year-end.

Comment: the weak 1H25 and strong 2H24 Heps puts Balwin on a trailing PE of 5.8x

and, with a discount to NAV of 69% it would appear to be cheap. Although a year-end dividend will be considered, the board may well, however, decide to defer as the Western Cape, which contributed 51% of the apartments’ sales revenue, comprised only 12.6% of the 35 068 units for sale in Balwin’s development pipeline. Management reckons therefore that the Western Cape only has a 3 year development pipeline as opposed to 10 years for Gauteng. The chances are, therefore, that the board may well decide to buy some land there but not nearly enough to prevent Balwin from becoming a play on a business friendly outcome of the 2027 local government elections boosting Gauteng economic growth. In a post results interview on BIZ News a decidedly upbeat CEO Steve Brookes confirmed the intention to buy Western Cape land but also as good as admitted that a dividend was unlikely as Balwin needs to get its too high debt down.

He also said government (presumably Gauteng) would repay the R7 1 million it had spent on infrastructure. We have no doubt, however, that this will have to await improved provincial finances which again plays to the notion that, although Balwin

Is well run and has excellent properties, investors do not have to anticipate the share price closing that 69% NAV discount just yet.

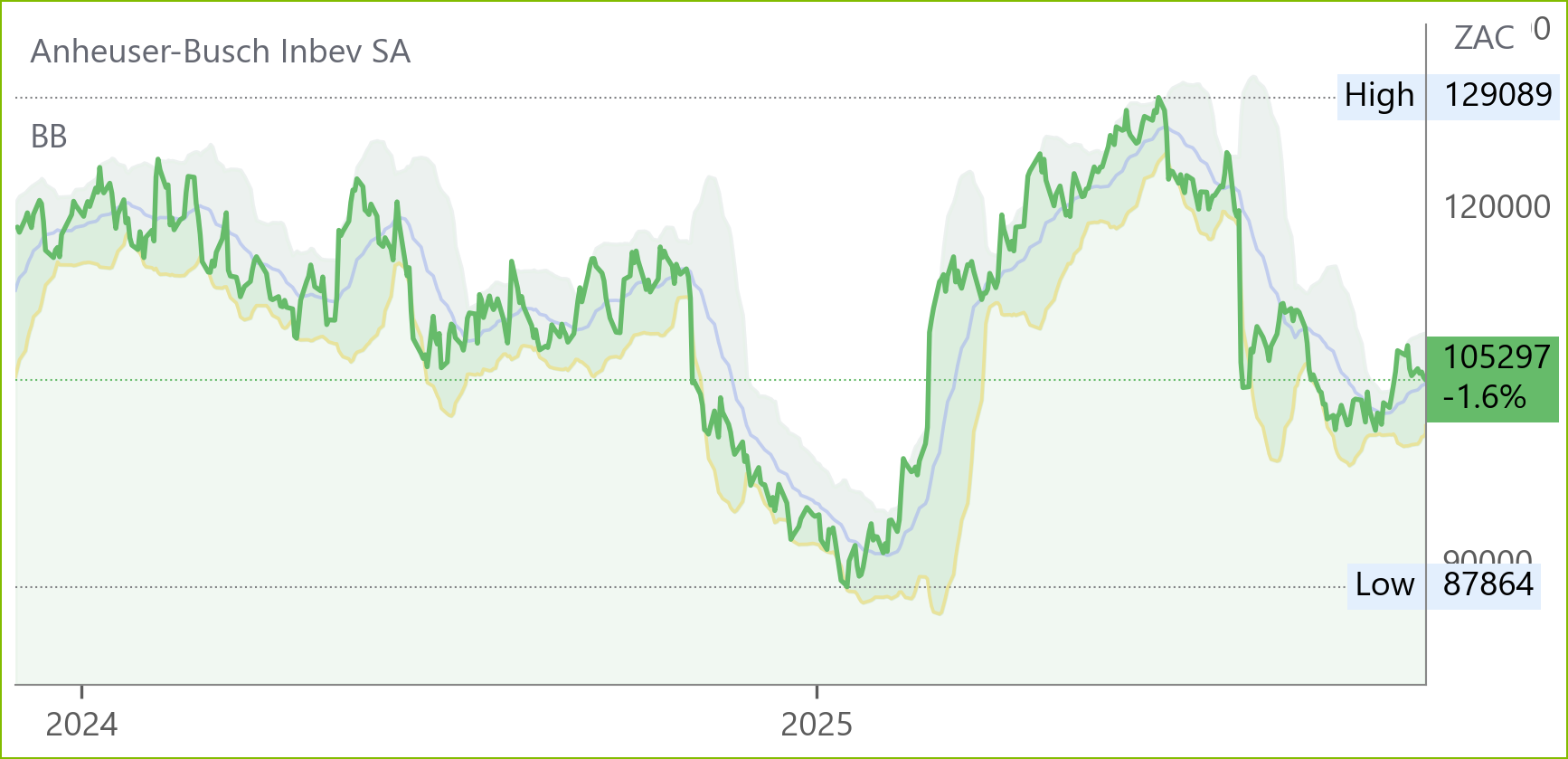

AB InBev (ANH) Interim Results for 9M Sep 25 (105297c)

HEPS: 2.78 USD (5.4% from Sep 24)

EPS: 0.99 USD (1.0% from Sep 24)

Operating Profit: Not disclosed

Revenue: 43.76bn USD (-2.6% from Sep 24)

EBITDA: 15.75bn USD (5.8% from Sep 24)

Dividend: 0.15 EUR per share

Corona led megabrand growth with 6.3% uplift outside its home market. No-alcohol beer revenue surged 27%. BEES Marketplace GMV rose 66% to 935m USD. Volumes declined 3.7% in Q3, impacted by beer (-3.9%) and non-beer (-2.2%) softness. Currency headwinds affected reported revenue. Share buyback of 6bn USD and 2bn USD bond redemption announced. Interim dividend of 0.15 EUR declared, payable 20 Nov ‘25.

FY25 EBITDA expected to grow 4–8%. Net finance costs guided at 190–220m USD per quarter. Normalised tax rate forecast at 26–28%. Capex range set at 3.5–4.0bn USD. Michel Doukeris, CEO, stated: “We remain focused on executing our strategy and delivering consistent performance, while investing in long-term growth and shareholder returns.”

