Finova Investor Digest

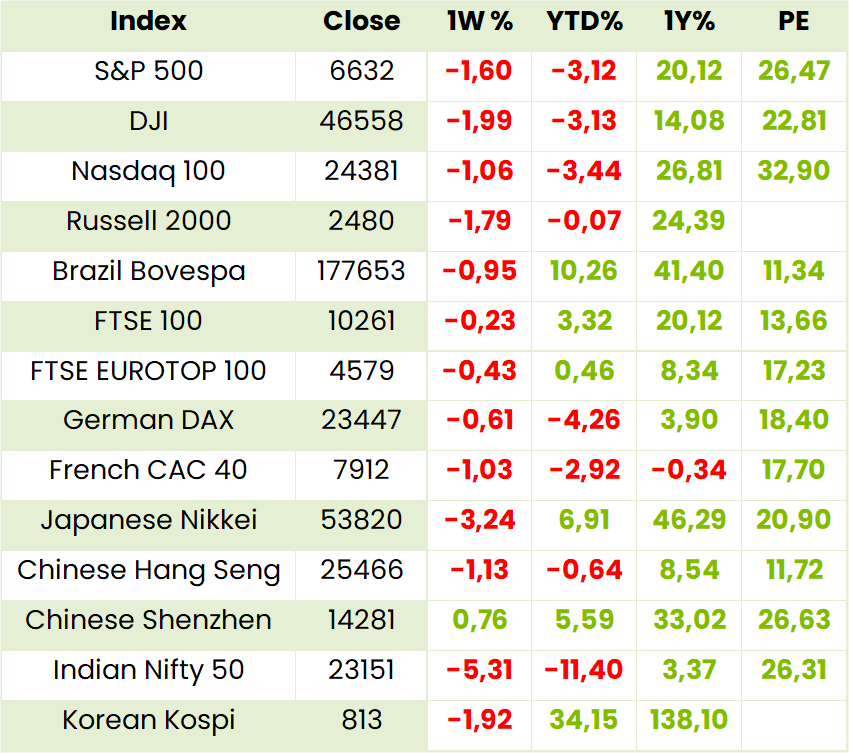

Global Indices

Currencies, Crypto & Commodities

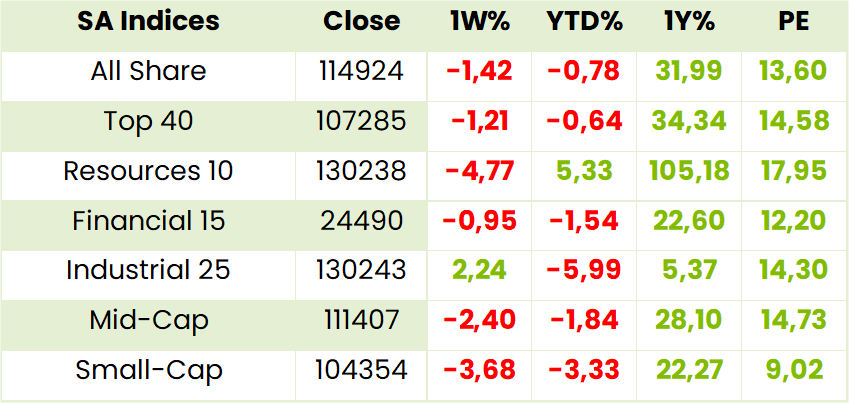

SA Indices

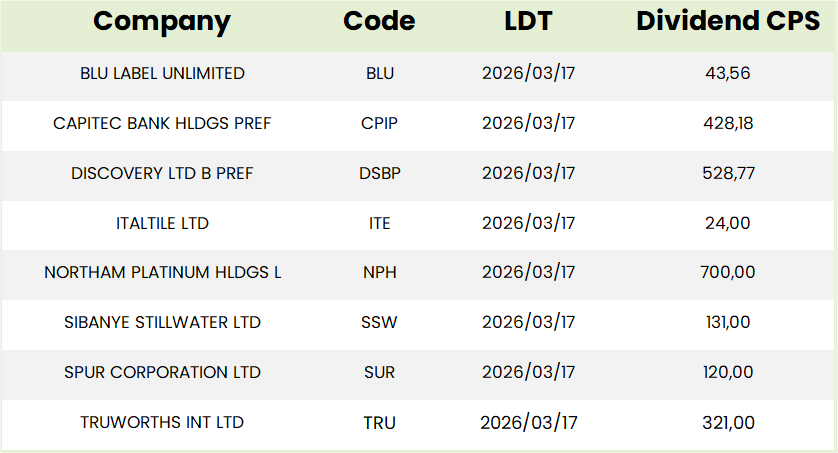

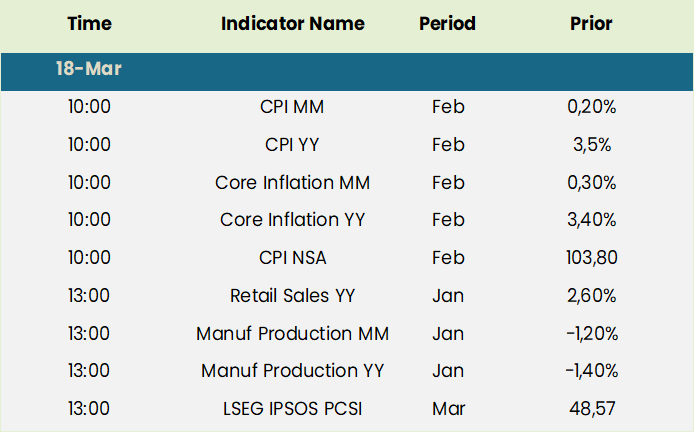

SA Upcoming Indicators & Dividends

SA Equity

Harmony Gold (HAR) Interim Results for 6M Dec 25 (25690c)

HEPS: 1431c (+13% from 1270c)

EPS: 1563c (+24% from 1265c)

Operating Profit: R16 107m (+61% from R10 003m)

Revenue: R44 400m (+20% from R37 141m)

Dividend: 530c per share (interim, up from 227c)

Operating profit surged 61% on stronger gold prices, despite a 9% fall in production and 11% lower underground grades. Revenue rose 20%, supported by a 36% higher average gold price. AISC increased 21% due to lower volumes. Harmony doubled its interim dividend under a revised policy, declaring a record R3.38bn payout. Copper integration from CSA mine and approval of Eva Copper project signal diversification. “Harmony has strengthened its position as a higher quality, lower risk global gold and copper producer… converting today’s strong gold price into lasting value.” – Beyers Nel, CEO.

Comment: as Harmony Gold is owner of the world’s oldest and deepest gold mines investors need assurance that the company will continue to operate long after Mponeng has finally closed. The answer of course is that the company has long been pursuing greenfields and brownfields expansion opportunities with the move into copper in Australia following on the much earlier expansion into Papua New Guinea copper mines. With bullion currently running at around $5000oz, well above the $3421oz received in 1H, the 2H FY26 DY will be well above the 3.8% of the first half’s 530c annualised. Crucially CEO Beyers Nel makes the point that with “disciplined and balanced capital allocation focused on value” Harmony will long be capable of “funding growth while delivering cash to shareholders”.

