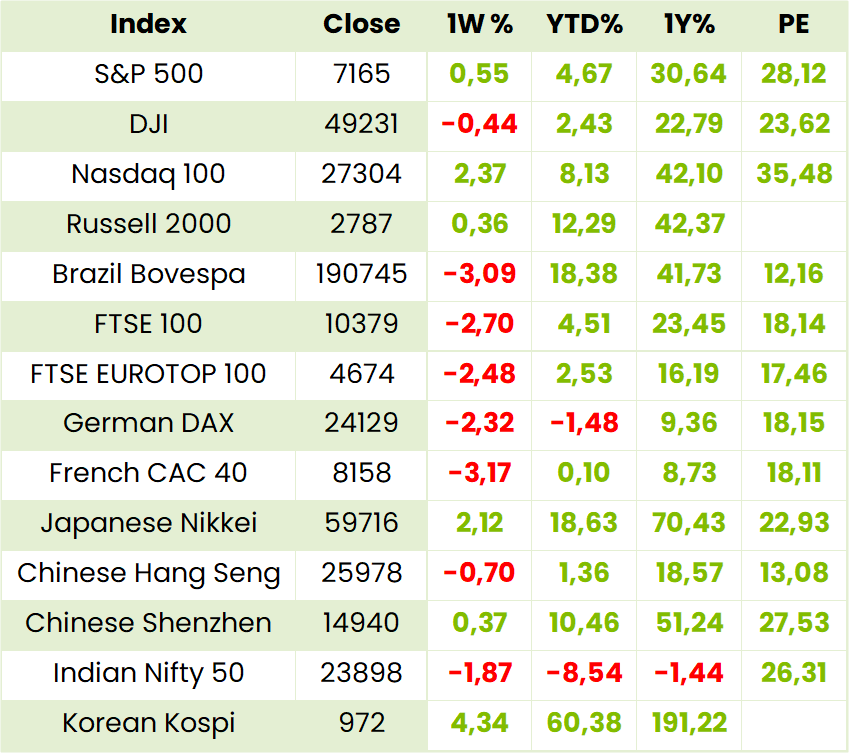

Global Indices

Currencies, Crypto & Commodities

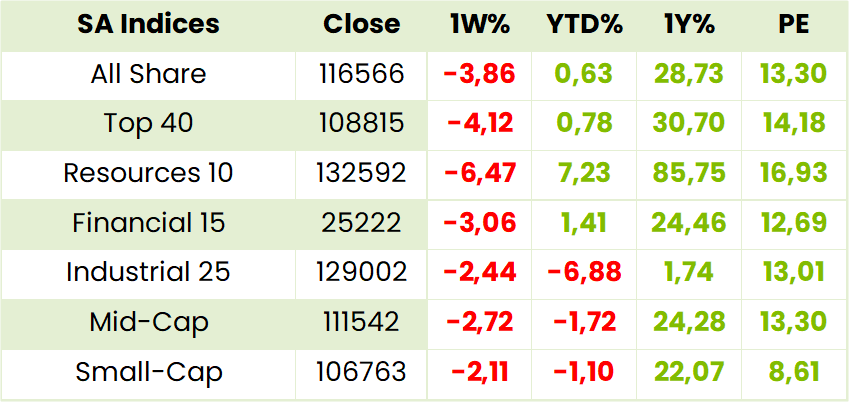

SA Indices

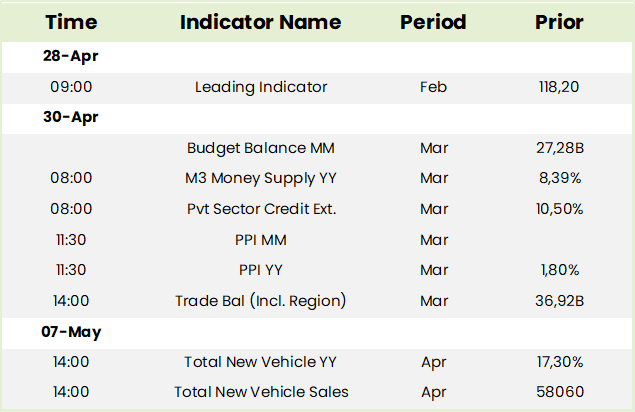

SA Upcoming Indicators & Dividends

Capitec Bank (CPI) Financial Results FY02/26 (440072c)

HEPS: 14606c (↑23% from 11912c)