Comment: these results beat forecasts by consensus which endorses the company’s pivot to non-alcoholic beverages as well as craft beer in some markets. Management is confident it can take advantage of changing tastes in these markets while continuing to benefit from those where beer Is still growing. It remains a HOLD for long term investors needing global diversification.

Dis-Chem (DCP) Interim Results for 6M Aug 25 (3391c)

HEPS: 73.8cps (9.0% from Aug 24)

EPS: 73.9cps (9.6% from Aug 24)

Revenue: R21.3bn (8.7% from Aug 24)

Dividend: 29.42cps

Better Rewards launched 21 Oct ‘25, incentivising chronic treatment adherence and healthy behaviour. X, bigly labs drove innovation, enabling data-led promotional strategies and omnichannel retailing. Dis-Chem Life expanded its footprint, with 40% of ecosystem investment directed to brand and operational scale. Retail pharmacy footprint grew to 302 stores, with 17 new openings. Wholesale network now services 1,608 independent pharmacies, representing 85% of the market. Inventory days reduced from 90.5 to 85.8, unlocking R374m in working capital.

Revenue for Sep–Oct ‘25 rose 9.7% year-on-year. FY26 priorities include 32 new store openings, omnichannel retail design, and a new app launch in mid FY27. Strategic partnerships, including Capitec, aim to broaden mass market access. Rui Morais, CEO, stated: “We are building a smarter and more connected health ecosystem where technology and customer obsession converge to create meaningful value.”

Comment: Rui Morais was CFO from 2012 and learnt from his mentor and, predecessor, Ivan Saltzman who, with his wife Lynette, founded Dischem with one store in 1978. Since becoming CEO in July 2023 the changes and initiatives put in place have been far reaching, fundamental, comprehensive, bold and, no doubt the result of years of observation. Coordination, monitoring, and innovation is data driven at the centre by

the tech hub, XBigly labs. Initiatives like life assurance, the strategic partnership with Capitec are accompanied by rapid expansion at the physical level such that with the F25 expansion of 20 stores with 22439m² the FY27 pipeline comprises 143981m² and 163 stores. This could well bear spectacular fruit in future, but the market is already rating it accordingly so we suggest awaiting better buying opportunities.