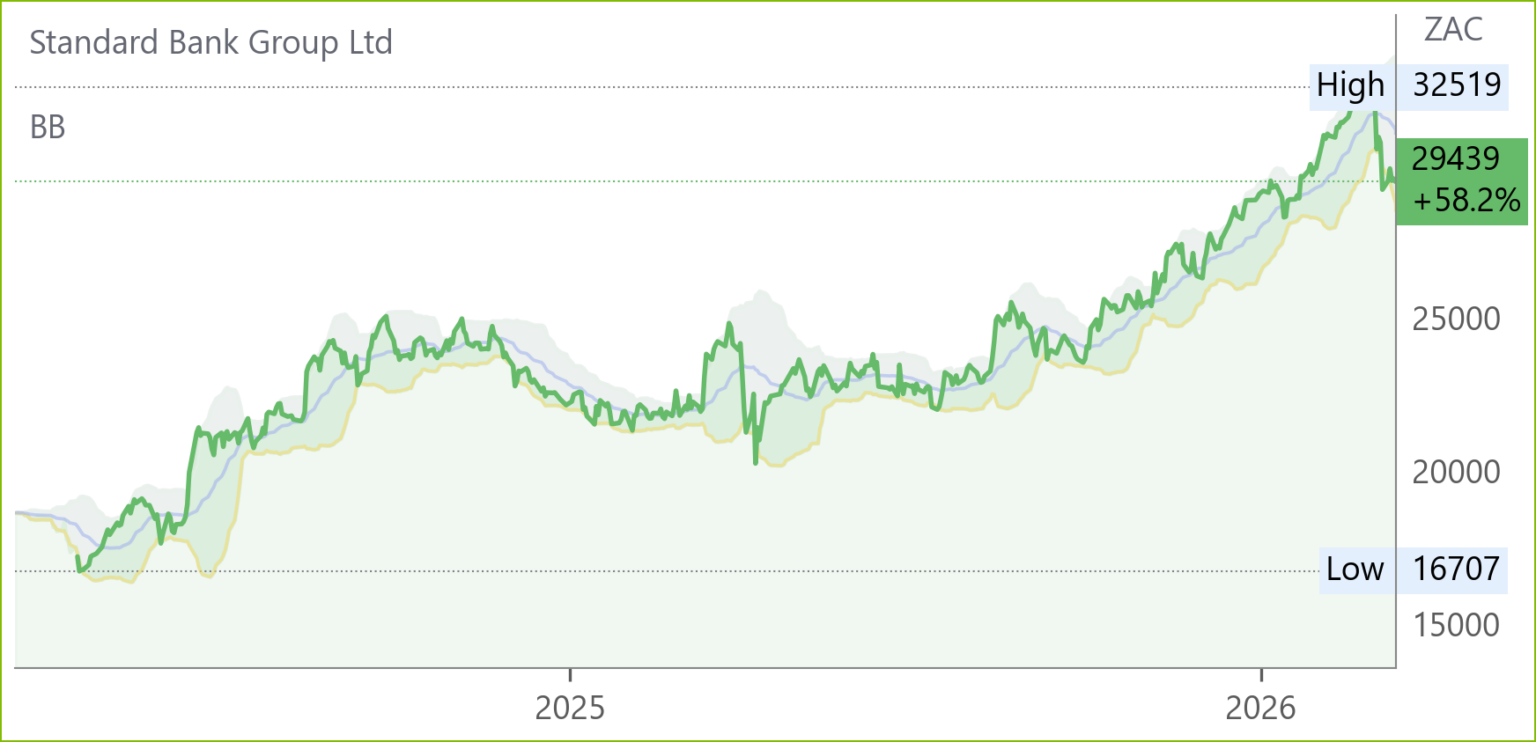

Standard Bank (SBK) Financial Results FY25 (29439c)

HEPS: 3 025.7c (+12% from 2 691.0c)

EPS: 3 019.1c (+14% from 2 644.1c)

Operating Profit: R49.1bn (+12% from R43.7bn)

Revenue: R194.8bn (+7% from R181.7bn)

Dividend: 1 695c per share (final dividend 878c)

Headline earnings rose to R49.2bn, supported by balance sheet growth, fee income and lower credit impairments. Digital retail initiatives in South Africa lifted digital clients by 9%, while Africa Regions contributed R19.7bn. Sustainable finance mobilisation reached R277bn since 2022, with R100bn in 2025. “In 2025, Standard Bank Group delivered another strong performance and successfully achieved the 2025 financial targets set out in August 2021.” – Sim Tshabalala, Group CEO.

Management expects mid-to-high single-digit banking revenue growth in FY26, disciplined cost control, and ROE above FY25’s 19.3%. Comment: CEO Sim Tshabalala points to the Group’s powerful position in its 21 African countries where the Africa Regions are growing steadily (4.5% in 2025) with, in many cases, higher interest rates, lower inflation (except Angola, Nigeria, and Malawi) and improving credit ratios. Despite SA’s paltry 1.4% GDP growth for 2025, the CEO is confident that the green shoots of recovery In many metrics, including home loans growth, bode well for some resilience in the face of higher oil prices. The integration of Liberty Life has gone well with insurance operations up 29% in 2025 and asset management up 16%. On a 9.6x PE and 5.8% DY the stock remains a core consideration for any long term portfolio. Prolonged rocketing of oil prices will, of course affect this, although oil producers Angola and Nigeria would benefit. On the more severe of two scenarios with a $100/bbl price and 3.5m bbl per day shortfall, Standard Bank calculates that global GDP, which the IMF was forecasting at 3.3% for 2026, would take a 0.6% hit. At the time of writing the price is $100 but, with the Iranians embarked on an all or nothing strategy to impose maximum damage to the global economy, the disruption could well be greater, and last longer, than markets are currently pricing in.

