Finova Investor Digest

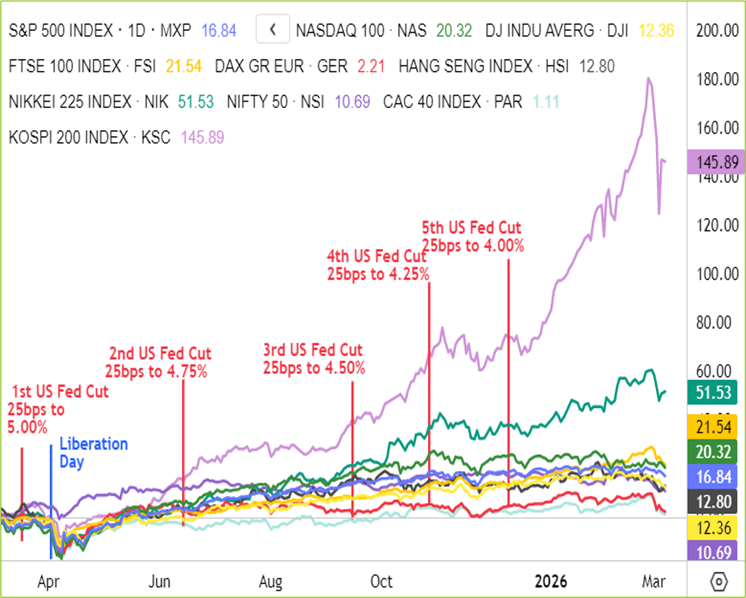

Global Indices

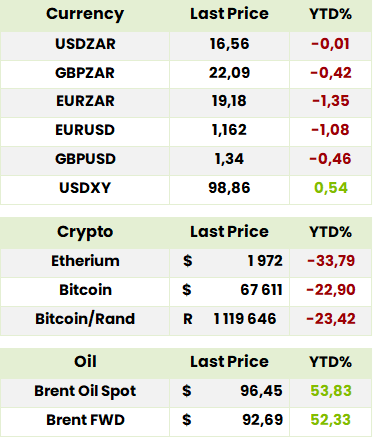

Currencies, Crypto & Commodities

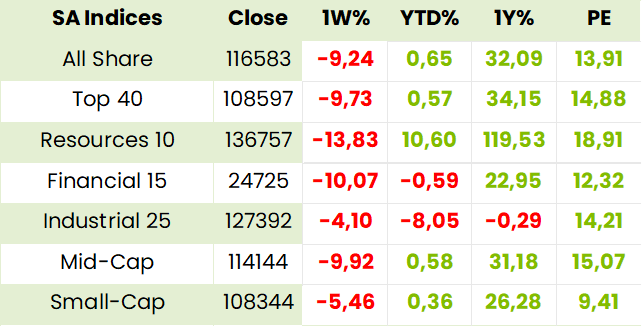

SA Indices

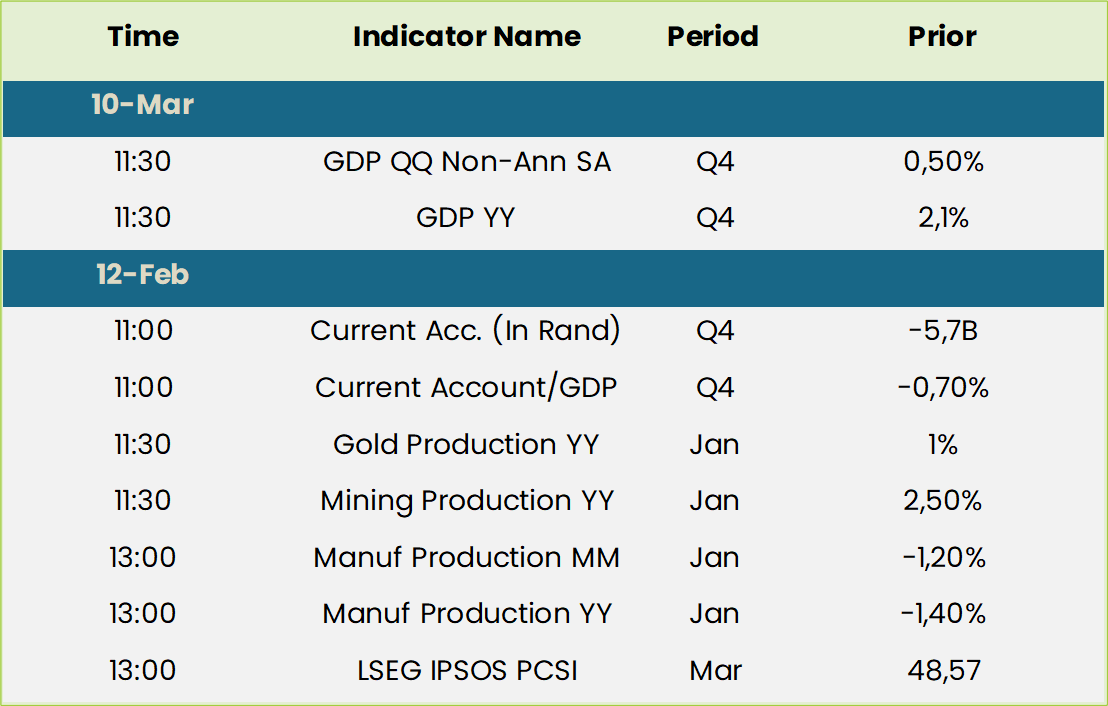

SA Upcoming Indicators & Dividends

SA Equity

*Denotes companies held in the Finova Flagship Portfolio and/or the Finova Retirement Portfolio

