Global Indices

Currencies, Crypto & Commodities

SA Indices

SA Upcoming Indicators & Dividends

Jubilee Metals (JBL) Interim Results for 6M Dec

HEPS: (0.40c) (↓ from 0.06c)

EPS: (0.34c) (↓ from 0.07c)

Operating Loss (US4.2m) (down 28% from loss US$5.9m)

Revenue: US$14.1m (↑70.5% from US$8.3m)

Gross Profit: US$3.1m (↑847.6% from US$0.3m)

EBITDA: US$7.8m (↓42.6% from US$13.6m)

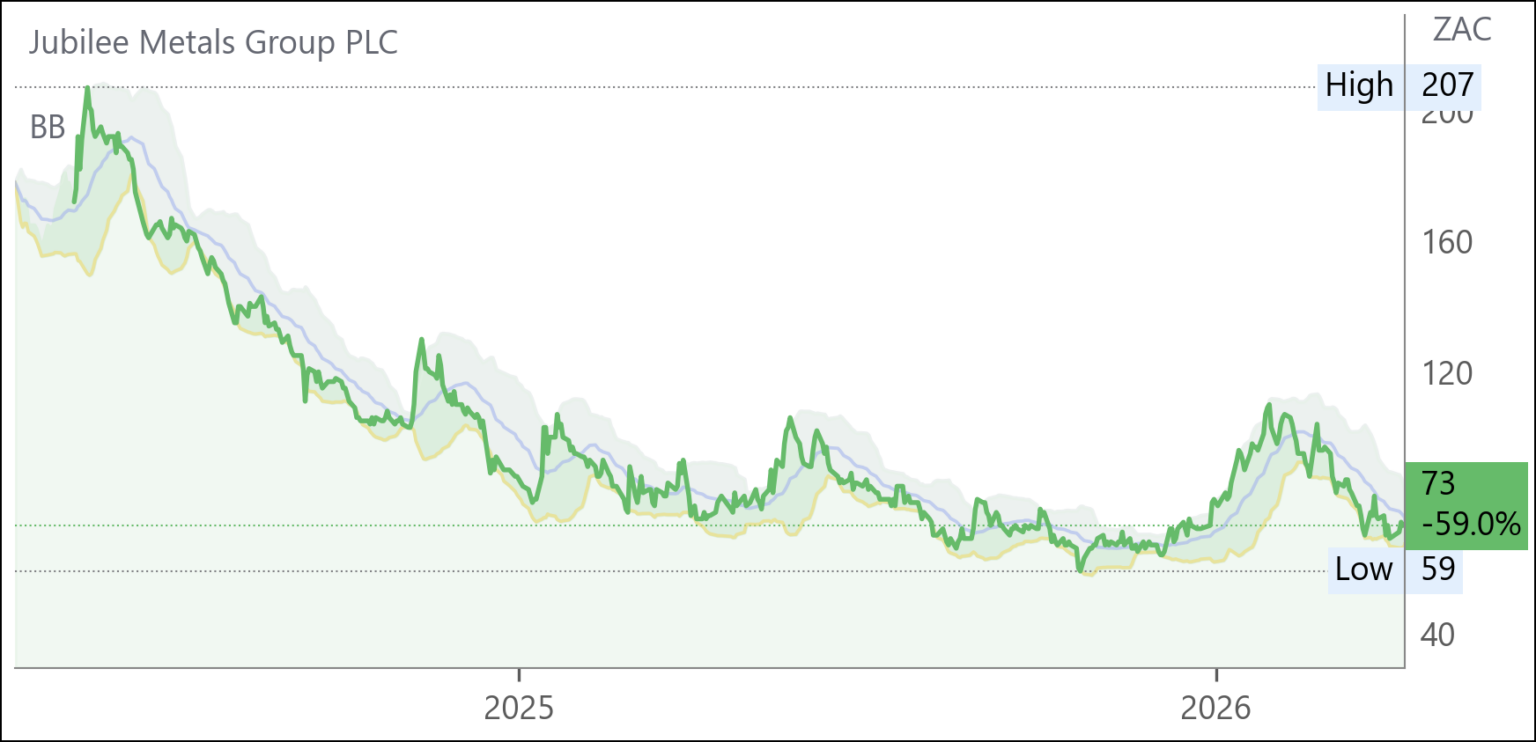

Copper output rose 8.7% to 1 543t, driven by Roan’s 172.8% surge. Disposal of South African chrome and PGM assets delivered US$19m cash, strengthening the balance sheet. Net cash improved to US$11.5m. Heavy rains at Molefe Mine and delays in dewatering commissioning temporarily constrained output. “This transition strengthens the Group’s balance sheet, simplifies the business and positions Jubilee to accelerate the delivery of its scalable, integrated copper strategy in Zambia.” – Leon Coetzer, CEO.

Comment: there are many moving parts in Jubilee’s transition from an SA based processing-led model to a Zambian resource-backed mining business and the 22.7% debt:equity ratio (1H 25: 14.2%) will be helpful. Management plans updates on the various projects the first of which will be on the Molefe mine. At interims therefore management may well be able to give guidance on production timelines and capex. Like any small developer with great assets, it takes time to get all these ducks in a row and Jubilee is no exception. So, although the stock remains well worth watching, there is no need to buy now.

Nu-World (NWL) Interim Results for 6M Feb ’26 (2880c)

HEPS: 227.7c (+29.9% from 175.4c)

EPS: 227.6c (+29.3% from 176.1c)

Revenue: R1.28bn (+2.6% from R1.25bn)

NAV: 7 511.4c per share (-0.6% from 7 559.3c)

