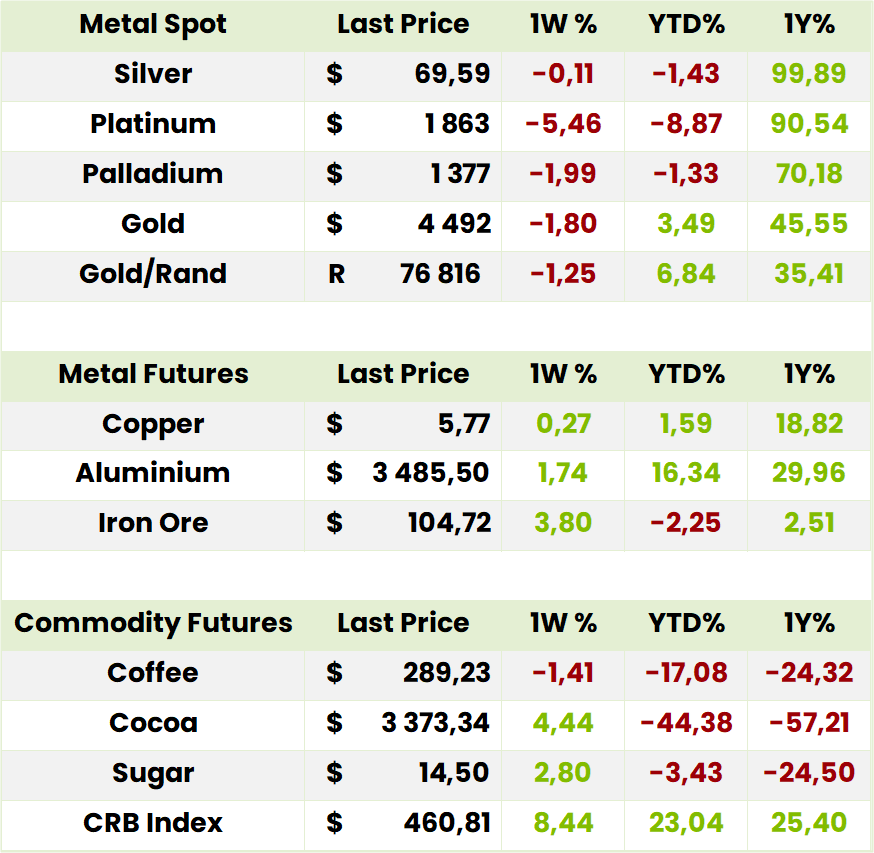

Global Indices

Currencies, Crypto & Commodities

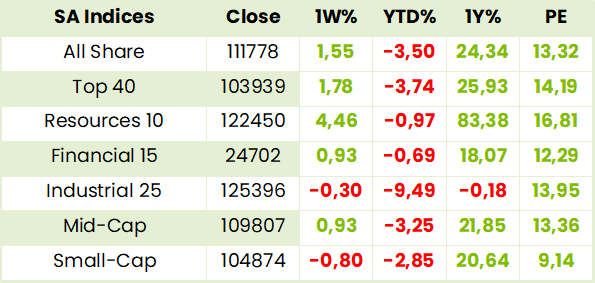

SA Indices

SA Upcoming Indicators & Dividends

*Denotes companies held in the Finova Flagship Portfolio and/or the Finova Retirement Portfolio