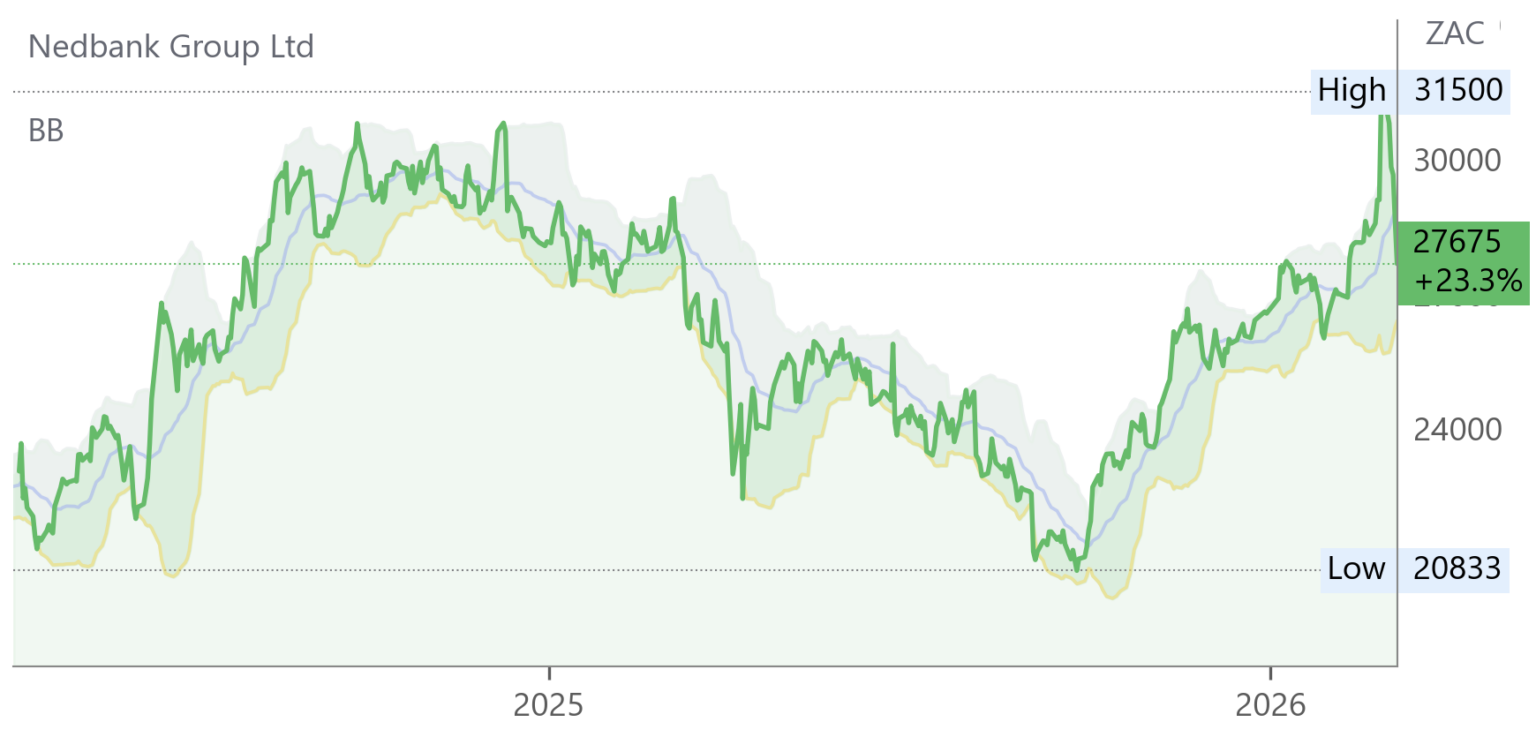

Nedbank* (NED) Financial Results FY25 (27675c)

HEPS: 3 706c (+2% from 3 631c)

EPS: 1 681c (-53% from 3 610c)

Revenue: R73.9bn (+3% from R71.7bn)

Dividend: 2 132c per share (+3% from 2 075c); final dividend 1 104c

Nedbank delivered headline earnings of R17.2bn, up 2%, supported by lower impairments despite higher expenses from a Transnet settlement. EPS fell sharply due to once-off items, while HEPS remained resilient. Strategic highlights included restructuring retail and wealth clusters, acquiring fintech iKhokha, and announcing plans to acquire NCBA Group in East Africa. Digital adoption surged, client numbers reached 8m, and sustainable finance lending exceeded targets. “2025 was a transformative year in which we made bold and swift strategic decisions.” – Jason Quinn, Chief Executive.

Comment: the pedestrian results notwithstanding, CEO Jason Quinn was very upbeat with the phrase

“I am very excited” cropping up frequently not least of course in relation to the jettisoning at last of its decade plus long 21% holding in the largely West Africa based Ecobank. In its place it has agreed to buy a 66% stake in the East African NCDA which will continue to have the remaining 34% listed on the Nairobi Stock exchange. In contrast to Nedbank itself, which has only just reached the 8 million client mark, NCDA has 60million clients and operates In Kenya, Tanzania, Uganda and Rwanda with offices in the Ivory Coast and Ghana. With Nedbank operating in the SADC region plus Mozambique and Zimbabwe with an office in Angola it will begin to be, as from 3Q26, when the deal is expected to go through, a serious Africa player. The FY26 outlook is somewhat muted as, although Quinn says there is strong underlying momentum, this will be partially offset by the non-inclusion of R986m from Ecobank, normalisation of impairments off a low FY25 base as well as negative endowment impact. Nedbank has, however, been the most modestly rated of the Big Four banks and this will begin to change. After the results the share price briefly breached its previous all time high of R309 in 2018 before succumbing to the intensification of hostilities in the Middle East which could well provide attractive buying opportunities for long term re-rating.

FirstRand* (FSR) Interim Results for 6M Dec 25 (8696c)

HEPS: 414.9c (+11% from 374.4c)

EPS: 415.0c (+10% from 376.4c)

Operating Profit: R23.2bn (+11% from R20.9bn)

Revenue: NII +8%, NIR +12%

Dividend: 259c per share (Interim, +18% from 219c)

NAV: 3 989c per share (+8% from 3 700c)

Strong advances and deposit growth, coupled with resilient credit metrics, supported topline momentum. FNB, RMB and WesBank all delivered improved returns, while UK operations faced margin pressure. Net interest margin rose 8 bps, aided by asset-liability optimisation. CET1 capital ratio strengthened to 14.4%. “FirstRand delivered a commendable performance, characterised by strong topline growth and an excellent contribution from non-interest revenue, supported by improving credit metrics.” – Mary Vilakazi, CEO. Outlook remains positive, with NII expected to grow mid-to-high single digits and credit losses trending to the lower end of the cycle range.

Comment: although FirstRand does a lot of “suitcase banking” with deals financed in many African countries it, unlike peers Standard Bank, Absa and, more recently Nedbank, lacks “boots (or branches) on the ground” outside the SADC countries. In the presentation Q & A, however, Mary Vilakazi said that talks to that end had terminated recently but she indicated the bank was still looking to see if something would emerge from the current move towards consolidation in the East African region. It also emerged that, at end of the month, once the amounts for which for which FirstRand is liable in in terms of the UK motor industry commissions saga are announced, and provided they are within what

It has provided, it will have the resources and be free to move decisively into East Africa.

This is probably just as well because, although management is optimistic regarding current operations, it is no doubt aware of the potential longer term threat of competition from the “disrupters” such as Tyme Bank, Pepkor and Bank Zero. Ironically enough, FNB’s famously innovative ex-CEO, Michael Jordaan, is Chairman

of the latter. While the stock is currently well worth holding, this could change depending on the above-mentioned UK announcement.