EPS: 14590c (↑22% from 11911c)

Operating Profit: R22.2bn (↑25% from R17.7bn)

Revenue: R42.4bn (↑19% from R35.8bn)

Net Interest Income: R24.1bn (↑19% from R20.2bn)

Dividend: 7980cps (↑23% from 6510cps)

Return on equity: 31%; Credit loss ratio: 8.1%

Non‑interest income: 67% of operating income post impairments

Insurance income ↑38%; Value‑added services & Capitec Connect ↑38%

Active clients: 26m; Active app users: 15m

Headline earnings rose 23% to R16.8bn, supported by strong loan disbursements in Personal (+27%) and Business Banking (+48%). Non-interest income grew 19% to R28.3bn, with insurance income up 38% to R5.2bn and VAS/Capitec Connect up 38% to R6.1bn. Active banking app clients increased 19% to 15.3m. ROE improved to 31% (from 29%), while NAV per share rose 17% to 51404c.

Outlook: “Capitec continues to earn trust by delivering simple, transparent and affordable financial solutions, positioning us for sustainable growth and long-term value creation.” – Graham Lee, CEO.

Comment: these numbers support management’s contention that growth has not yet peaked with Fintech contributing 26% to Headline earnings, Personal Banking 41% and Insurance 27% respectively. Its Business Banking contributed 5% with client numbers increasing by 71% to 456000 while management continues to set great store by its future potential. The same applies to Avafin business more than half of which was in Poland followed by Mexico, then Czechia, Spain and Latvia. Avafin contributed only 1% to Headline earnings but comprised R1.3bn of the group’s R10bn credit impairment charge. So, while management is confident it will find the winning formulae for these regions it will take some time before they move the needle. Unlike peers such as Standard Bank, Absa and Nedbank, Capitec is not as yet focusing on the rest of Africa regions. Despite this we consider it to be a firm hold for the long term albeit correctly priced at present.

Standard Bank (SBK) Financial Information Q1 Mar ’26 (31214c)

Standard Bank Group provides ICBC (Industrial & Commerce Bank of China) with quarterly consolidated financial information, prepared under IFRS, to enable equity accounting of results. For 1Q26, this disclosure ensures ICBC can accurately reflect Standard Bank’s performance in its own financial reporting.

Earnings Attributable to Ordinary Shareholders: R12.3bn (↑12% from R11bn)

Headline Earnings: In line with attributable earnings

Ordinary Dividends Declared: R14.5bn (Mar ’26)

Ordinary Shareholders’ Equity: R261.7bn (↓1% from R264.2bn at Jan ’26)

Strong trading performance supported earnings growth, with headline adjustments immaterial. Treasury shares increased to R5.2bn, while retained earnings fell to R249.1bn after dividend declaration. Foreign currency translation reserve improved by R3.3bn, reflecting exchange rate movements.

Outlook: Guidance for FY26 remains unchanged despite macroeconomic uncertainty linked to Middle East conflicts. Management emphasises resilience across its network and confidence in delivering on strategic objectives.

Omnia (OMN) Interim Results for 6M Sep ’25 (9254c)

HEPS: 320c (↑11% from 288c)

EPS: 326c (↑13% from 289c)

Operating Profit: R1 184m (↑7% from R1 103m)

Revenue: R9 763m (↑0.1% from R9 753m)

EBITDA: R900m (↑12% from R802m)

Dividend: 38cps (interim, ↑9% from 35cps)

Agriculture delivered resilient growth despite supplier shutdowns and droughts in Australia and Brazil, supported by strong demand and Nutriology® solutions. Mining expanded volumes in SADC and commissioned detonator plants in Canada, strengthening its North American footprint. Chemicals remained under pressure but progressed restructuring and capital release initiatives. Net cash position was R695m, with stable NAV and reduced working capital.

Outlook: “This strong result reflects our team’s unwavering focus on delivering sustainable growth and long-term value for our stakeholders.” — Seelan Gobalsamy, CEO.

