Finova Investor Digest

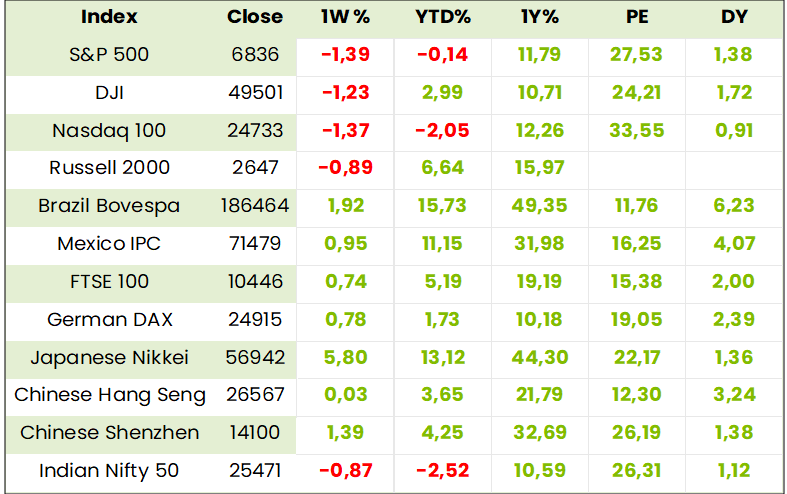

Global Indices

Currencies, Crypto & Commodities

SA Indices

SA Upcoming Indicators

SA Equity

AB InBev (ANH) Financial Results for FY25 (127171c)

HEPS: 3.61 USD (+19% from 3.04 USD)

EPS: 3.73 USD (+6% from 3.53 USD)

Operating Profit: 7 410m USD (+5% from 7 061m USD)

Revenue: 59 320m USD (‑0.8% from 59 790m USD)

EBITDA: 21 223m USD (+4.9% from 20 220m USD)

Dividend: €1.15 per share (final €1.00 + interim €0.15)

Headline earnings rose strongly, supported by margin expansion and disciplined capital allocation. Volumes fell 2.3% but pricing gains offset currency headwinds. Free cash flow reached USD 11.3bn, with net debt/EBITDA improving to 2.87x. A €1.15 dividend was proposed, alongside a USD 6bn buyback programme.

“Beer plays an important role in bringing people together… we exit 2025 with improved momentum and enter 2026 well positioned.” – Michel Doukeris, CEO.

Comment: lower volumes were in line with the declining trend in global beer consumption and were partially offset by growth in non-alcoholic beverages. Like Heineken which has said it will cut 7000 of its 87000 work force, ABInBev and Carlsberg have also said they will cut jobs, but CEO Doukeris also talks of “improved momentum” and 4 to 6% growth in ebitda for FY26. With consensus forecasting double digit underlying EPS growth the stock remains a useful Rand hedge for long term SA portfolios.

British American Tobacco (BTI) Preliminary Results for FY25 (94845c)

HEPS: 361.0p (+19% from 304.0p)

EPS: 349.1p (+157% from 135.9p)

Operating Profit: £9 997m (+265% from £2 737m)

Revenue: £25 610m (‑1% reported, +2.1% constant FX)

Gross Profit: +2.1% (adjusted)

Dividend: 245.04p per share (+2%)

EPS surged due to settlement provision movements, while HEPS rose steadily. New Categories revenue grew 7% to £3.6bn, now 18.2% of group revenue, with Velo Plus delivering triple‑digit growth. Smokeless consumers increased by 4.7m to 34.1m. Free cash flow fell 49% to £4bn, but leverage improved to 2.48x.

Momentum in smokeless and resilient combustibles underpin confidence. “I am pleased with our accelerating momentum through 2025, enabling full‑year delivery at the top end of our guidance… we are confident in sustainably delivering on our financial algorithm.” – Tadeu Marroco, CEO.

Comment: new categories revenue growth would come much closer to stabilising total revenue growth were it not for the widespread and substantial volumes of illicit trade. The preliminary results mention Australia and Bangladesh in particular and, despite the fact that SA operations are likely to be closed with 5000 job losses, no mention was made of this. It is also a problem in the US, but management is confident of efficient enforcement at federal and state levels in the near future. Not all jurisdictions are lax and in France, for example, revenue collection is efficient. Despite the likelihood that efficient enforcement will take time, management is confident in achieving its financial guidelines which include adjusted diluted EPS growth of 5-8% per annum. This in turn means it is likely to consolidate at the new high levels at which it has traded since mid-25 and, in due course, move on from there.