Aspen Pharmacare* (APN) Interim Results for 6M Dec 25 (13803c)

HEPS: 417.4c (-35% from 645.4c)

EPS: 331.1c (-38% from 537.7c)

Operating Profit: R2.7bn (-31% from R3.9bn)

Revenue: R21.1bn (-4% from R22.0bn)

Gross Profit: R9.6bn (-8% from R10.5bn)

EBITDA: R5.1bn (-13% from R5.8bn)

Commercial Pharmaceuticals delivered 4% CER revenue growth and 11% EBITDA uplift, supported by strong demand for Mounjaro® in South Africa and improved China performance. Manufacturing EBITDA fell sharply (-84%) due to the absence of the prior mRNA contract, though Aspen received EUR25m settlement proceeds. Free cash flow rose to R2.0bn, reducing net debt to R28.6bn. The AUD2.37bn APAC divestment is expected to close by May ’26, eliminating most debt. “Aspen remains focused on executing its strategic priorities, driving sustainable growth and reshaping manufacturing for long-term value creation.” – Stephen Saad, Group CEO.

Comment: to convince an apparently sceptical market, Saad spells out in his presentation how Aspen will achieve its target of restoring most of FY25 Ebitda of R9.6bn by FY27 despite the fact that it will require c.60% Ebitda growth on the remaining Ebitda of R6.0bn. This will include factors such as that manufacturing is now profitable and Mounjaro sales in SA are growing much faster than competing brands and that approval of its own semaglutide generic product by the strict Canadian regulators will encourage approval by numerous Latin American and other markets where patents are expiring. Saad is confident that this product will be much more affordable thus opening up not only the SA mass market but those of Sub Saharan Africa as well. We think Saad has a point when he says the stock is undervalued!

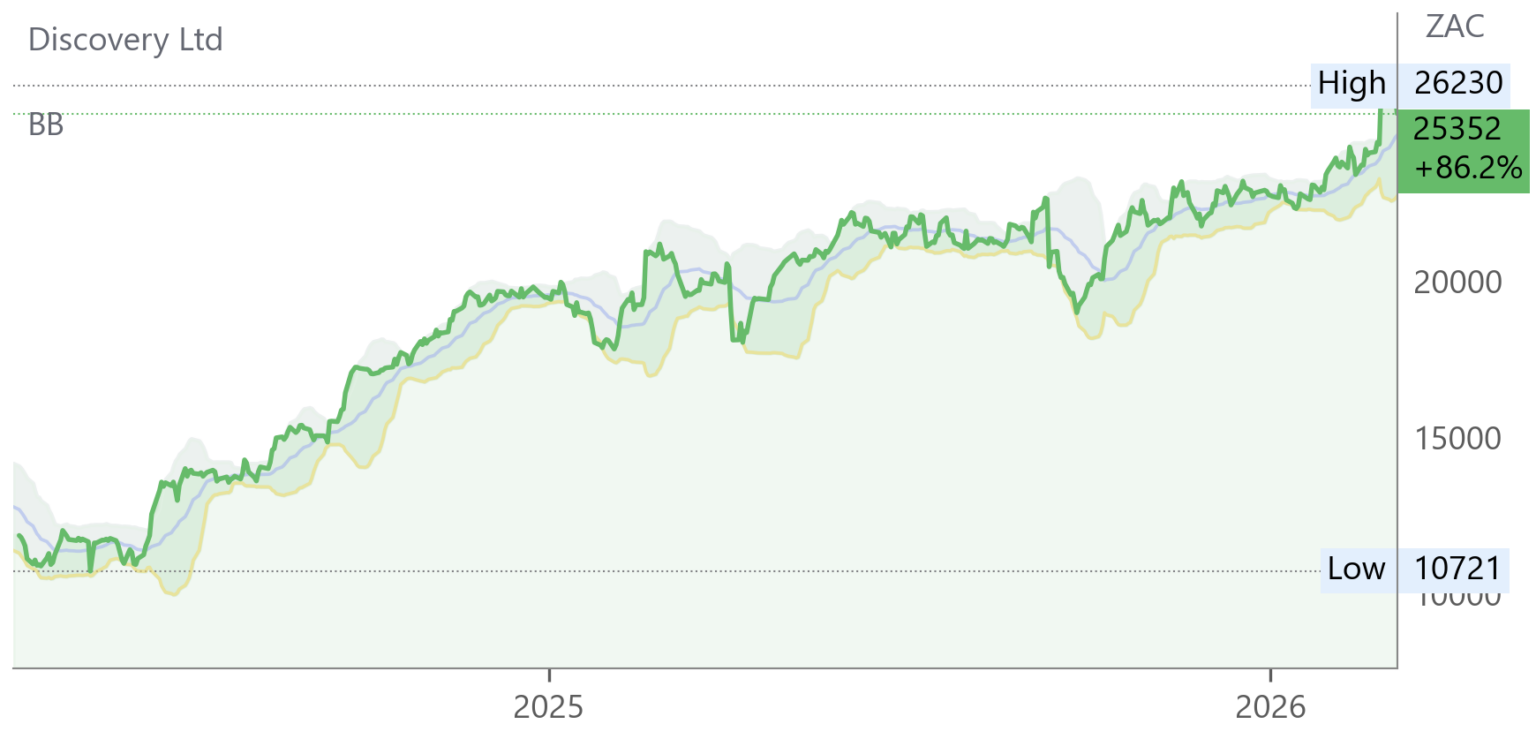

Discovery (DSY) Interim Results for 6M Dec 25 (25352c)

HEPS: 850.0c (+27% from 667.1c)

EPS: 846.6c (+28% from 661.3c)

Operating Profit: R8.9bn (+24% from R7.2bn)

Dividend: 111c per share (interim, +28% from 87c)

NAV: R73.4bn (+25% from R65.7bn)

Discovery delivered strong growth, with headline earnings up 29% and normalised operating profit rising 24% to R8.9bn. South Africa contributed 19% profit growth, while Vitality’s global composite surged 41%. Embedded value increased 15% to R135.8bn, supported by disciplined pricing and AI-driven engagement. Discovery Bank accelerated client acquisition, averaging 1,500 new clients daily. CEO Adrian Gore stated: “2025 was a transformative year in which we made bold and swift strategic decisions.” – Adrian Gore, Group CEO.

Comment: the 850c interim heps annualised would, at 26261c, point to a 15x PE well ahead of its peers in the life sector so, given the 72% hike in share price since when it was around R153ps as recently as August 2024 (this after languishing somewhat since the trading at the same level nearly nine earlier in August 2024), investors could be forgiven for balking at investment now. As ever, however, Adrian Gore supplies some reasons to the contrary. Simply put he says for ten years the group has embarked on heavy capex in various areas most of which are now coming to fruition. Discovery Bank for example is now profitable and growing fast including from customers outside the existing client base. Elsewhere the key factor is the monetisation internationally of the long established Vitality model, together now with AI, getting people to do things better whether it be in the realm of health, driving, or managing their finances. The Ping An Health investment in China had a shoot the lights out year and the link with AIA is but one with major insurers in Asia, the UK and elsewhere with Europe now in its sights. He points out that, with more spend on health care a must, in particular for developed countries, Discovery is scaling as it moves up the J curve with 15% CAGR likely for the next five years. On a PEG ratio of > 1.0x it is still investible, especially if there are more geo-politically induced share price dips.