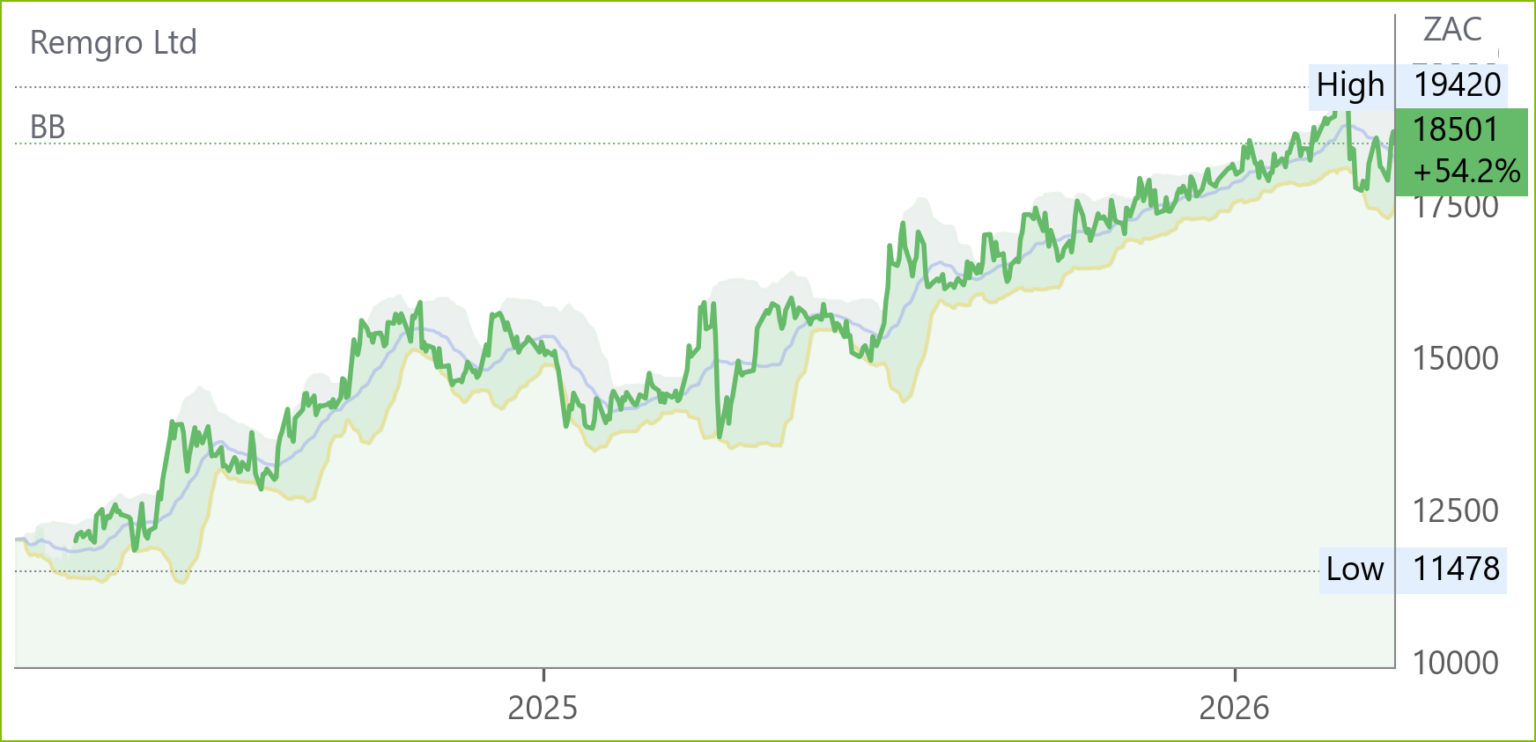

Remgro* (REM) Interim Results for 6M Dec 25 (18501c)

HEPS: 931c (+38.5% from 672c)

EPS: 930c (+41.1% from 659c)

Dividend: 173c interim dividend (+80.2% from 96c)

NAV: R297.03 per share (+1.6% from R292.34)

Headline earnings surged, supported by strong contributions from Mediclinic, Rainbow Chicken, CIVH, Heineken Beverages and a once-off Transnet pipeline refund at TotalEnergies SA. Cash inflows at the centre rose, aided by higher sustainable dividends and the CIVH/Vodacom transaction. Liquidity remains robust, though exposure to Middle Eastern operations via Mediclinic introduces geopolitical risk. Portfolio optimisation and growth are highlighted as key levers for shareholder value creation. “Remgro is confident that portfolio optimisation and growth remain the key levers to unlock further value for shareholders.” – Johann Rupert, Chairman.