Datatec (DTC) Interim Results for 6M Aug 25 (7189c)

HEPS: 22.0cps (109.5% from Aug 24)

EPS: 21.7cps (92.0% from Aug 24)

Revenue: US$1.84bn (2.9% from Aug 24)

Gross Profit: US$483.4m (11.7% from Aug 24)

EBITDA: US$139.0m (35.6% from Aug 24)

Dividend: 175cps

HEPS and EPS more than doubled, driven by margin expansion in Westcon and strong operating leverage in Logicalis International. EBITDA rose 35.6% due to improved cost control and higher software/services mix.

Westcon’s recurring software and services mix expanded, while Logicalis International delivered excellent performance. Latin America showed considerable improvement. AI-driven infrastructure demand boosted cybersecurity and data centre solutions. Datatec broadened investor access via OTCQX listing and launched share repurchase programmes. Dividend cover policy was reduced from 3x to 2x, enabling a 133.3% increase in interim dividend. Inventory and cost discipline supported EBITDA conversion.

Trading conditions remain favourable, with higher-margin software and services driving profitability. Jens Montanana, CEO, stated: “Continued margin expansion and strong operating leverage supported further improvement in the quality of Datatec’s earnings… all promising better performance in FY26.”

Comment: Between Logicalis and Westcon, Datatec covers vast swathes of North America, Western Europe, the Middle East, China, SE Asia and Asia Pacific. These interims confirm Jens Montana’s prediction that the strong performance of 2H 25 would continue in FY26. We believe his renewed confidence at these interims will be again be borne out by at least a repetition of the 1H HEPS of USD22c which, at ZAR 17.29 would make for ZAR 761cps and a 6 month FPE of 9.3x. Although overall product sales revenue was 18.7% up and services and annuity services revenue only 8.6% up there is little doubt that the work on AI solutions and cyber security is at more favourable margins. We believe this is a good opportunity to participate in a global player in the AI transition and recommend investors consider choosing the scrip alternative for the cash dividend. The price will be based on the VWAP for the 30 day trading period to 30 November day with election on 5h December.

Adcorp (ADR) Interim Results for 6M Aug 25 (720c)

HEPS: 53.0cps (up 87.6% from Aug 24)

EPS: 53.0cps (up 87.6% from Aug 24)

Operating Profit: R72.2m (up 70.7% from Aug 24)

Revenue: R6.39bn (-5.5% from Aug 24)

Gross Profit: R624.0m (-3.7% from Aug 24)

Dividend: 24.77681cps

HEPS and EPS nearly doubled due to improved operating efficiencies, cost discipline, and the absence of prior year once-off transformation costs.

Adcorp exited lower-margin activities and faced softer demand in automotive, permanent placement, and Australian protein-processing sectors. Despite this, gross margin improved to 9.8%. Net unrestricted cash closed at R201.5m after R52.2m in dividends. Days sales outstanding rose to 40 days, impacting working capital. Tax rate dropped to 10.6% due to utilisation of assessed losses and tax incentives. Interim dividend increased 85% year-on-year.

Second-half outlook is cautiously optimistic, with expected GDP recovery supporting demand in logistics, manufacturing, and consumer sectors. Australia remains steady, with diversification into healthcare and hospitality.

Operating Updates & Trading Statements

Anglo American (AGL) Production Report for Q3 Sep 25 (65667c)

Copper production rose 1% YoY to 184 kt, driven by higher grades at Quellaveco and Los Bronces, offsetting lower output at Collahuasi. Iron ore fell 9% to 14.3 Mt due to a planned pipeline inspection at Minas-Rio, which was completed ahead of schedule. Manganese surged 140% to 973 kt following cyclone recovery. Diamond output rose 38% to 7.7 Mct, led by Jwaneng. Steelmaking coal dropped 54% to 1.9 Mt due to the Moranbah North incident and Jellinbah sale. Nickel rose 2% to 10.1 kt on higher grades.

Portfolio simplification accelerated with the $2.5bn sale of Valterra Platinum and on divesting Nickel and De Beers. The proposed merger with Teck will create a copper-focused critical minerals leader with over 70% copper exposure. Operational synergies are expected from the Los Bronces–Andina joint mine plan. Minas-Rio FY25 guidance was raised to 23–25 Mt. Duncan Wanblad, CEO, stated: “We’ve delivered another solid quarter… our agreement to merge with Teck represents our next major strategic step to accelerate value accretive growth. Results due 20 Feb ’26.