Earnings rose nearly 30% on modest revenue growth, reflecting improved margins and operational efficiency. Net asset value dipped slightly, signalling balance sheet pressure despite profit gains. CEO J.A. Goldberg emphasised continued focus on brand distribution across international subsidiaries. “Nu-World remains committed to delivering shareholder value through disciplined execution and resilient trading performance.” – J.A. Goldberg, CEO.

Purple (PPE) Interim Results for 6M Feb ’26 (199c)

HEPS: 2.86c (+21% from 2.36c)

EPS: 2.86c (+21% from 2.36c)

Operating Profit: R78.7m (+33.3% from R59.0m)

Revenue: R258.5m (+8.8% from R237.5m)

Easy Group drove growth with revenue up 18.5% and profit before tax up 66.3%. Client assets rose 41.2% to R94.9bn, with retail inflows up 51%. Expansion highlights include EasyRetire scaling, (They have 2.8m registrations but only 1m active clients with renewed interest from old registrations and higher conversion rates) EasyETFs surpassing R2bn AUM, and entry into the Philippines. ZARU stablecoin partnership and AI acquisition plans signal diversification. “Operating leverage is not emerging. It is extending rapidly.” – Charles Savage, CEO.

Trading Statements & Updates

Combined Motor Holdings (CMH) Trading Statement FY26 (3914c)

HEPS: 504.0c – 544.3c (+25% to +35% from 403.2c)

EPS: 503.9c – 544.2c (+25% to +35% from 403.1c)

HEPS and EPS are both expected to rise by 25–35%. This reflects strong trading momentum across CMH’s automotive retail operations. Management highlighted resilience in consumer demand despite macroeconomic pressures. Results due 28 Apr ’26.

Snippets

FirstRand (FSR) raised its total provision for the UK FCA’s motor finance redress scheme to £750m (c.R17.7bn), including £510m newly booked. Management argues the scheme is disproportionate, diverging from the UK Supreme Court’s Johnson ruling, and may constrain capital for MotoNovo. Despite this, group capital ratios remain above targets. Normalised earnings post-provision are expected to contract 10–15%, with ROE below guidance. FirstRand warned it may reconsider UK consumer finance exposure, while Aldermore remains resilient.