Operating Updates & Trading Statements

Northam (NPH) Trading Statement and Update for 6M Dec ’25 (37050c)

HEPS: 1 518.5c–1 529.5c (>1 000% from 61.1c)

EPS: 2 000.5c–2 011.5c (>1 000% from 61.5c)

Operating Profit: R5.8bn (+439% from R1.1bn)

Revenue: R23.3bn (+60% from R14.5bn)

EBITDA: R7.5bn (+317% from R1.8bn)

PGM output rose 3.7% to 468k oz, chrome concentrate increased 14.8% to 823k tonnes, and sales volumes grew 13.7%. Safety milestones were achieved across all operations, with Booysendal surpassing 12m fatality-free shifts. Net debt fell to R2.6bn, supported by R9.3bn cash and undrawn R12.3bn facilities. Renewable energy projects, including an 80MW solar plant at Zondereinde, are advancing. “Northam’s high-yielding assets and growth strategy position us to expand market share in PGMs and chrome while delivering shareholder value.” – Paul Dunne, CEO. Results due 27 Feb ’26

Pan African Resources (PAN) Trading Statement for 6M Dec 25 (3098c)

HEPS: 7.28–7.40 USc (+507–517% from 1.20c)

EPS: 7.18–7.43 USc (+187–197% from 2.50c)

Revenue: +157.3% (driven by gold price and volumes)

Revenue surged over 150% due to a 61.6% increase in the average gold price to US$3,812/oz and 51.5% higher production at 128,296oz.

Production expansion from Tennant Mines and MTR projects supports FY26 guidance of 275,000–292,000oz. “Pan African is well positioned to deliver sustainable growth and shareholder returns, supported by strong fundamentals and disciplined capital allocation.” – Cobus Loots, CEO.