Comment: Mediclinic comprised 24% of intrinsic NAV at 31 December and the Middle East comprised 22% of adjusted earnings thereof for the 6 months to 30 September 2025 so, although, with many people moving out of the region for the duration, earnings for 2H26 will be substantially down, we are talking about a maximum hit to the group of around 5%. We are confident of the growth prospects for other major NAV components such as Outsurance (20%), CIVH (9.5%) and Discovery (7%). Although the latter is a portfolio investment, as was Firstrand, we suspect (and hope) it won’t be sold in a hurry. Heineken comprised 7.5% and is now getting its act together with, amongst many other initiatives, expectations of pushing its SA beer (Windhoek, Amstel and Heineken) market share well above the current 20%. It also has high hopes of fast growth in African beer consumption in contrast to easing trends in some developed country markets. The R4.9bn raised from the sale after the half year end of the bulk of its Firstrand investment would, together with the R12bn of cash at the half year end, comprise 10% of intrinsic NAV at 31 December of R297. This was at a 39% discount to then price of 18161c. Bottom line: one doesn’t often get assets like this at such a discount including a war chest to avail oneself of upcoming opportunities in turbulent times such as those to come.

Advtech (ADH) Financial Results FY25 (4090c)

HEPS: 235.8c (+17% from 2024)

EPS: 234.4c (+16% from 2024)

Operating Profit: R2 038.2m (+14% from 2024)

Revenue: R9 330.4m (+10% from 2024)

Dividend: 118.0c per share (Final dividend 73.0c declared)

Advtech delivered strong growth across earnings and revenue, supported by consistent cash generation and disciplined capital management. The board maintained a dividend cover of 2.0x, reflecting confidence in sustainable returns. Normalised earnings rose 17% to R1 297.2m, underpinned by resilient demand in education services. CEO Roy Douglas noted: “Advtech continues to build on its strategic strengths, ensuring long-term shareholder value through quality education and operational excellence.”

Results highlight steady expansion in operating profit and earnings, with dividend uplift reinforcing shareholder confidence.

Comment: management builds a strong case for the continuation of the growth of the 4 year 2021-25 CAGRs: Group revenue was 12%, Operating Profit 16%, Normalised EPS 18%, DPS 24%. Like its peer, Stadio, Advtech is aiming for university status in its tertiary operations which, as at February 2026 saw enrolments up 19% over 2025 at 71467. While SA Schools enrolments were up 1% to 34569, Rest of Africa was up 14% to 13161. Total enrolments were 13% up at 119197. With a Debt: equity ratio of 39% to facilitate ongoing expansion and, on a 3% DY and 16.9x PE Advtech can safely be bought for regular mid-teens or better EPS growth.

MAS (MSP) Interim Results for 6M Dec 25 (1937c)

HEPS: 3.72 eurocps (-21.7% from 4.75 eurocps)

EPS: 1.97 eurocps (-83.6% from 12.01 eurocps)

Revenue: EUR51.9m (+0.2% from EUR51.8m)

Gross Profit: EUR21.9m (-27.2% from EUR30.1m)

NAV: 181 eurocps (+7% from 169 eurocps)

LTV: 21% (down from 25.6%)

Earnings contracted sharply due to weaker Romanian consumption, disposal of higher-yielding assets, and fair value write-downs on Flensburg Galerie. TSR per share rose 7% on NAV growth and buybacks. Operational resilience was evident with 98.2% occupancy and near-100% rent collection. CEO Irina Grigore commented: “MAS remains focused on disciplined capital allocation and long-term shareholder value creation.” Results for FY06/26 due 30 Jun ’26.