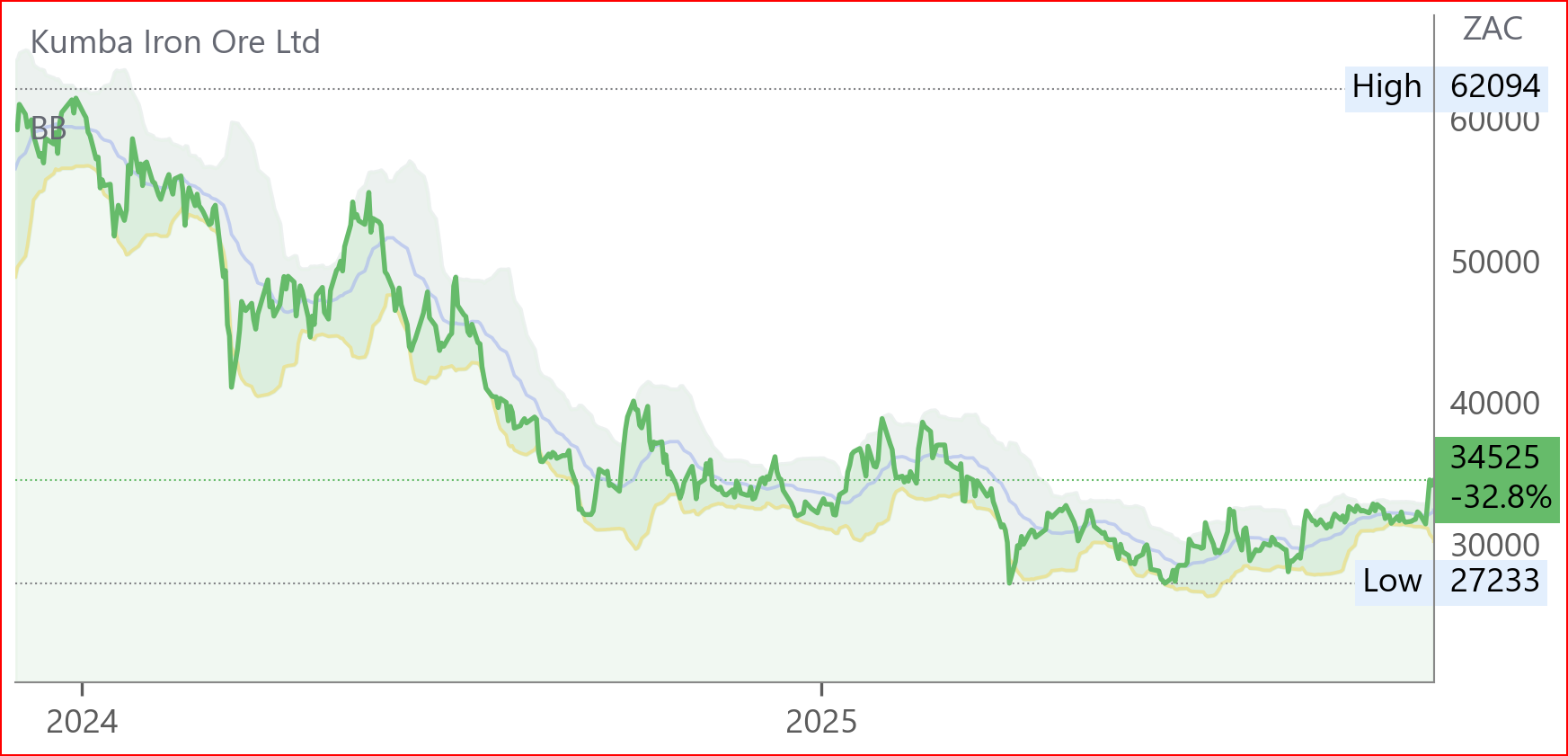

Kumba (KIO) Production and Sales Report for Q3 Sep 25 (34525c)

Total iron ore production declined 2% YoY to 9.2 Mt due to maintenance at Sishen ahead of UHDMS integration. Kolomela output rose 8% to 2.9 Mt, offsetting Sishen’s 6% drop. Sales increased 7% to 9.6 Mt, supported by improved rail performance and port stock levels. Waste mining rose 12% to 44.2 Mt, driven by equipment efficiency gains. Realised FOB export price held at US$94/wmt, 12% above benchmark. TRIFR improved to 0.97, maintaining a fatality-free record at both mines.