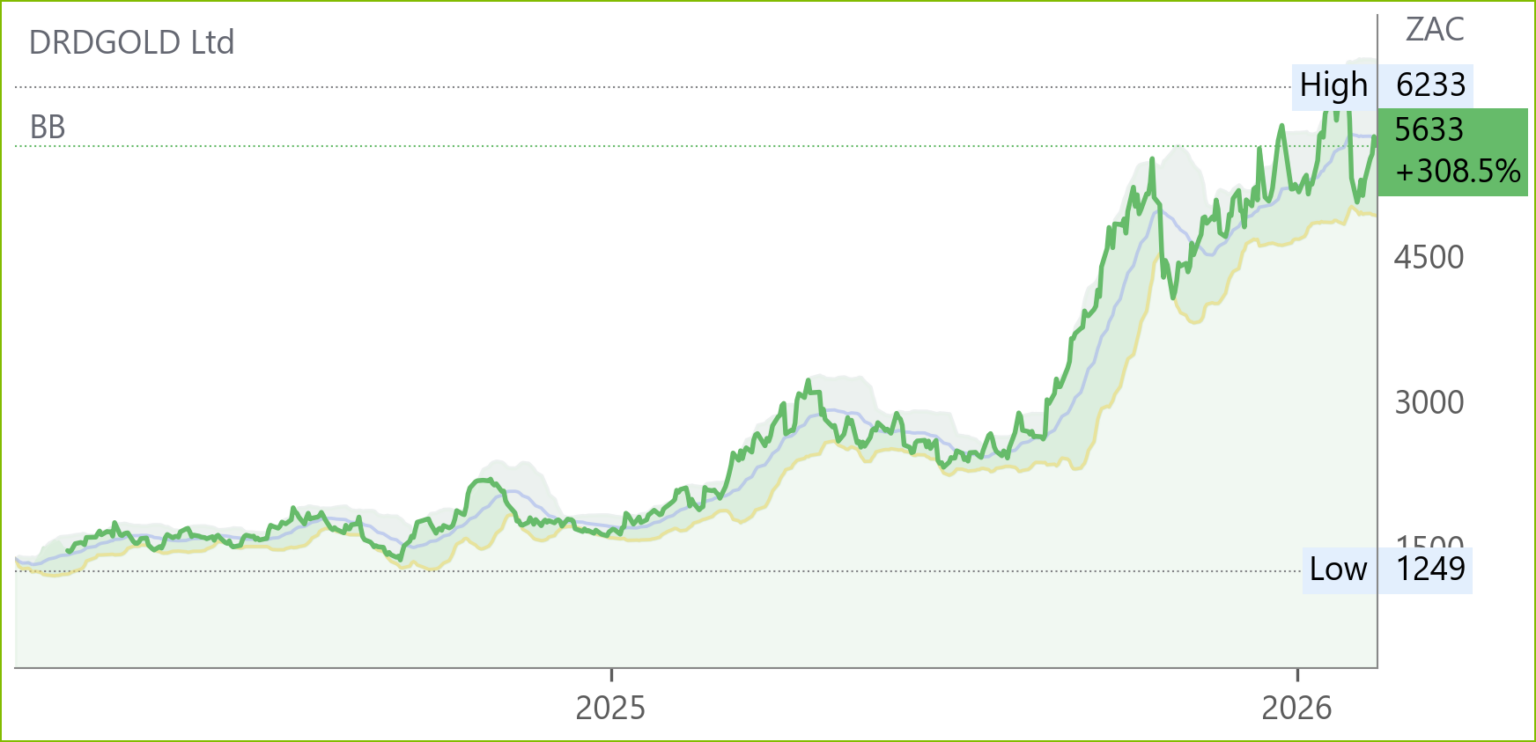

DRDGold (DRD) Trading Statement for 6M Dec ’25 (5633c)

HEPS: 217.5c–228.7c (+93% to +103% from 112.6c)

EPS: 216.9c–228.2c (+93% to +103% from 112.6c)

Revenue: R5.05bn (+33% from R3.80bn)

Dividend: R345.7m paid during the period

Revenue rose on a 43% higher Rand gold price despite 7% lower gold sales. Ergo benefited from solar and battery storage, cutting Eskom electricity use by 38% and costs by 23%. FWGR added 67Mt to resources via the Kloof 2 dump transfer. Capital reinvestment surged 74% to R1.65bn, advancing Vision 2028 projects. Cash holdings grew to R1.73bn, with no bank debt. “We remain positive that construction milestones will be met, recovering lost time despite weather delays.” – Board statement. Results due 18 Feb ’26

South32 (S32) Interim Results for 6M Dec 25 (4915c)

HEPS: 9.0 cps (+6% from 8.5 cps)

EPS: 10.3 cps (+29% from 8.0 cps)

Operating Profit: US$464m (+29% from US$360m)

Revenue: US$2.81bn (‑3% from US$2.88bn)

Dividend: 3.9 USc per share (interim, +15% from 3.4 USc)

EPS rose significantly faster than HEPS, reflecting disposal gains and portfolio optimisation. Revenue dipped slightly, but stronger operational performance lifted earnings. The interim dividend was increased to 3.9 USc per share, maintaining a 40% payout ratio.

Resilient demand for critical minerals and disciplined capital allocation underpin confidence in future growth. Mozambique’s Mozal aluminium plant will be placed on care and maintenance in Mar ’26 after failing to secure affordable power, impacting 2,000 employees and contractors. Underlying earnings rose 13% above consensus to US$435m, driven by higher copper, silver and aluminium prices, lower costs, and a profitable manganese division recovery. Brazil aluminium guidance was trimmed. “We’re definitely heading for care and maintenance.” – Graham Kerr, CEO.

Aspen Pharmacare (APN) Trading Statement for 6M Dec 25 (12515c)

HEPS: 400.1–432.4 cps (‑38% to ‑33% from 645.4cps)

EPS: 317.2–344.1 cps (‑41% to ‑36% from 537.7cps)

Revenue: Commercial Pharmaceuticals +4% (CER)

EBITDA: R4.9–5.2bn (‑11% to ‑16% from R5.8bn)

HEPS and EPS fell sharply due to once‑off restructuring costs of ~R700m in sterile facilities and the absence of prior mRNA contract contributions. Commercial Pharmaceuticals delivered organic growth across Injectables, OTC and Prescription, supported by strong demand for Mounjaro in South Africa and improved China performance. Free cash flow exceeded R1.7bn, reducing net debt to R28.6bn.

Outlook remains positive with double‑digit NHEPS growth expected in FY26. “Aspen is advancing its strategic priorities, reshaping manufacturing and driving sustainable growth in Commercial Pharmaceuticals.” – Stephen Saad, Group CEO.