Comment: so, Total Shareholder Return of 7% notwithstanding, with results like these and a share price that‘s gone nowhere for 10 years its no wonder PK Kapital thinks it can do better. So should they if the NAV really is (at ZAR 19.62/€) 3551 c! Just to make sure they get a chance, why not help them along by offering them some or all of your shares at any price of your choosing up to, say, 2400? Annualising the halfway Heps of € 3.72 to ZAR 146c makes for a 13.3x PE which is, in any case, the highest in its sector -for no good reason. NB Soon after MAS results were published PK Kapital, which is listed on the Cape Town Stock Exchange, invited MAS shareholders to tender some or all of their shares for sale to PK.

Choppies (CHP) Interim Results for 6M Dec 25 (180c)

Reported in BWP, converted to ZAR @ 1.25

HEPS: 3.1c (-57.5% from 7.3c)

EPS: 4.2c (-31.1% from 6.1c)

Operating Profit: R190m (-20% from R238m)

Revenue: R6,406m (+8.6% from R5,896m)

Gross Profit: R1,259m (+4.4% from R1,206m)

EBITDA: R181m (-28.9% from R255m)

Dividend: 1.0c interim dividend (-37.5% from 1.6c)

Revenue growth was supported by 25 new stores, inflationary tailwinds and volume gains, but profitability fell sharply due to Botswana’s diamond-market slump, government austerity, inflationary costs, and deflationary pressures in Zambia. Liquorama was the only segment to improve margins. Cash generation remained positive, with free cash flow up 65%. “Choppies is building scale now to capture operating leverage during recovery.” – Board Statement.

Grand Parade (GPL) Interim Results for 6M Dec ’25 (199c)

HEPS: 8.8c (↓18.5% from 10.8c)

EPS: 8.8c (↓18.5% from 10.8c)

Dividend: Nil (Dec ’24: Nil)

Profit fell R8.8m to R37.4m, reflecting weaker performance across investments. No interim dividend was declared. Management noted the results are unaudited and short-form, with full details available in the published statement. Outlook remains cautious as the group continues to restructure its portfolio for sustainable growth.