Absa (ABG) Financial Results FY25 (23061c)

HEPS: 2987c (+12.2% from 2662c)

EPS: 2679.6c (+3.1% from 2599.2c)

Revenue: R115.7bn (+5.2% from R109.9bn)

Dividend: 850c per share (final)

NAV: 20,802c (+7.7% from 19,311c)

Absa delivered resilient FY25 results with headline earnings up 12.2% and revenue growth of 5.2%, supported by strong loan and deposit growth (+6.1% and +7.9% respectively). ROE improved to 15.0% while cost-to-income ratio edged higher to 53.8%. Net interest margin compressed slightly to 4.53%. CEO Kenny Fihla stated, “We remain committed to enabling inclusive growth and building financial resilience across our pan-African footprint.” The Group declared a final dividend of 850c per share, confirming solvency and liquidity compliance.

Comment: earnings from the Africa Regions grew 25% to R7.8bn or 31 % of the Group total. This outpaced the 7% growth in earnings in SA to R17bn or 69% of the total. Absa now operates in 12 African countries. It is as yet early days in the new CEO Kenny Fihla’s tenure, but the numerous appointments he has made, including from among former colleagues at Standard Bank, may well make themselves felt in FY26. He has, however, also appointed M-Pesa’s Sitoyo Lopokoiyit which places the group in a good position to scale Absa’s Chat Wallet so as to compete with the telcos, fincos and retailers which are now entering the payments field. This has opened up thanks to Reserve Bank reforms which have facilitated a national payments system which is easy for banks, telcos, fintechs and retailers to plug into. On an 8x PE it is highly likely that Absa, which is under rated relative its peers, will reduce the gap.

OUTsurance* (OUT) Interim Results for 6M Dec 25 (7255c)

HEPS: 151.8c (+14.2% from 132.9c)

EPS: 151.1c (+13.7% from 132.9c)

Operating Profit: R3 610m (+5.1% from R3 434m)

Revenue: R20.5bn (+14.3% from R17.9bn)

Dividend: 120.7cps interim (+36.2% from 88.6cps) and 30.3cps special

OUTsurance delivered resilient growth, with normalised earnings up 7.7% to R2.3bn and ROE at 32.3%. Strong South African performance offset weather-related claims in Australia, while Ireland remains loss-making but on track for breakeven. Premiums grew 17.4% in P&C, though claims ratio rose to 58.6% due to higher catastrophe events. Cost-to-income ratio improved to 27.5% following structural expense reductions. A special dividend was declared from monetisation of non-core assets. Leadership transition will see Venessa Naidoo appointed chairperson post-AGM Nov ’26. “Our diversified earnings base and disciplined capital management underpin sustainable growth across geographies.” – Marthinus Visser, CEO.

Comment: so, the advantages of a balanced portfolio were shown by the extent of the swings in normalised earnings in Australia (down 43.3% from R1198m to R679m) and SA (up 68.9% from R1171m to R1980m). Ireland went from -R218m to -R263m but is on schedule for breakeven in April 2029. On the assumption that 2H26 will not see a repeat of claims, in any of the three territories, on the scale of the very substantial weather catastrophe conditions in Australia, the bounce back could make buying now on a 22.8x PE, well worthwhile. (LDT for special and ordinary dividends 14 April).

Sanlam* (SLM) Financial Results for FY25 (9000c)

HEPS: 792c (-18% from FY24)

EPS: 763c (-29% from FY24)

Operating Profit (NRFFS): R15,9bn (+3% from FY24)

Revenue: R495,9bn (+18% from FY24)

Dividend: 485c per share (final, +9% from FY24)

Headline earnings fell 18% and EPS dropped 29%, reflecting weaker investment returns and structural changes, while revenue surged 18% to a record R495,9bn. Net client cash flows more than doubled to R127bn, supported by strong inflows across life, general insurance and asset management. Sanlam restructured operations, strengthened its Allianz partnership in Pan-Africa, and reshaped asset management towards high-growth asset classes. “Building on this strong foundation, our Vision 2030 strategy targets faster future growth and stronger future cash generation.” – Paul Hanratty, Group CEO.