Capitec (CPI) Trading Statement for FY26 (464811c)

HEPS: 14 294c–14 890c (+20–25% from 11 912c)

EPS: 14 293c–14 889c (+20–25% from 11 911c)

HEPS and EPS growth of 20–25% reflects strong lending activity, higher transaction volumes, and expanding insurance income. A simplified fee structure introduced in Mar ‘25 reduced costs for clients but was offset by rising adoption of Capitec Connect and value-added services. Loan disbursements increased, supported by new credit offerings and improved loan book quality.

Momentum in business banking and insurance products underpins sustainable growth. “Capitec is positioning itself for long-term value creation, supported by disciplined execution and client-focused innovation.” – Gerrie Fourie, CEO. Results due 22 Apr ‘26.

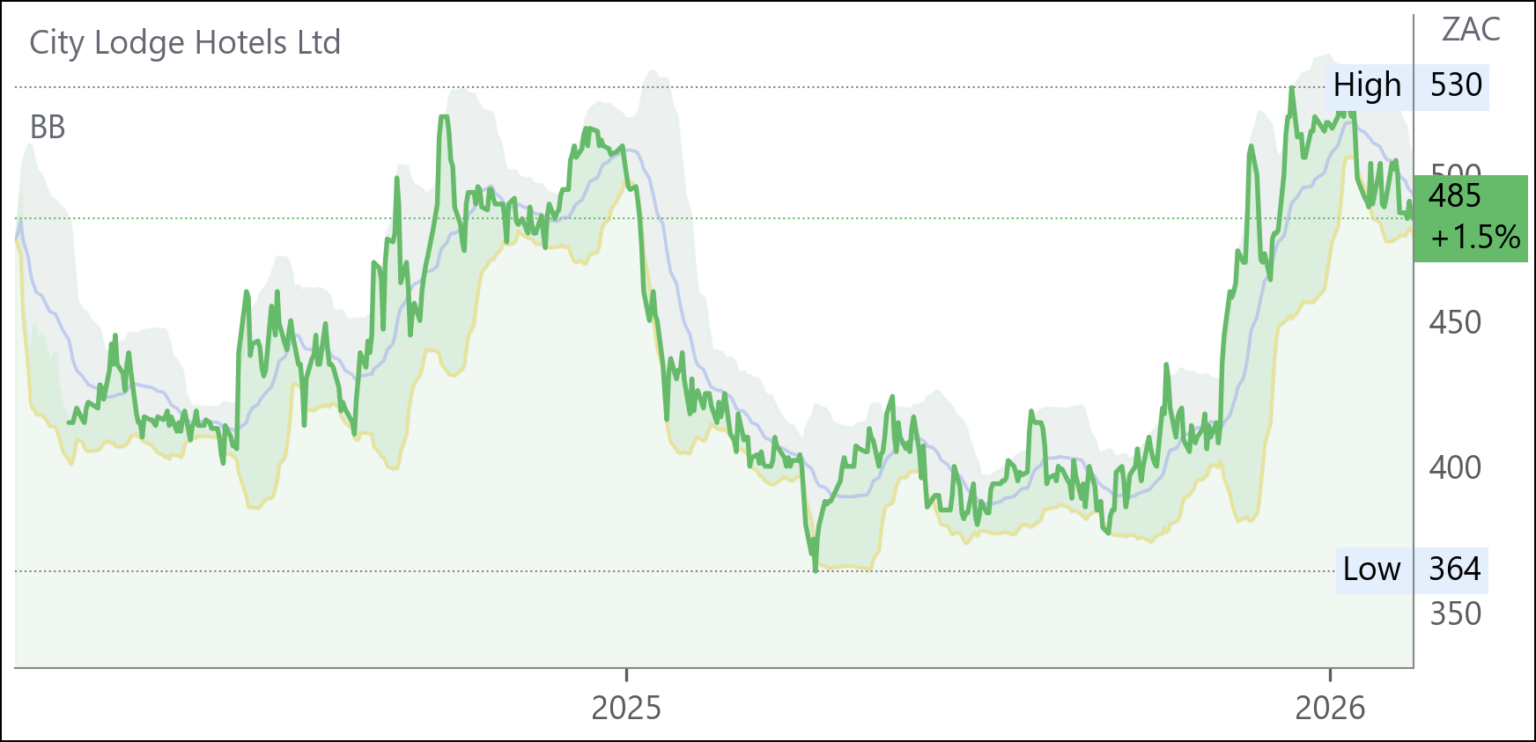

City Lodge (CLH) Voluntary Trading Statement for 6M Dec 25 (485c)

HEPS: 20.7–22.0 cps (‑4% to +2% from 21.6 cps)

EPS: 20.7–22.0 cps (‑4% to +2% from 21.6 cps)

Adjusted headline earnings per share rose to 25.3–26.6 cps (up 29%–36% from 19.6 cps), reflecting stronger underlying trading. Improved occupancies, festive‑season demand and recovery in domestic leisure and corporate travel underpinned H1 F26 performance; management signals continued recovery and a positive outlook. Results due 19 Feb ’26.