Comment: Omnia is strategically positioned to capture cyclical upside from volatility in the ammonia market and prolonged supply chain interruptions through the Strait of Hormuz. Ammonia, a critical input for mining explosives and nitrogen-based fertilisers, faces supply disruptions and pricing upheaval, trapping nearly one-third of global exports. Omnia’s integrated operations across mining and agriculture, supported by resilient distribution and recent capacity investments, enable margin expansion and pricing power while competitors face bottlenecks. With a strong balance sheet and diversified footprint, Omnia offers resilience and leverage. Over the next 18–24 months, investors can expect cyclical windfalls, reinforcing its case as a strategic beneficiary. BUY

AECI (AFE) Financial Results FY12/25 (10898c)

HEPS: 357c (↑36% from 263c)

EPS: 357c (↑36% from 263c)

EBITDA: R2.7bn (record, ↑19% from R2.3bn)

EBITDA Margin: 15% (↑300bps from 12%)

Net Debt: R465m (↓88% from R3.7bn)

Dividend: 228cps (↑4% from 219cps)

Free Cash Flow Conversion: 133% (Chemicals)

EBITDA reached a record R2.7bn in Mining, with margins expanding to 15%, while Chemicals delivered 133% free cash flow conversion. Net debt fell sharply from R3.7bn to R465m, reducing gearing to 4% and strengthening the balance sheet. Disposal of non-core assets generated R2.2bn, sharpening focus on core divisions. EPS rose 36% to 357c, and dividends increased to 228cps. Consensus earnings are forecast to grow 43.7% annually. Outlook: “AECI is advancing its transformation journey, and we are committed to delivering on our strategic goals, creating long-term shareholder value, and building a solid foundation for future success.” – Interim CEO Dean Murray.

Comment: By the time Holger Riemensberger resigned owing to personal reasons in October most of the strategic disposals planned during his tenure had been affected. Murray now expects growth to come from investment in 21.4xfurther upgrading of the Modderfontein plant as well as further investment in the mining and chemicals businesses. Mining is expected to do well in Australia, which is in any case recovering from some really severe weather events in 1H26, as well in Africa including the DRC. On the fertilizer side, Murray is confident the rigorous capital allocation process will yield the expected higher returns as per the ROIC guidance of 19-21% in FY26 from 15% in FY25. As regards the interruption in ammonia and other fertilizer related materials from the Persian Gulf he is confident he will not have a problem as AECI only had to import 10% of its ammonia in FY25. If anything, it could be a beneficiary.

The consensus heps forecast of 513cps places the stock on a FPE of 21.4x which may be enough for now. The combination, however, of operational strength, balance sheet resilience, and valuation upside reinforces a strong BUY.