JSE (JSE) Financial Results for FY25 (16767c)

HEPS: 1 328.9c (+17.7% from 1 128.6c)

EPS: 1 322.3c (+17.1% from 1 129.4c)

Operating Profit: R1.2bn (+20.3% from R1.0bn)

Revenue: R3.4bn (+14.4% from R2.97bn)

EBITDA: R1.38bn (+15.5% from R1.19bn)

Dividend: 961c per share (ordinary, +16%); 100c per share (special)

JSE delivered record results, with NPAT surpassing R1bn for the first time, supported by strong trading volumes and diversified revenue streams. ROE rose to 22%, reflecting disciplined cost management and resilient systems. CEO Leila Fourie noted: “Our results reflect both the current strength of South Africa’s markets and the discipline of a strategy built through the cycle.” – Leila Fourie, Group CEO.

Comment: having doubled in less than two years the share price may well be due for retracement especially since it is currently cum the 961c ordinary as well 100c special dividend. On a 12.6x PE and 5.7% DY, however,

it still shows value. As outgoing CEO Leila Fourie points out the JSE has consistently engaged in transformational systems upgrades and, for example, is currently in advanced talks with buy side and other players under the leadership of NationaL Treasury to facilitate, ultimately, the trading on the JSE of hard currency financial instruments. Currently about R10 trillion is held by South Africans in dollar denominated investments which have to be listed offshore. When government wants to issue dollar denominated bonds it has to go to the likes of Brussels instead of the JSE. Bringing this onshore will benefit buy and sell side investors, clearing house agents, custodians and, of course, the JSE! Ms. Fourie also points to signs of increasing ability to attract listings which could go elsewhere such as Optasia and maybe Coca Cola HBC AG, Tyme Bank, African Bank and Canal Plus. Definitely a stock to consider on that pull back!

Impala Platinum* (IMP) Interim Results for 6M Dec 25 (26700c)

HEPS: 1 035c (+402% from 206c)

EPS: 1 039c (+399% from 208c)

Operating Profit: R9.5bn (+423% from R1.8bn)

Revenue: R60.8bn (+44% from R42.3bn)

Gross Profit: R13.4bn (+532% from R2.1bn)

EBITDA: R18.1bn (+180% from R6.5bn)

Dividend: 410c per share (Interim)

Implats delivered a robust H1 FY26, supported by stronger PGM pricing and operational stability. Safety improved, though one employee was fatally injured in a vehicle accident. Unit costs rose 11% to R23 183/oz, while capex fell 23% to R3bn. Free cash flow surged to R7bn, with net cash at R12.1bn. “Encouraging operational momentum and stability across processing assets provides a solid foundation for delivery for the remainder of FY2026.” – Nico Muller, CEO. All three major PGM markets are expected to remain in deficit during 2026, underpinning pricing strength.

Comment: the price has retreated 23 % from its high last month and, although it is maintaining its production guidance for FY06/26 at between 3.4-3.6moz, in effect unchanged from FY25, this is still lower than 2020 as well as the peak around 3.8moz in 2007. The stock is therefore more of a pure play on pgm prices than the likes of Valterra and Northam which we prefer.

Shoprite (SHP) Interim Results for 26W Dec 25 (25757c)

HEPS: 710.5c (+7.7% from 659.8c)

EPS: 697.1c (+4.5% from 667.3c)

Operating Profit: R7.7bn (+3.5% from R7.4bn)

Revenue: R136.8bn (+7.2% from R127.6bn)

Dividend: 307c per share (interim, +7.7% from 285c)

Shoprite lifted sales by R9.2bn to R136.8bn despite deflationary pricing, with trading profit up 5.9% to R7.7bn. Net profit rose 4.2% to R3.8bn, supported by festive season outperformance. Sixty60 surged 34.6% to R11.9bn, while adjacent businesses grew 70.9%. Supermarkets RSA contributed 84.3% of sales, with Checkers up 8.9%. CEO Pieter Engelbrecht said: “Our results reflect the strength of our planning, marketing and execution during festive season trade.” – Pieter Engelbrecht, CEO.

Woolworths (WHL) Interim Results for 26W FY25 (5204c)

HEPS: 167.4c (+9.6% from 153c)

EPS: 167.4c (+9.6% from 153c)

Operating Profit: R2.0bn (-23.0% from R2.6bn)

Revenue: R42.5bn (+5.4% from R40.3bn)

Gross Profit: R17.0bn (+4.0% from R16.3bn)

EBITDA: R4.6bn (+3.2% from R4.5bn)

Dividend: 118c per share (interim, +10.3%)

Food turnover grew 7.0% with online sales up 23%, while Fashion, Beauty & Home rose 6.2% driven by strong Home (+14%). Country Road Group in Australia delivered modest growth (+2.3%) but margins were pressured by promotions. Cash conversion improved to 109.8% and net debt/EBITDA remains at 1.48x. “We are encouraged by the resilience of our Food and Fashion businesses and remain focused on delivering sustainable growth despite inflationary headwinds in Australia.” – Roy Bagattini, CEO.

Truworths (TRU) Interim Results for 26W Dec 25 (5609c)

HEPS: 495.4c (+1.3% from 489.1c)

EPS: 494.6c (+1.2% from 488.7c)

Operating Profit: R2.72bn (flat vs R2.71bn)

Revenue: R12.5bn (unchanged)

Gross Profit: R6.47bn (flat, margin 51.8%)

Dividend: 321cps (interim dividend, +1.3% from 317cps)

NAV: +4.3% per share

Sales growth was muted at +0.4% with unchanged margins, reflecting tough consumer conditions in South Africa and the UK. Cash generation fell to R2.8bn from R3.3bn, while share buybacks of R746m supported NAV growth. CEO Michael Mark commented: “Truworths delivered resilient results in a challenging retail environment, maintaining margins and strengthening the balance sheet through disciplined capital allocation.” – Michael Mark, CEO.

Blu Label (BLU) Interim Results for 6M Nov ’25 (986c)

HEPS: 44.17c (↓16% from 46.01c)

EPS: -555.56c (↓1,363% from 43.98c)

Operating Profit: -R4.1bn (↓730% from R653m)

Revenue: R8.64bn (↑19% from R7.25bn)

Gross Profit: R1.35bn (normalised)

EBITDA: -R4.1bn (↓730% from R653m)

Dividend: 43.56c interim dividend declared

Explanation: EPS collapsed due to Cell C restructuring losses, while revenue grew 19%. EBITDA swung to a R4.1bn loss, reflecting IFRS accounting impacts from Cell C transactions.