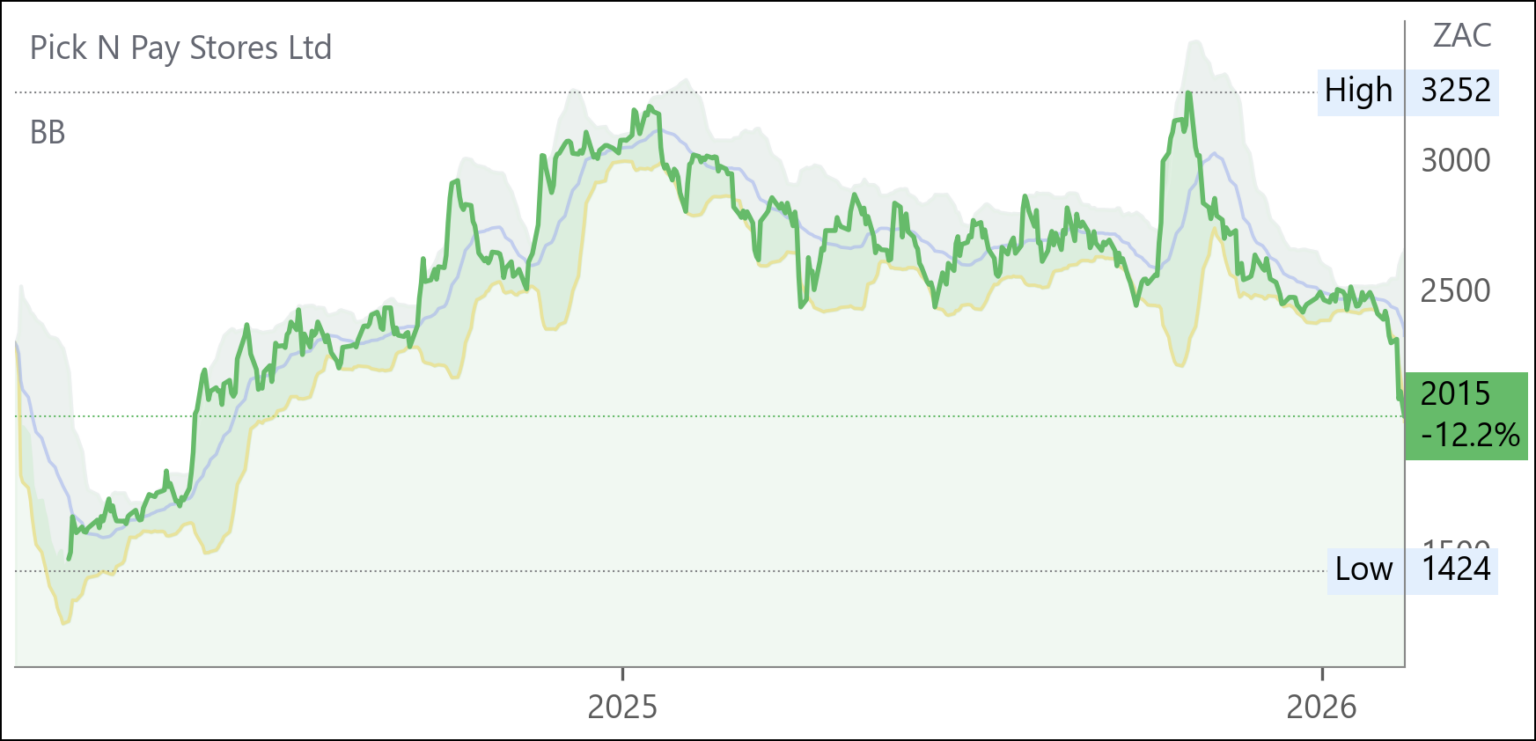

Pick n Pay (PIK) Trading Update 48W Feb ’26 & Trading Statement FY26 (2015c)