Comment: given the somewhat complex accounting issues, management stressed the positive operating performance -Net Result from Financial Services was 3% up at R15.9bn but, on a normalised basis, was up 20%! The reported 792 Heps, however, makes for a high 11.4x PE (consensus shows 9.4x). That said, we believe the share remains a Hold at these levels given the positive Africa outlook for the Allianz partnership, strong performance of Santam and its strengthened position in the Shriram ecosystem, increasing stakes in Shriram Wealth, Shriram Asset Management, Shriram Insights Share Brokers as well as regulatory approval on increases in Shriram General and Life Insurance shareholdings.

Santam (SNT) Financial Results for FY25 (40850c)

HEPS: 3,743c (↑8% from 3,477c)

EPS: 3,717c (↑11% from 3,356c)

Revenue: R56.1bn (↑7% from R52.3bn)

Dividend: 1,090c per share (final dividend, ↑11% from 985c) Santam delivered strong FY25 results, supported by disciplined underwriting and execution of its FutureFit 2030 strategy. Conventional insurance NEP grew 15% with a net underwriting margin of 11.3%, aided by favourable claims and property portfolio recovery. MiWay achieved record new business sales, while acquisitions contributed positively. International expansion was bolstered by Lloyd’s approval for Santam Syndicate 1918, effective Jan ’26, and Shriram General Insurance in India delivered 27% GWP growth. “Our disciplined execution and strategic focus have positioned us strongly for sustainable growth and international expansion.” – Tavaziva Madzinga, Group CEO.

Comment: with Zimbabwean actuary Tavaziva Madzinga well into his third year as CEO, the FutureFit 2030 strategy continues to unfold with growth vectors including shifting to a multi-channel model while maintaining broker dominance as well as international diversification which contributed 19% of GWP (FY24: 17%). This included the hiking of its 40.25% share in Shriram General Insurance of India to 51% in 2024 as well the recent establishment of a reinsurance office in the GIFT city in Gujarat. Management also points out that Santam will benefit from the Sanlam-Alliance joint venture in Africa. Together with the interim dividend of 590c the share is on a 4.2 DY and 10.7x PE. We think there is a strong case for the gap between it and its above mentioned peer to be closed.

Metair (MTA) Financial Results FY25 (415c)

HEPS: 191c excluding Rombat fine (+82% from 105c) and-21c including Rombat fine

EPS: 31c (–80% from 155c)

Operating Profit: R1 087m (+99% from R546m, excl. Rombat fine)

Revenue: R17.9bn (+57% from R11.4bn)

Metair delivered strong operational growth, with revenue up 57% and operating profit nearly doubling, supported by AutoZone volumes and improved repayment terms. However, the Rombat fine and Hesto accounting adjustments weighed heavily on EPS, which fell sharply. Cash generation improved 27% to R1.88bn, with cash balances rising 50% to R1.21bn. No dividend was declared as management prioritises balance sheet resilience. An appeal against the €413m Rombat fine was lodged in Feb ’26. “Metair is pleased with the operational performance of its businesses in 2025, reflecting a simplified structure and sustainable capital alignment.” – PS O’Flaherty, CEO.

Comment: O’Flaherty is continuing with the major changes already made in his two year tenure and these include diversification from dependence on OEM with the move to servicing the aftermarket via Autozone which already contributes 30% of revenue and 40% is targeted “as soon as possible”. The much challenged OEM side of the business services Ford, Toyota and Volkswagen and, if Chinese brands set up OEM businesses in SA on a CKD basis, Metair, which is already engaging with them, could well participate. Management is strongly contesting the EU fine, which is fully provided for, and judging by the strategic excisions made so far we think Rombat could well be the next to go. On a 2.2PE and NAV of 1135c there is a case for early accumulation, but we think it would be worth waiting for further progress on strategic issues and debt reduction (Net Debt R3.9bn v. Equity R2.26bn).