Blu Label progressed its digital platform strategy, with Cell C’s restructuring and listing simplifying its balance sheet and governance. Post period-end, BluEnergy secured a NERSA licence to trade renewable energy, opening new growth avenues. Despite accounting volatility from Cell C, prepaid distribution and payments operations delivered resilient earnings. Dividend payments resumed, signalling confidence in cash generation. “The Group enters the second half with strong operational momentum, improved earnings visibility and a clearer pathway to medium-term value creation.” – LM Nestadt, Chairman.

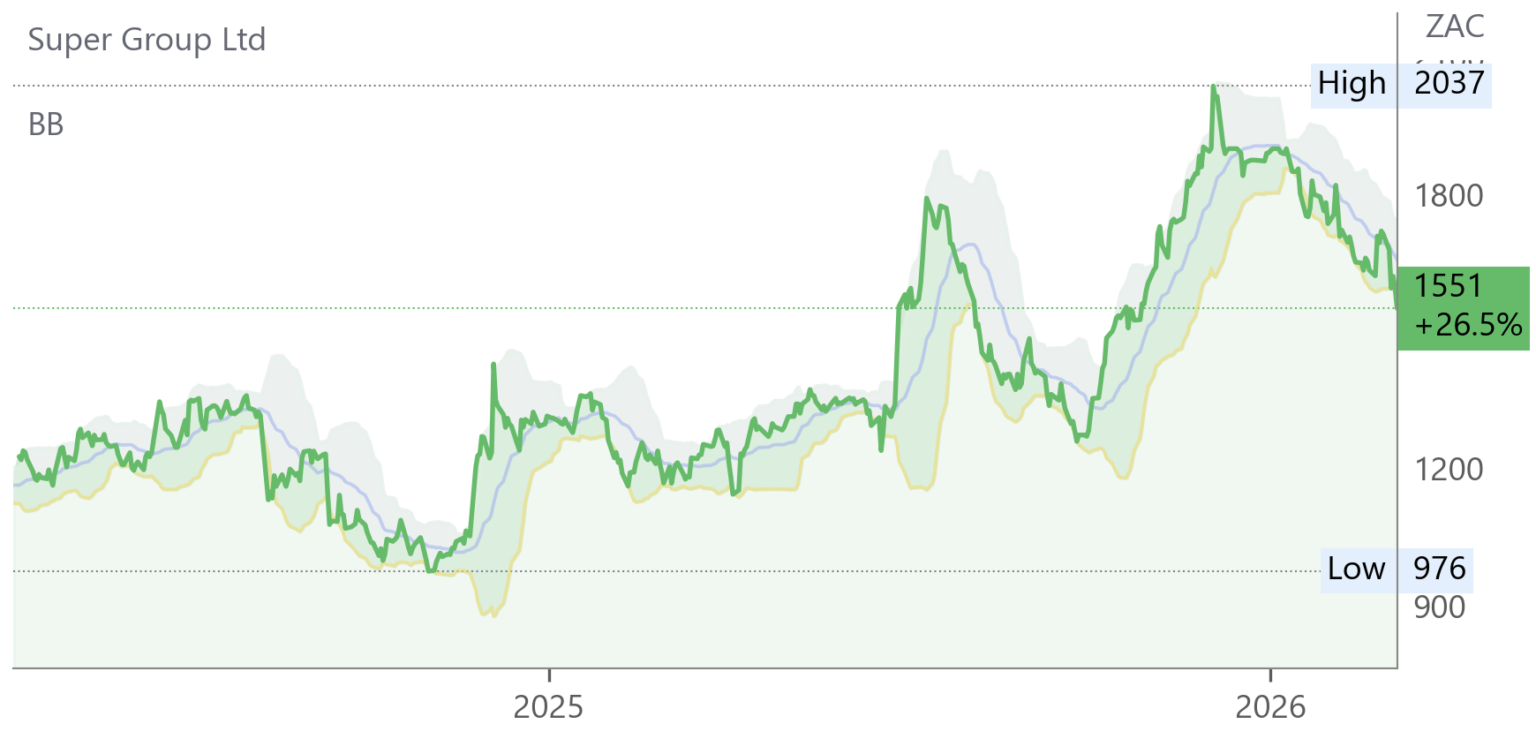

Super Group (SPG) Interim Results for 6M Dec ’25 (1551c)

HEPS: 155.4c (↑28% from 121.4c)

EPS: 157.5c (↑26% from 124.9c)

Operating Profit: R1.10bn (↑8.7% from R1.01bn)

Revenue: R22.68bn (↑7% from R21.20bn)

Gross Profit: R4.87bn (↑136% from R2.07bn)

EBITDA: R1.96bn (↑5.9% from R1.85bn)

Strong supply chain and dealership operations in South Africa, alongside stellar growth at Spanish distributor Ader, drove earnings momentum. Dealerships outperformed the market, boosted by new and used vehicle sales and early adoption of Chinese and Indian brands. Cash generation rose 39% to R711m, reinforcing balance sheet resilience. “Our diversified model continues to deliver robust growth despite global uncertainty.” – Peter Mountford, CEO.

Motus (MTH) Interim Results for 6M Dec ’25 (12479c)

– HEPS: 807c (↑19% from 681c)

– EPS: 805c (↑19% from 675c)

– Operating Profit: R2.74bn (↑8% from R2.54bn)

– Revenue: R57.7bn (↑3% from R56.2bn)

– Dividend: 300c interim dividend (↑25% from 240c)

EPS and HEPS rose in line, supported by stronger vehicle sales and margin expansion. Operating profit grew 8% despite FX volatility, while cash generation surged to R1.9bn.

Motus delivered improved interim results, driven by robust demand for passenger vehicles in South Africa and resilient aftermarket parts activity. New vehicle sales rose 13% locally, while pre-owned volumes increased 5%. Strong cash generation reduced net debt, lowering finance costs by 23%. The Group executed share buybacks and unwound its B-BBEE structure, enhancing shareholder returns. Board changes included the retirement and passing of Executive Director KA Cassel and the resignation of Non-executive Director A Tugendhaft. “Our disciplined execution and strong cash generation provide a solid foundation for sustainable growth and shareholder value.” – OJ Janse van Rensburg, CEO.

Wilson Bayly Holmes Ovcon (WBO) Interim Results for 6M Dec 25 (17423c)

HEPS: 1 086c (+1% from 1 072c)

EPS: 1 086c (+1% from 1 080c)

Operating Profit: R676m (-3% from R695m)

Revenue: R14bn (-4% from R14.7bn)

Dividend: 300cps (interim, unchanged)

NAV: R5.8bn (+4% from R5.6bn)

High activity in South Africa’s roadwork and renewable energy sectors supported performance, with mining infrastructure in West Africa and Zambia adding resilience. UK operations remained steady despite subdued conditions. The order book eased 3% to R36.4bn. “WBHO continues to leverage infrastructure demand while maintaining disciplined capital allocation to support shareholder returns.” – WP Neff, CEO.