HEPS: Loss expected to widen by >20% (from –61.5c)

Revenue: +3.2% (like-for-like +3.4%)

Turnover grew modestly, with Boxer up 11.9% and online sales surging 31.8%. Clothing turnover rose 4.9% but faced late-period weakness. Company-owned supermarkets delivered 3.5% like-for-like growth, offsetting closures of underperforming stores. Market softness in Nov ’25 weighed on results, though momentum recovered in Dec ’25 and Jan ’26. Headline loss expected at R489.6m, widening 20% from R407m in FY25, though improved from R977m in FY24. EPS guidance remains uncertain. Turnover rose 3.2% over 48 weeks, with like-for-like sales up 3.4%. Planned closures and conversions of underperforming stores reduced turnover by 1.4%, weighing on performance. Expect deeper losses despite modest turnover growth, as restructuring of underperforming outlets offsets sales gains. Results due 25 May ’26.

Rainbow Chicken (RBO) Trading Statement for 6M Dec 25 (700c)

HEPS: 69.46c–76.59c (+94.9%–114.9% vs 35.64c in 6M Dec 24)

EPS: 69.46c–76.57c (+95.2%–115.2% vs 35.58c in 6M Dec 24)

Improved agricultural performance, operational efficiencies, robust demand and lower feed costs underpinned a near doubling of earnings. The strong rebound reflects reduced commodity input costs and disciplined execution across operations. Outlook remains constructive, with management emphasising resilience in volatile conditions. Results due 11 Mar ‘26.

RCL Foods (RCL) Trading Statement for 6M Dec ’25 (892c)

HEPS: ↓ ≥25% (≥27.4c lower from 109.4c)

EPS: ↓ ≥40% (≥54.0c lower from 135.1c)

EPS fell more sharply than HEPS due to once-off gains in the prior period, including Rainbow unbundling (22.3c impact), insurance proceeds (2.8c), and partial recovery of the sugar levy (5.6c). Sugar business performance was materially impacted by deep-sea imports displacing local sales into lower-priced export markets.

Market dynamics in the sugar industry weighed heavily, with tariffs failing to protect against imports. Groceries and Baking units showed improved profitability despite volume pressure. Urgent resolution of the sugar tariff review by ITAC is critical for sustainability of growers and millers. Results due 2 Mar ’26.

Sea Harvest (SHG) Further Trading Statement FY25 (960c)

HEPS (Group): 216c–222c (+293%–303% vs 55c FY24)

HEPS (Continuing Ops): 192c–196c (+434%–444% vs 36c FY24)

HEPS (Discontinued Ops): 24c–26c (+25%–35% vs 19c FY24)

EPS (Group): 79c–86c (+10%–20% vs 72c FY24)

EPS (Continuing Ops): 95c–101c (+80%–90% vs 53c FY24)

EPS (Discontinued Ops): (16c)–(14c) vs 19c FY24

Explanation: HEPS surged >200% driven by stronger hake catch rates, improved pricing, dairy milk flow and efficiency gains. EPS lagged due to impairments in Australia, Aquaculture and Cape Harvest Foods linked to prawn fishery reductions, abalone farm closures and Ladismith Cheese disposal.

Sea Harvest expects a sharp rebound in FY25 earnings, with HEPS rising over 200% on improved hake and pelagic performance, dairy growth and tight cost control. EPS gains were muted by impairments in Australia, Aquaculture and Cape Harvest Foods. Ladismith Cheese was classified as discontinued operations under IFRS 5. Management highlighted efficiency gains and stronger pricing as key drivers of recovery. Results due 3 Mar ‘26.