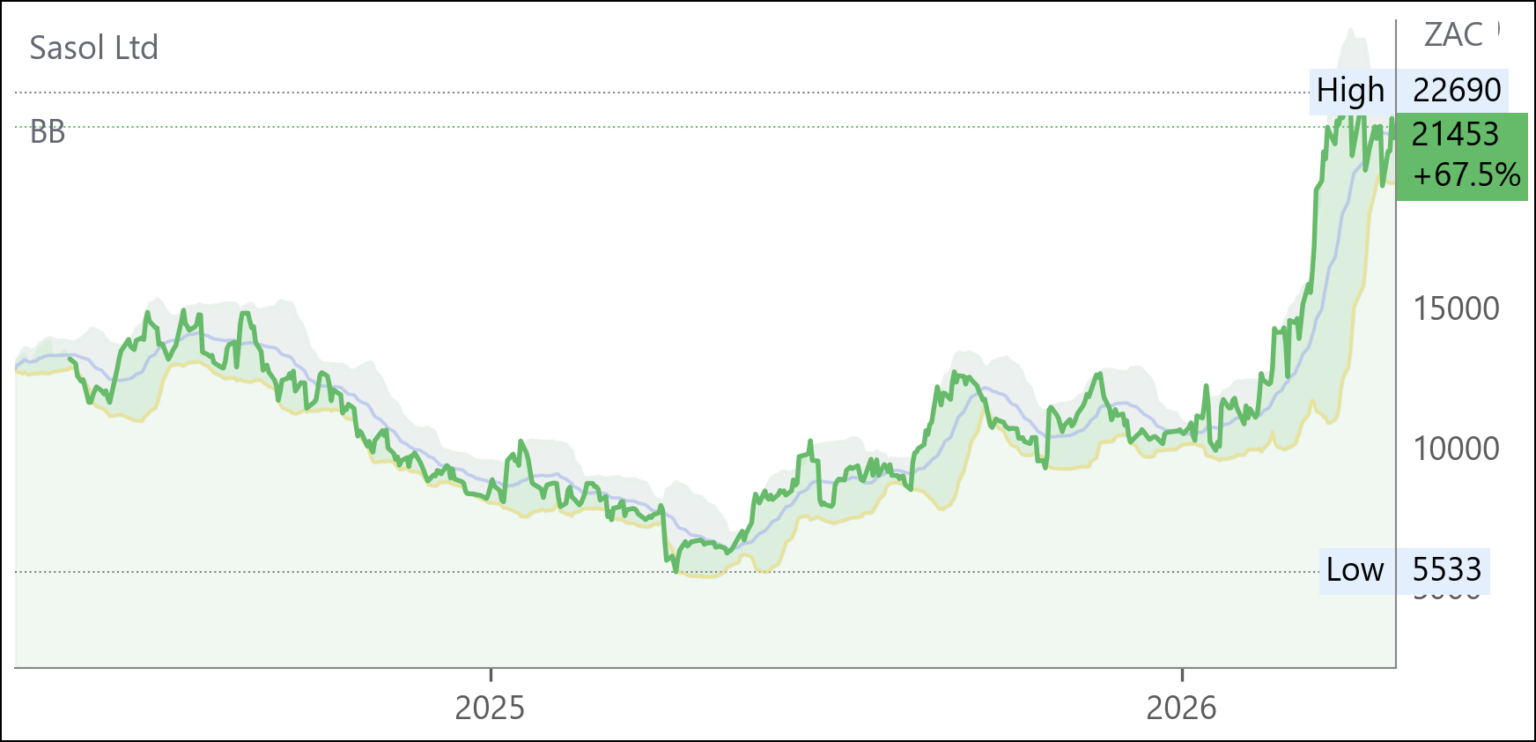

Sasol (SOL) Business Performance Metrics 9M Mar ’26 (21453c)

Southern Africa: Coal quality improved, boosting SO production (+8% y/y) and reducing external purchases. Natref volumes rose on energy security demand.

Mozambique: Flooding disrupted condensate logistics, cutting gas output.

ORYX GTL: Production halted in Mar ’26 due to gas supply disruption; restart timing uncertain.

Chemicals Africa: Revenue increased on higher volumes and prices.

International Chemicals: US benefited from stronger pricing; Eurasia faced feedstock constraints and force majeure.

Bond Issue: US$750m seven-year bond at 8.75% coupon, debt-neutral, extending maturity profile.

Sustainability: Natref achieved ISCC PLUS certification for SAF and renewable diesel.

Outlook: Fuel sales guidance raised to 10–15% above FY25; gas production revised down 5–10%. Capex lowered to R20–22bn. Management remains focused on operational continuity amid geopolitical volatility.

Clicks (CLS) Interim Results for 6M Feb ’26 (26595c)

HEPS: 653c (↑8.1% from 604c)

EPS: 653c (↑8.3% from 603c)

Operating Profit: R2.3bn (↑7.4% from R2.1bn)

Revenue: R24.9bn (↑7.4% from R23.2bn)

Gross Profit: R7.6bn (↑6.5% from R7.1bn)

Dividend: 258cps interim (↑8.4% from 238cps)

Pharmacy sales grew 8.6%, lifting market share to 24.9%. Retail turnover was impacted by warehouse system delays (R175m lost sales) and festive season discounting, but product availability recovered by Feb ’26. Store footprint reached 1 003, pharmacies expanded to 795, and ClubCard membership rose to 12.9m. UPD doubled its electric vehicle fleet, reducing fuel exposure.

Outlook: “Despite consumer pressures, we remain committed to expanding our footprint and achieving medium-term targets.” – Bertina Engelbrecht, CEO.

Comment: with Clicks and Dischem accounting for about half of the dispensary market, plus a little bit more from Shoprite’s Medirite and some independent chains like Alphapharm, there’s still a long way for Clicks to go in acquiring independents who cannot compete on scale with non-pharmacy products and loyalty incentives. Having just breached the 1000 store mark, progress towards 1200 stores will also be aided by moves into townships, other urban and rural areas. Then there is the Bro-Nation initiative which has led to Man Sorbet which , following the success of Sorbet, has led to the realisation that men will respond to a men focused grooming outlet. So, with these and other initiatives, there is little doubt that there is plenty of growth potential in addition to the non-discretionary stability from the dispensaries. Management is, however, realistically forecasting 2H Heps growth of 8.1% (mid-range of forecast) which will make for a muted FY 26 heps growth of 3.1% which will be well down on the 10 year CAGR of 13.1% to FY25. It also makes for a 6 month FPE of 18.9x which, while in line with the traditionally high rating of Clicks, could turnout to be a little bit much for current fuel juiced general inflation despite the fact that its own costs, especially in the wholesale delivery operation, are substantially shielded by extensive use of EVs. So, while the stock is much cheaper than usual, and as such is realistically priced, it is a BUY only for those who are convinced the Straits will be open next week!