Comment: the interims are a little disappointing, after all the talk of increased government infrastructure spending, as is the order book at R263bn (R296bn as at Jun 25). Positives, however, include being named preferred contractor for the Cape Winelands Airport project which is likely to go ahead in 2028, as well as a lengthy list of near orders, orders received after year end, preferred status and expected orders totalling R19bn. On a PE of c. 9.3x and 2.9% DY this is not yet priced in but the market may well want to wait for some of these announcements to start rolling in before doing so.

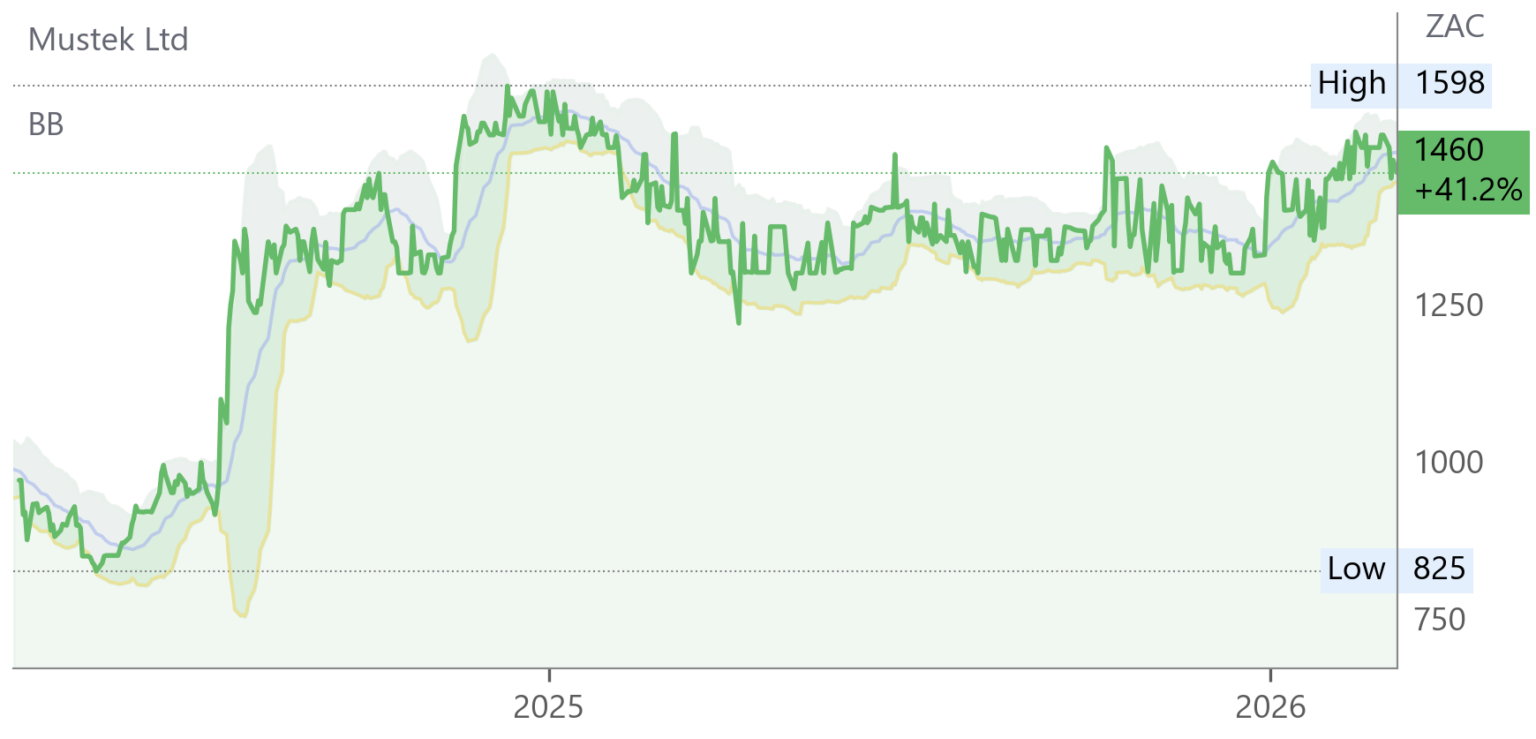

Mustek (MST) Interim Results for 6M Dec ’25 (1460c)

HEPS: 83.54c (↑256% from 23.47c)

EPS: 83.36c (↑262% from 23.01c)

Operating Profit: R94.6m (↓1% from R95.6m)

Revenue: R3.54bn (↓2.4% from R3.63bn)

Gross Profit: 12.6% margin (↓130bps from 13.9%)

HEPS and EPS surged over 250% despite modest declines in revenue and operating profit, reflecting improved earnings quality and balance sheet strength.

Mustek delivered sharply higher earnings, supported by cost discipline and improved asset efficiency, despite softer revenue and margin pressure. Net asset value per share rose 3.7% to 2,930c, reflecting stronger capital management. The Group continues to focus on optimising its product mix and enhancing operational resilience in a competitive ICT environment. A virtual results presentation was scheduled for 25 Feb ’26 to outline strategic priorities. “We remain committed to strengthening Mustek’s position in the ICT sector while delivering sustainable value to shareholders.” – Hein Engelbrecht, Group CEO.

Italtile (ITE) Interim Results for 6M Dec 25 (890c)

HEPS: 60.6c (-14% from 70.1c)

EPS: 60.9c (-14% from 70.6c)

Operating Profit: R1.0bn (-14% from R1.2bn)

Revenue: R6.1bn (unchanged)

Dividend: 24.0c per share (interim, -14% from 28.0c)

NAV: 637.4c (-6% from 678.1c)

Results were impacted by weak demand, dumping of cheap imports, and rising input costs. CTM volumes fell 3%, while Italtile Retail gained market share. TopT struggled against informal traders, though four new stores are planned. Ceramic Industries faced difficult trading conditions with 77% utilisation. CEO Lance Foxcroft will step down in Jun ’26, with Brandon Wood appointed CEO Designate. “We believe there is more potential to leverage our world-class technology to ensure enhanced quality and additional product innovation, as we drive efficiencies and improve productivity to mitigate selling price deflation.” – Lance Foxcroft, CEO.