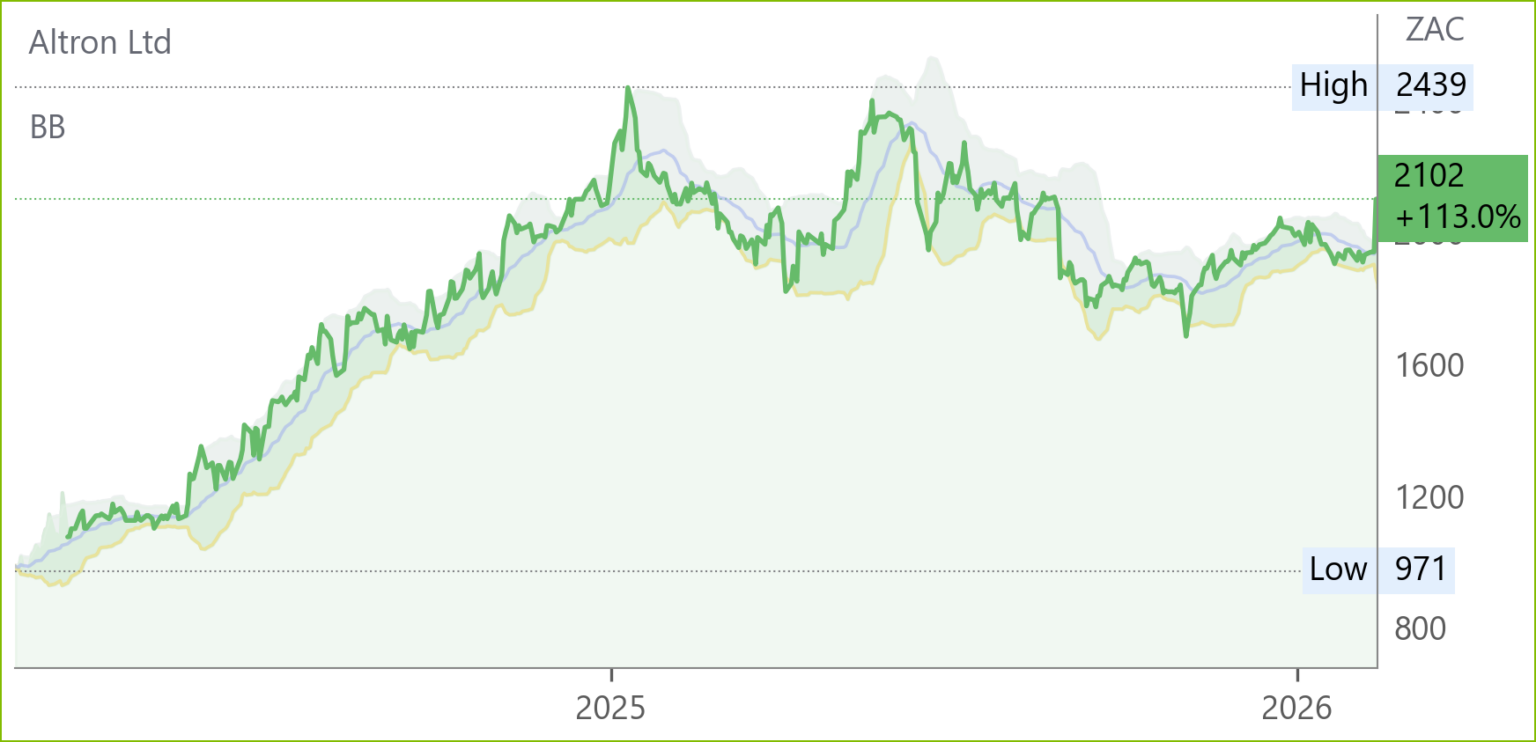

Altron (AEL) Trading Statement for FY26 (2102c)

HEPS: >201 cps (+50%+ from 134 cps)

EPS: >155 cps (+50%+ from 103 cps)

HEPS and EPS are expected to rise more than 50% year‑on‑year, driven by strong performance across continuing operations including Netstar, FinTech, HealthTech and Digital Business. The group will host a pre‑close investor call on 24 Feb ’26 to provide further operational detail.

Momentum in technology services and digital transformation supports a positive outlook. “Altron is delivering sustainable growth by focusing on core operations and driving innovation across our portfolio.” – Phillipe Welthagen, Investor Relations. Results due late Feb ’26.

Snippets

Orion Minerals (ORN) signed a landmark US$250m prepayment facility with Glencore to fund development of the Prieska Copper Zinc Project. Tranche A (US$40m) will finance the Uppers, while Tranche B (US$210m) supports the Deeps, with early drawdown of US$50m possible. First concentrate is expected end-Q1 ’27. The deal strengthens Orion’s transition to production and expands its Northern Cape portfolio.

Bidvest (BVT) confirmed termination of its agreement to sell Bidvest Bank to Access Bank plc after conditions precedent were not met. The disposal process has been relaunched, with Bidvest continuing to support the bank, which remains well-capitalised. Separately, Bidvest concluded an agreement to sell Bidvest Life to a private equity-led consortium, subject to regulatory approvals.