Progress continues on UHDMS construction, expected to treble premium-grade output at Sishen. Full-year guidance remains unchanged at 35–37 Mt for both production and sales. CEO Mpumi Zikalala stated: “Improved logistics stability has contributed to performance… positioning us well to deliver on our market guidance for the full year.”

Glencore (GLN) Production Report for Q3 FY25 (8308c)

Copper production rose 36% QoQ in Q3 25, driven by higher grades at KCC (+66%), Mutanda (+60%), Antamina (+52%), and Antapaccay (+66%). Despite this, YTD copper output fell 17% YoY due to lower head grades and recoveries. Steelmaking coal surged 123% YoY, largely due to EVR’s contribution post-acquisition. Ferrochrome dropped 51% following smelter suspensions. Nickel declined 16% YoY, while cobalt and zinc rose 8% and 10% respectively.

Water restrictions at Collahuasi eased with the commissioning of a new desalination plant. The Mount Isa copper mine ceased operations in Jul 25, shifting smelting to third-party feedstocks. The Pasar copper smelter sale was completed in Sep 25. DRC cobalt export quotas were reinstated, with Glencore allocated 4kt for Q4 25. Excess cobalt will be stored in-country. Full-year copper guidance was tightened to 850–875kt. CEO Gary Nagle stated: “Underpinned by a strong third quarter production performance, particularly in copper and coal, full-year 2025 production guidance for our key commodities has been maintained.” Glencore will prioritise copper over cobalt in the DRC while quotas remain.