Operating Updates & Trading Statements

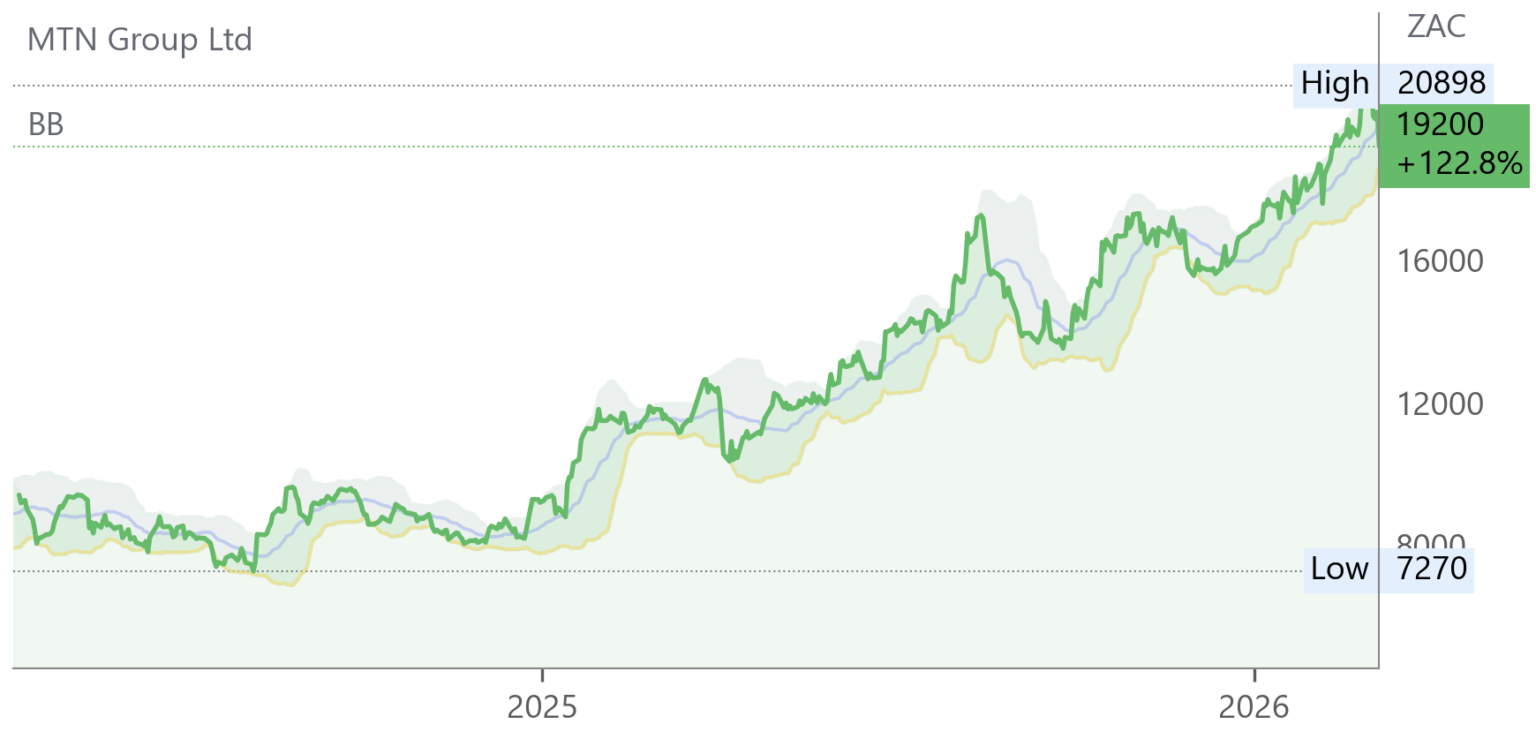

MTN* (MTN) Trading Statement for FY25 (19200c)

HEPS: 1 264–1 284c (>1000% from 98c)

EPS: 1 062–1 168c (>300% from -531c)

Revenue: Strong growth across Nigeria, Ghana, and other markets

MTN anticipates a strong FY25 performance, driven by robust service revenue and profitability in Nigeria and Ghana, offsetting competitive pressures in South Africa. EPS recovery reflects reduced impairments, while HEPS surged on improved operational momentum. Restatements in Ghana marginally improved FY24 comparatives. Results due 16 Mar ’26.

Sanlam* (SLM) Trading Statement FY25 (9209c)

HEPS: 723–819c (-25% to -15% from 964c)

EPS: 694–801c (-35% to -25% from 1068c)

Operating Profit: NRFFS 694–767c (-5% to +5%)

HEPS and EPS contracted sharply due to corporate activity, disposal gains in 2024, and negative investment variances linked to long-dated bond yield anomalies. Net client cashflows more than doubled, while new business volumes rose strongly across life and general insurance. Discretionary capital increased R3.94bn, enhancing balance sheet flexibility. “We continue to deliver strong growth and operating performance amid a turbulent macroeconomic backdrop, positioning us to deliver sustainable value for our shareholders.” – Paul Hanratty, Group CEO.

OUTsurance* (OUT) Trading Statement for 6M Dec 25 (6863c)

HEPS: 132.9c (+11% to +17% from 119.6c)

EPS: 132.9c (+11% to +17% from 119.6c)

Operating Profit: R2.22bn (+10% to +15% from R2.02bn)

Strong premium growth and expense efficiency in South Africa offset higher natural peril losses in Australia. OUTsurance Life delivered solid new business growth, while Ireland remained in scale-up phase with expected break-even ahead. Equity market gains supported earnings despite lower interest rates. CEO Danie Matthee commented: “OUTsurance continues to deliver resilient operational performance, underpinned by disciplined growth and efficiency across our core markets.” Results due 11 Mar ’26.