Grindrod (GND) Financial Results FY25 (1747c)

HEPS: 179.8c (↑285% from 46.7c)

EPS: 310.0c (↑559% from 47.1c)

Operating Profit: R2.1bn (↑107% from R1.0bn)

Revenue: R5.6bn (↑12% from R5.0bn)

EBITDA: R1.6bn (↑430% from R295m)

Dividend: 25.2c final + 43.0c special per share

Grindrod delivered record port volumes, with Maputo reaching 32mtpa and Matola 9.9mtpa. Logistics performance was subdued due to rail refurbishment and weaker graphite/container volumes, but overall results surged on strong terminal operations and divestitures of non-core assets. Cash generation exceeded R2bn, supporting both final and special dividends. “Grindrod has successfully completed its strategic reset and moved decisively into a growth phase, delivering measurable returns despite external volatility.” – VB Commaille, Group Company Secretary.

Rainbow Chicken (RBO) Interim Results for 6M Dec 25 (699c)

HEPS: 74.81c (+109.9% from 35.64c)

EPS: 74.79c (+110.2% from 35.58c)

Revenue: R8.79bn (+11.3% from R7.89bn)

EBITDA: R1.05bn (+81.4% from R581m)

Dividend: 15.0cps (interim, first declaration)

Rainbow delivered strong growth, with EPS and HEPS more than doubling, supported by robust chicken demand, lower input costs, and operational efficiencies. EBITDA margin expanded to 12% from 7.4%, reflecting improved pricing and product mix. Strengthening of the Rand against the US Dollar further boosted profitability. The balance sheet shows increased assets and liabilities, positioning Rainbow to fund capital investments and growth initiatives. An interim dividend of 15cps was declared, marking the company’s second payout since listing. “Rainbow is well placed to support ongoing operational requirements, planned capital investments and future growth initiatives.” – Board of Directors.

AVI (AVI) Interim Results for 6M Dec ’25 (10405c)

HEPS: 455.1c (↑11.7% from 407.5c)

EPS: 452.8c (↑10.6% from 409.5c)

Operating Profit: R1.9bn (↑11.6% from R1.7bn)

Revenue: R8.2bn (↑4.9% from R7.8bn)

Gross Profit: R3.2bn (↑6.3% from R3.0bn)

Dividend: 245c per share (interim dividend, ↑11.4% from 220c)

AVI delivered resilient growth despite constrained consumer demand, supported by innovation in biscuits and strong December trading in fashion retail. I&J fishing profits improved, though abalone remained under pressure. Restructuring initiatives added R39.4m to earnings, while cash generation remained robust with ROCE at 35.9%. “Sound profit growth in a constrained environment reflects disciplined execution and portfolio resilience.” – Simon Crutchley, CEO.

Orion Minerals (ORN) Interim Results for 6M Dec 25 (35c)

HEPS: -0.06c (↑14% from -0.07c)

EPS: -0.06c (↑14% from -0.07c)

Operating Loss: AUD6.42m (↓2% from AUD6.52m)

Orion advanced development of its Prieska Copper Zinc Mine, securing a US$250m prepayment facility to fund construction of the Uppers and Deeps. Dewatering infrastructure achieved 500m³/hr pumping capacity, while Okiep Copper Project optimisation incorporated data from eight new prospects. Wastewater dam construction is underway, enabling dewatering of Flat Mine North. Exploration at Jacomynspan Nickel-Copper-Cobalt-PGE Project continued, targeting metallurgical innovation. Losses narrowed slightly due to lower exploration costs and finance income. “Orion is well advanced in its transition to developer and operating mining company, focused on metals crucial to a decarbonising world.” – Tony Lennox, CEO.

Merafe (MRF) Financial Results for FY25 (119c)

HEPS: 12.2c (↓72% from 42.9c)

EPS: 5.7c (↓79% from 26.7c)

Operating Profit: R143m (↓77% from R615m)

Revenue: R5.8bn (↓31% from R8.4bn)

EBITDA: R533m (↓69% from R1.7bn)

Dividend: 8c per share (final dividend, unchanged)

NAV: R4.7bn (↓3% from R4.9bn)

Merafe faced sharp earnings decline in FY25 due to weaker ferrochrome sales, a stronger ZARUSD exchange rate, and suspension of smelting operations in the Glencore-Merafe Chrome Venture. Chrome ore and PGM sales volumes grew, partially offsetting ferrochrome weakness. Safety improved with no fatalities and a 23% TRIFR reduction. “The viability of smelting operations depends on materially lowering energy costs and sustained improvement in global ferrochrome demand.” – Zanele Matlala, CEO.