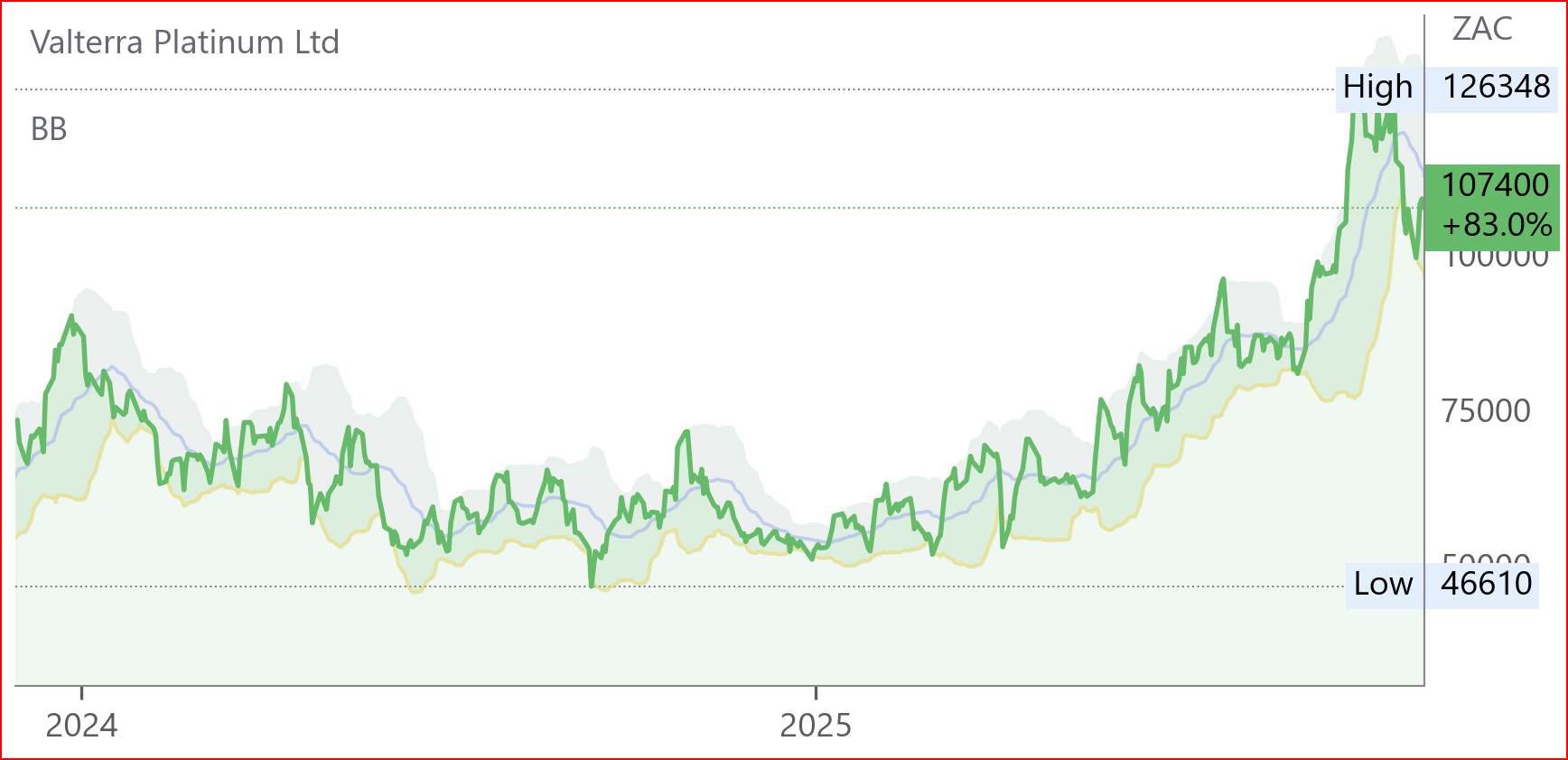

Valterra Platinum (VAL) Production Report for Q3 Sep 25 (107400c)

Refined PGM production declined 11% to 981,500 ounces due to lower work-in-progress drawdown and Kroondal’s transition to tolling. Own-mine PGM output fell 2% to 539,600 ounces, impacted by lower grades and volumes at Mototolo, Unki and Amandelbult, partially offset by Mogalakwena’s 4% increase. PGM sales volumes dropped 15% to 936,800 ounces, with timing delays rolling some volumes into Oct. Toll-refined PGMs rose 40% to 215,700 ounces. Chrome output increased 10% to 271,000 tonnes. Nickel and copper declined 15% and 9% respectively.

Amandelbult’s Tumela section reached steady-state production ahead of schedule, supporting a 118% QoQ recovery. Full-year guidance remains at 3.0–3.2 million ounces M&C and ~3.4 million refined PGMs. The Q3 realised basket price rose 30% YoY to US$1,916/oz, driven by macroeconomic resilience, inflation hedging, and Chinese demand.

CEO Craig Miller stated: “It is pleasing to see the continued recovery in our quarterly M&C production volumes… we maintain our full year guidance for Amandelbult of 450,000–480,000 PGM ounces.”

WeBuyCars (WBC) Trading Statement for FY 25 (4600c)

HEPS: 222.3c–226.9c (↑>100% from FY24)

EPS: 221.8c–226.4c (↑>100% from FY24)

HEPS and EPS more than doubled due to the absence of once-off listing costs and derivative losses that impacted FY24. FY25 earnings reflect core operational strength, with headline earnings rising from R343.9m to ~R940m. Share issuance during FY24 diluted per-share metrics slightly, but underlying earnings grew robustly.

WeBuyCars completed its first full year as a JSE-listed entity, with strong core headline earnings of R917m–R958m. Shareholder dilution from pre-listing capital raises impacted CHEPS, but operational momentum remained intact. The derecognition of a R426.5m derivative asset and R45m listing costs in FY24 no longer weighed on results. A minor R2.2m loss on asset sales was the only adjustment in FY25. Share count rose to 417.7m, reflecting strategic expansion.

Management remains focused on scaling its digital and physical footprint, with continued investment in inventory, logistics, and customer experience. The Board expects sustained earnings growth, supported by robust demand and operational leverage. “WeBuyCars is well-positioned to deliver long-term value as we deepen our market presence and enhance customer engagement,” said Faan van der Walt, CEO. Results due 17 Nov ’25.