Zeder Investments (ZED) Financial Results FY26 (131c)

HEPS: -27.3c (loss widened from -10.0c)

EPS: -27.3c (loss widened from -10.0c)

Operating Profit: -R23m (↓ from R37m profit)

Dividend: 7.0cps special (↓ from 61.0cps special in FY25

NAV: R1.50 per share (↓15.3% from R1.77)

NAVPS fell 15.3% due to downward valuation of Zaad ahead of disposal. A Sale Agreement was signed on 31 Jan ’26 to dispose of Zaad (excluding May Seed), valued at R1.094bn. Zeder intends to distribute most proceeds to shareholders, subject to obligations and indemnities. Leadership changes saw Johann le Roux step down as CEO/FD, replaced by Dries Mellet as FD and acting CEO.

Outlook: “Zeder’s objective remains to maximise long-term wealth for shareholders, with prudent distribution of Zaad disposal proceeds and strategic focus on May Seed.” – Board Commentary.

Trading Statements & Updates

Valterra Platinum (VAL) Production Report Q1 Mar ’26 (141369c)

M&C PGM Production: 743,500oz (↑7% y/y)

Own-mined Production: 486,200oz (↑5% y/y)

Purchase of Concentrate: 257,300oz (↑10% y/y)

Refined PGM Production: 778,500oz (↑78% y/y)

PGM Sales Volumes: 791,400oz (↑60% y/y)

Amandelbult output recovered strongly (+43%) post-2025 flooding, while Mogalakwena declined 6% due to crusher maintenance. Refined production surged as maintenance was rescheduled to Q3, reducing electricity costs. Basket prices rose 70% in rand terms to R47,529/oz, driven by platinum, rhodium and ruthenium strength.

Outlook: “We remain focused on embedding a culture of zero harm, while advancing operational excellence and delivering sustainable performance despite geopolitical uncertainty.” – Craig Miller, CEO

Impala Platinum (IMP) Production Report 9M Mar ’26 (24206c)

6E Group production was stable at 2.56Moz, with refined output up 5% to 2.63Moz and sales volumes rising 3%. Managed operations delivered 2.0Moz, while JV output dipped 2% to 395koz. Third-party receipts increased 16% to 167koz. Safety metrics improved, though two fatalities occurred at Rustenburg. Furnace 4 rebuild progressed, reducing excess inventory to 320koz. Strong operating momentum at Rustenburg and Zimplats offset weaker volumes at Marula and Canada. Demand for PGMs remained robust despite geopolitical tensions, with rand basket prices supportive.

“We remain focused on delivering consistent and safe production in the final months of FY2026 – ensuring our ability to capitalise on strong rand PGM pricing, maximise free cash flow generation and deliver value.” – Nico Muller, CEO.

South32 (S32) Quarterly Report Mar ’26 (5102c)

Net Cash: US$96m (↑US$121m from Dec ’25)

Dividend: US$175m (interim)

Alumina: 2,779kt (flat y/y; Brazil Alumina record 1,060kt, ↑5%)

Aluminium: Hillside 538kt (flat); Mozal 248kt (↓6%, placed on care & maintenance)

Copper Eq: Sierra Gorda 67.2kt (flat; distribution US$135m)

Zinc Eq: Cannington 147.6kt (↓16% from 174.7kt)

Manganese: Australia 2,249kwmt (guidance ↓6% to 3,000kwmt); SA 1,557kwmt (flat)

Adverse weather and Cyclone Narelle impacted manganese and Cannington, but Brazil Alumina achieved record output. Hermosa’s Taylor zinc-lead-silver project advanced with key permitting milestones.

Outlook: “Our strong balance sheet leaves us well placed to manage short-term volatility in global markets, while continuing shareholder returns and investing in high-quality growth options to increase our production of copper, zinc and silver.” – Graham Kerr, CEO.