Mpact (MPT) Financial Results for FY25 (2186c)

HEPS: 307c (↓5% from 324c)

EPS: 329c (↑1% from 327c)

Operating Profit: R914m (↓1% from R923m)

Revenue: R14bn (↑5% from R13.3bn)

Gross Profit: ↑3% from prior period

EBITDA: R1.52bn (↑1% from R1.50bn)

Dividend: 60c per share (final dividend, ↓43% from 105c)

NAV: R37.76 per share (↑6% from R35.64)

Mpact navigated a demanding FY25, with strong growth in agricultural packaging offset by margin pressure in paper manufacturing. The Mkhondo mill upgrade was completed, enhancing efficiency, while solar PV capacity reached 18MWp, saving R45m in energy costs. The contemplated closure of Springs mill reflects portfolio discipline. “We are shifting focus to converting the asset base into stronger earnings, cash generation and improved returns.” – Bruce Strong, CEO.

Trellidor (TRL) Interim Results for 6M Dec 25 (128c)

HEPS: 0.6c (-98.1% from 29.6c)

EPS: 0.6c (-98.1% from 29.6c)

Revenue: R161.1m (-47.1% from R304.3m)

Trellidor reported a sharp decline in earnings, with HEPS and EPS down over 97% due to weaker demand and the disposal of Taylor and NMC. Revenue fell 47.1% to R161.1m, though net debt reduced significantly to R46.7m, lowering interest costs. Management emphasised that dividend payments will resume once revenue and margin improvements are supported by sustainable cash generation. A shareholder webinar is scheduled for 10 Mar ’26 to discuss results.

Trading Statements & Updates

Sun International* (SUI) Trading Statement FY25 (3695c)

HEPS: 675c–698c (↑35–40% from 499c)

Adjusted HEPS: 554c–572c (↑4–8% from 531c)

EPS: 655c–674c (↓12–14% from 764c)

Dividend: Interim dividend of R1bn already paid.

Sun International flagged strong FY25 headline earnings growth, supported by resilient trading across its casino and hospitality portfolio. EPS fell due to revaluation of contingent consideration from the Dreams S.A. disposal and goodwill impairments on online licences. Debt reduced to R5bn, with interest cover improving to 7.9x. “Our disciplined de-gearing and resilient operations underpin confidence in sustainable shareholder returns.” – Nwabisa Titus, Investor Relations.

Snippets

Reinet Investments (RNI) announced regulatory approval for the disposal of its entire holding in Pension Insurance Corporation Group Limited to Athora UK Holding. Completion is expected around 27 Mar ’26, with Reinet set to receive approximately GBP 2.9bn. This transaction forms part of a broader restructuring involving multiple shareholders, marking a significant liquidity event for Reinet.

Remgro (REM) has sold 51.97m FirstRand shares between 2 Feb and 10 Mar ’26 at an average price of R93.87, realising R4.88bn. This continues its strategic exit from non-core holdings, reducing its residual stake from 1.64% to zero. Proceeds bolster Remgro’s cash resources under its capital allocation framework. The disposals are classified as a Category 2 transaction and do not require shareholder approval.

Woolworths (WHL) announced CEO succession, confirming Roy Bagattini will step down after six years. Sam Ngumeni, current COO, will succeed him as Group CEO effective 1 Sep ’26. The board praised Bagattini’s leadership in strengthening the business and driving growth. Ngumeni’s appointment signals continuity and focus on operational excellence.

Pan African Resources (PAN) announced a binding scheme to acquire 100% of Emmerson Resources (ASX:ERM) via an Australian court-approved arrangement. Emmerson shareholders will receive 0.1493 new Pan African shares per ERM share, valuing the deal at ~£163m (A$311m). The acquisition consolidates Tennant Creek assets, eliminates joint venture complexities, and supports Pan African’s ASX listing. “This transaction consolidates our position in Tennant Creek, optimising project sequencing and capital allocation.” – Cobus Loots, CEO. Results of the Scheme Meeting are expected mid–late Jun ’26, with implementation targeted for Jul ’26.