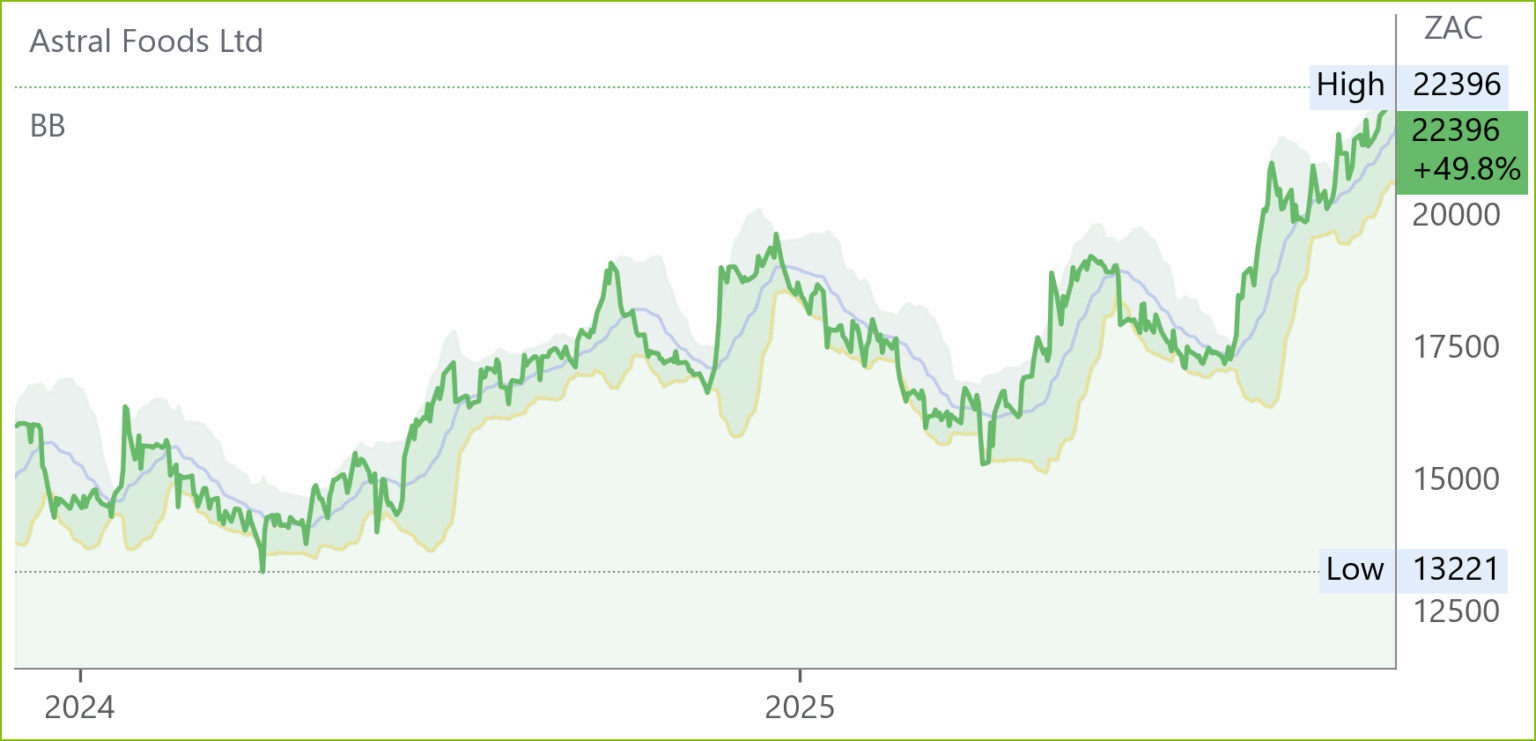

Astral Foods (ARL) Trading Statement and Operational Update for FY25 (22396c)

HEPS: 2 016–2 208cps (↑5–15% from FY24)

EPS: 2 096–2 291cps (↑7–17% from FY24)

EPS and HEPS driven by increased broiler slaughter numbers, higher poultry sales, improved per-unit production costs, and better poultry sales realisations following prolonged price deflation. Internal and external feed sales volumes also rose, supported by sound procurement in volatile commodity markets and improved poultry farming performance.

Astral focused on rebuilding its balance sheet, successfully restoring a surplus cash position. Operational efficiencies and volume-driven cost improvements supported profitability. The group maintained its best-cost strategy despite volume-related increases in variable expenses. Improved farming metrics lowered feeding costs and enhanced broiler live cost outcomes. Results Due 17 Nov ’25.

Quantum Foods (QFH) Trading Statement and Operational Update for FY25 (775c)

HEPS: 127.4c–143.4c (↑58%–78% from FY24)

EPS: 129.9c–145.9c (↑62%–82% from FY24)

HEPS and EPS surged due to recovery in layer flock, increased feed and livestock volumes, improved operational efficiency, and minimal load shedding. Strong performance in Zambia and Uganda also contributed positively.