Quilter (QLT) Trading Statement Q1 Mar ’26 (4105c)

AuMA: £141.9bn (↑19% from £119.6bn)

Gross Flows: £6.1bn (↑24% from £4.9bn)

Net Inflows: £3.0bn (↑35% from £2.2bn)

Record quarterly core net inflows exceeded £3bn for the first time, representing 9% annualised of opening AuMA. The Affluent segment delivered £2.9bn net inflows (↑30% y/y), supported by strong Quilter Platform volumes and IFA channel growth (+22%). High Net Worth inflows rose 80% y/y to £214m, reflecting stronger new business momentum. Persistency remained stable, while adviser productivity improved 15% y/y to £3.9m annualised gross sales.

Outlook: “We delivered a record quarter for net inflows, surpassing the £3bn threshold, reflecting the strength of our propositions and distribution capabilities.” – Steven Levin, CEO.

Afrimat (AFT) Trading Statement FY26 (3249c)

HEPS: 91.8–99.1c (↑27.0–37.1% from 72.3c)

EPS: 76.9–83.2c (↑22.1–32.1% from 63.0c)

Strong aggregates performance, higher local iron ore volumes, and satisfactory international sales supported earnings growth. Losses in cement moderated, while divestiture of non-core brick, block, and readymix plants progressed, with Competition Commission approval secured though Section 11 approval remains pending. Anthracite supply from Nkomati commenced but will not affect FY26 results.

Outlook: Management expects continued momentum from iron ore and aggregates. “Afrimat is entering FY27 with a stronger, more focused portfolio, positioning the Group for sustainable growth and shareholder value creation.” – Board Statement. Results due 20 May ’26.

Labat Africa (LAB) Trading Statement FY26 (4c)

HEPS: 11.15c (↑96.5–116.5% from 5.40c)

EPS: 8.17c (↓12.9–32.9% from 10.59c)

Revenue: R511m (↑146.8–166.8% from R199m)

NAV: 34.36c (↑44.6–64.6% from 22.23c)

Revenue surged on stronger operational activity, with subsidiaries Classic International and Ahnamu contributing materially after their Feb ’26 year-end. EPS fell despite higher HEPS, reflecting adjustments in headline earnings. NAV growth underscores improved balance sheet strength. Management highlighted that aligning subsidiary reporting periods will add three months of trading, further supporting FY26 results.

Outlook: Enhanced subsidiary performance is expected to sustain momentum. “Labat is entering a new phase of growth, driven by operational improvements and subsidiary contributions, positioning us for stronger shareholder value creation.” – Board Statement.

Results due Aug ’26.

Mondi (MNP) Trading Update Q1 Mar ’26 (16854c)

EBITDA: €212m (down 27% from Q1 ’25 €290m)

Sales volumes rose in Corrugated and Flexible Packaging, supported by capacity expansions and diversified markets. However, lower selling prices and rising energy costs compressed margins. Consumer Flexibles remained stable, while Corrugated Solutions and Paper Bags faced pressure. Heightened geopolitical tensions in the Middle East added volatility, though Mondi’s direct exposure is limited. Three converting plants in Hungary, Poland and Germany will close in 2026, reducing headcount by 450. Cash flow optimisation and cost discipline remain priorities.

“Despite the uncertain outlook, we continue to focus on what we can control — driving operational excellence, rigorous cost and margin discipline, optimising our production footprint and focused cashflow management.” – Andrew King, CEO.

Snippets

Stor-Age Property REIT (SSS) announced the acquisition of Execustore in Ballito, KwaZulu-Natal for R59m, effective 1 Apr ’26. The purpose-built double-storey facility offers 5 700m² GLA with significant expansion potential on 6 600m² of land. Strategically located near Ballito Junction and Lifestyle Centre, the property strengthens Stor-Age’s portfolio in a high-growth corridor, servicing Ballito, Salt Rock, Zimbali and Shaka’s Rock.

For Anglo American (AGL), the $53bn merger with Teck positions it as a copper heavyweight, directly benefiting from structural demand growth in AI, defence, and grid infrastructure. Regulatory approval is expected between Sep ’26 and Mar ’27, reinforcing Anglo’s long-term copper exposure and earnings resilience. Teck’s Q1 profit beat estimates, driven by record copper sales and a 36.7% surge in prices to $5.83/lb. Output rose 32% to 140kt, with Quebrada Blanca contributing 55.5kt. Sales volumes jumped 46% to 155kt, lifting adjusted EPS to C$1.75 vs consensus C$1.15. Rising freight and explosives costs from Middle East tensions may weigh on Q2.