Trading Statements & Updates

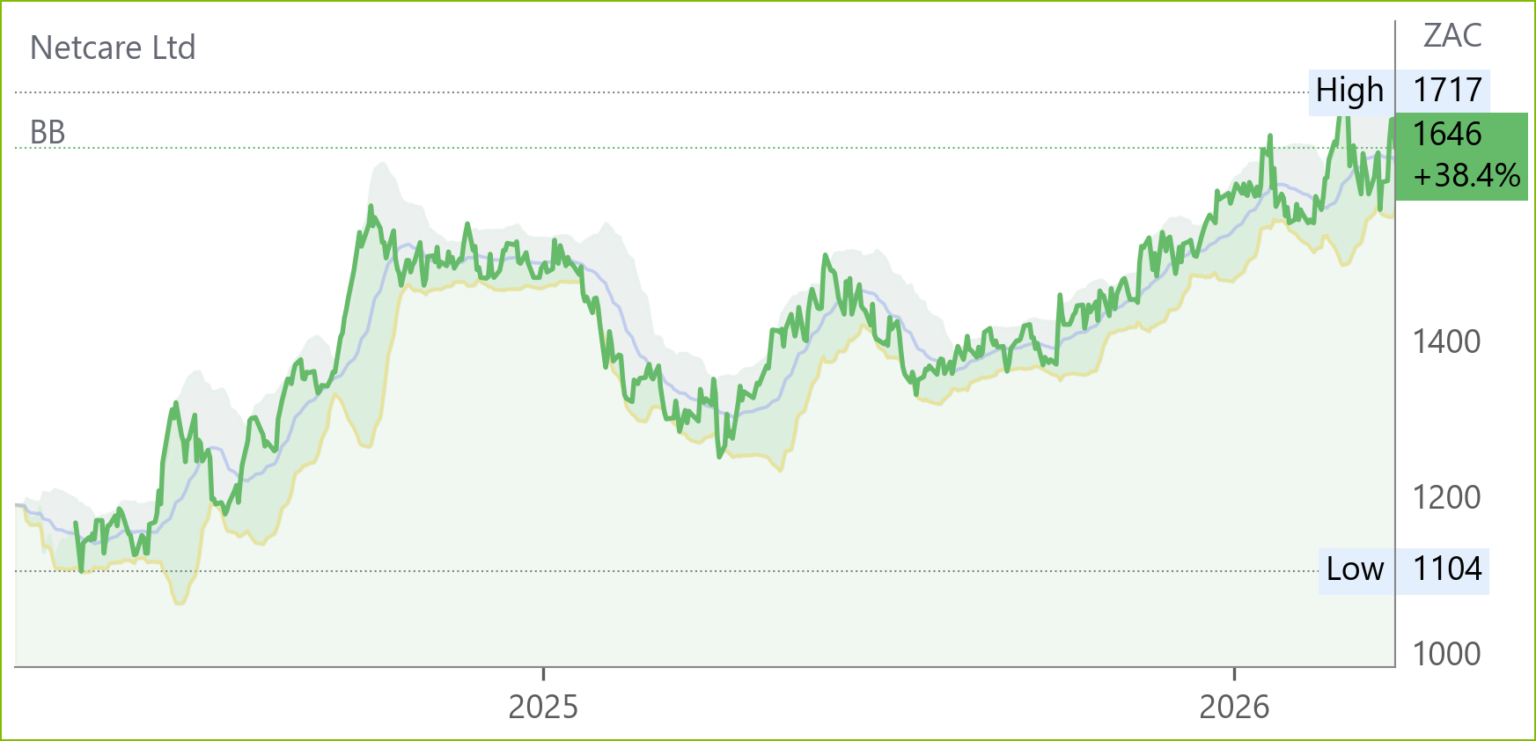

Netcare (NTC) Operational Update for 5M Feb 26 (1646c)

Revenue: +4.5% (vs 5M Feb 25)

EBITDA: Margins slightly higher (vs 5M Feb 25)

Paid Patient Days: +0.8% (acute hospitals +0.5%, mental health +2.9%)

Operating Costs: Well contained

Share Buyback: R292m spent (18.1m shares at avg 1608c) since Oct 25; total 167.1m shares repurchased since Sep 23 (11.6% of issued shares)

Netcare reported resilient performance despite pressures in medical scheme utilisation. Revenue growth and disciplined cost control supported EBITDA margin expansion. Acute hospital activity is expected to strengthen in H2 26, aided by 89 new beds and conversions into higher-demand disciplines. Mental health operations will benefit from the commissioning of the 87-bed Akeso Polokwane facility in Mar 26. CEO Richard Friedland noted: “Improving macroeconomic indicators provide a supportive backdrop for continued operational momentum and reinforce our confidence in long-term growth prospects.” Results due 25 May ‘26.

Snippets

Discovery Limited (DSY) announced that its subsidiary, Vitality Group International, has sold nearly half its stake in Cambridge Mobile Telematics for $49.5 million (≈R831 million). Originally investing $5 million in 2014, Discovery retains strategic rights and an 8.7% shareholding. The disposal yields a $7.9 million gain, excluded from normalised operating profit.

Datatec’s (DTC) Logicalis Germany acquired NetworkedAssets, a Berlin and Wrocław-based software and network automation specialist, effective 24 Mar ’26. The deal establishes a Polish engineering base and strengthens expertise in carrier, data centre, and cloud environments. CEO Jens Montanana said: “The transaction builds on a successful existing relationship, extends Logicalis’ footprint into Poland and adds valuable engineering expertise.”

Jubilee (JBL) Phase 1 drilling at Molefe Mine confirmed continuity of shallow copper oxide mineralisation with consistent grades, extending the mineralised zone by 250m east. Key intercepts included 16m @ 8.01% TCu and 7.5m @ 9.17% TCu. CEO Leon Coetzer said: “We are very excited by these results, which confirm the continuation of high-grade copper reef close to surface.”