Egg supply rose 79%, enabling reactivation of Pinetown packing station. Despite high volumes, earnings from eggs declined due to a 17% drop in average selling prices. Broiler farming excelled, supported by genetic gains and cost control. Feed volumes increased 9%, aided by recovery at Pretoria mill and repairs at Malmesbury. Mozambique operations were disrupted by civil unrest and looting. A R10m environmental penalty was levied for legacy non-compliance at Eggland farm; appeal pending.

Quantum expects continued recovery across operations, with expansion at Malmesbury feed mill on track for Q2 FY26. Results due 28 Nov ’25.

Orion Minerals (ORN) Quarterly Activities Report for Sep ’25 (20c)

Orion advanced its transition from developer to producer across its South African copper-zinc assets. A non-binding term sheet was signed with Glencore for US$200–US$250 million in funding and concentrate offtake for the Prieska Copper Zinc Mine (PCZM). Operational readiness progressed with shaft dewatering, infrastructure upgrades, and recruitment of key personnel including Johan van Dyk as Project Director. At Okiep Copper Project (OCP), geological modelling incorporated eight new prospects. A$8.6 million was raised post-quarter via share placement, with a second tranche pending shareholder approval on 27 Nov ’25.

Orion aims to commence Upper-Level production in month 13 and Deeps mining by month 28, targeting >30ktpa copper and >65ktpa zinc at steady state. CEO Tony Lennox stated: “This was a watershed moment for the Company and our shareholders… Orion will move towards the close of 2025 in a position of strength, firmly on track to make the transition to developer and producer by the end of 2026.” The company continues to optimise its execution plan, including BOOT plant tenders and revised mining schedules. Results due 27 Nov ’25.

Merafe (MRF) Production Update for 9M Sep 25 (110c)

Ferrochrome production fell 51% due to smelter suspensions triggered by adverse market conditions. Chrome ore output declined 3% following temporary equipment breakdowns. PGMs concentrate production rose 6%, driven by higher feed tonnages.

Production from the Glencore Merafe Chrome Venture was significantly impacted by weak market demand, prompting operational curtailments. Smelter shutdowns reduced ferrochrome volumes to 709kt, while chrome ore output reached 267kt. PGMs concentrate rose to 4koz, reflecting improved plant throughput. The venture remains focused on cost containment and operational flexibility amid volatile commodity pricing.

Renergen (REN) Trading Statement Update for 6M Aug 25 (1638c)

HEPS: (86.6c to 95.7c loss) (↑89% to ↑109% from 45.73c loss)

EPS: (86.6c to 95.7c loss) (↑89% to ↑109% from 45.73c loss)

Losses widened due to once-off transaction costs linked to the ASP Isotopes combination, full commissioning of Phase 1 plant which increased depreciation, and a shift from capitalised to expensed costs. Interest expense also rose. Phase 1 of the Virginia Gas Project was fully commissioned during the period, marking a key operational milestone. The plant’s transition to full depreciation and cost recognition reflects its move into commercial operation.

Results will be released on 31 Oct ’25.

Snippets

FirstRand (FSR) will acquire 20.1% of Optasia, a leading AI-powered fintech platform, concurrent with Optasia’s JSE IPO. The investment supports FirstRand’s strategy to expand financial access in underbanked markets across Africa, the Middle East, and Asia. Optasia’s scalable micro-lending model and mobile data-driven collections align with First National Bank’s growth ambitions in underserved segments. Deal announced 27 Oct ’25.

Curro (COH) confirmed progress on its proposed delisting via a scheme of arrangement led by Jannie Mouton Stigting. Key regulatory and funding approvals have been secured, with Competition Authority submissions pending. The scheme consideration now reflects a 74% premium to Curro’s share price. Shareholders will vote at a general meeting on 31 Oct ’25, with proxy forms due 29 Oct ’25.

Aspen Pharmacare (APN) has resolved a major contractual dispute with a customer over an mRNA manufacturing and technology agreement. The settlement involves a payment of EUR 25 million (approximately ZAR 500 million) to Aspen by 1 December 2025. This follows earlier announcements and concludes the matter in full and final terms.