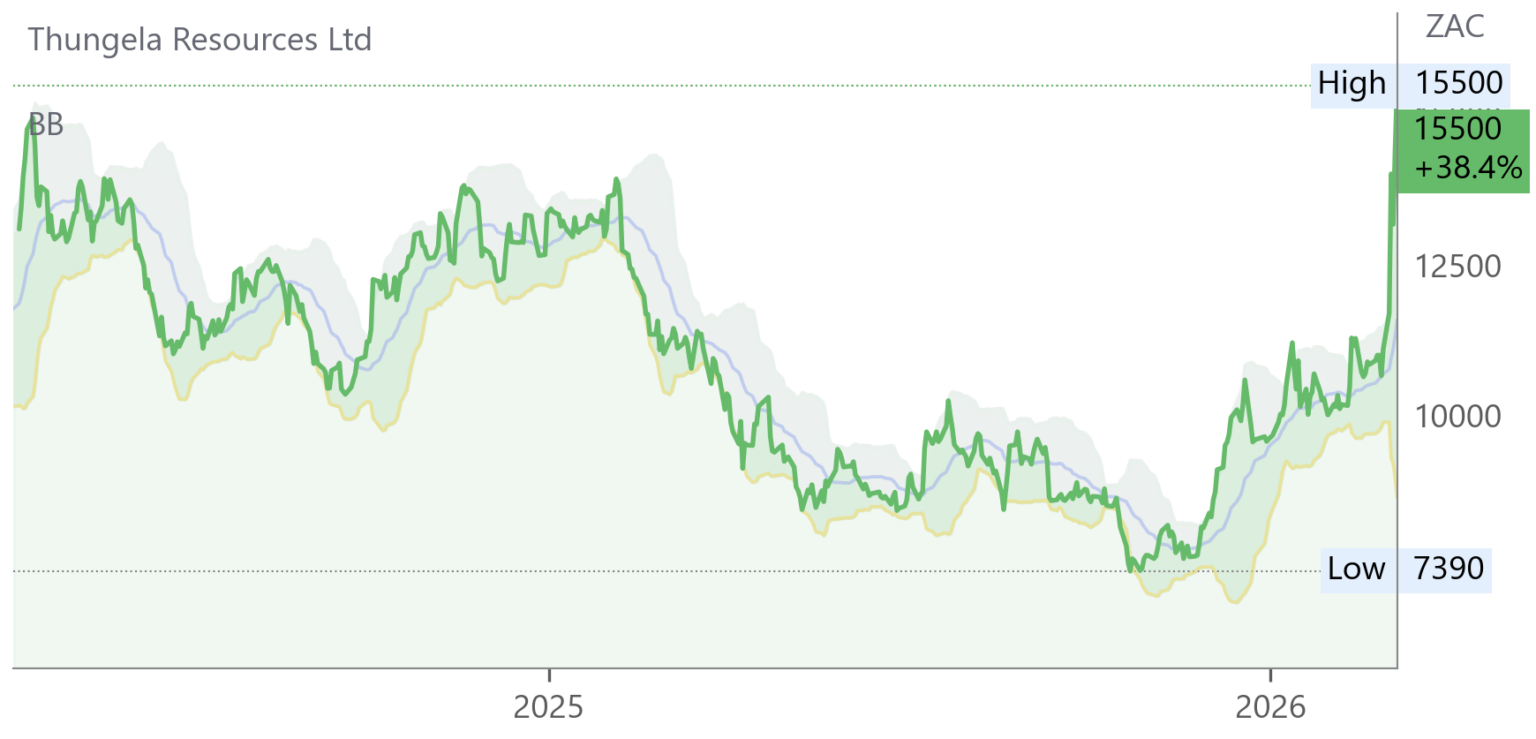

Thungela Resources (TGA) Trading Statement for FY25 (15500c)

HEPS: 5.50c – 7.50c loss (>100% decrease from +25.59c)

EPS: 53.50c – 56.00c loss (>100% decrease from +26.76c)

Revenue: Impacted by weaker coal prices

Thungela expects a headline loss of R0.7–R1.0bn and a net loss of R7.0–R7.3bn for FY25, driven by R8.8bn impairments across South Africa and Australia due to softer coal prices and stronger local currencies. Deferred tax assets of R1.1bn were not recognised, further reducing earnings. Despite losses, cash flow and liquidity remain intact. Results due 23 Mar ’26.

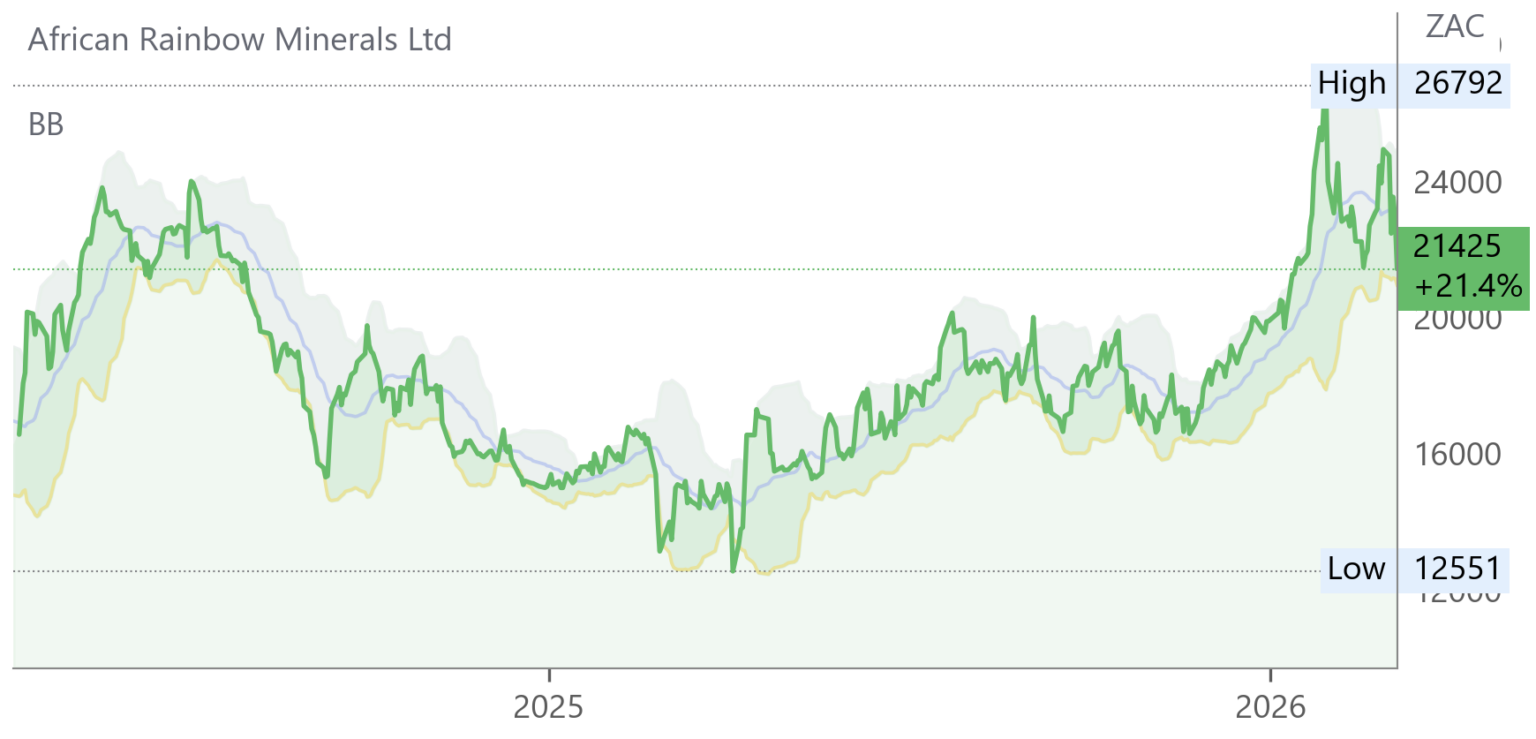

African Rainbow Minerals (ARI) Interim Results for 6M Dec 25 (21425c)

HEPS: 866c (+12% from 775c)

EPS: 1220c (+72% from 711c)

Revenue: R8.4bn (+32% from R6.4bn)

Dividend: 500c interim dividend per share

EPS rose significantly due to stronger PGM basket prices and disposal gains, while HEPS growth was modest. Revenue increased 32% on higher commodity prices, though iron ore and manganese earnings were pressured by exchange rates and weaker volumes. Safety performance improved with record fatality-free shifts, and renewable energy integration commenced at platinum operations. Bokoni Mine suspended milling to focus on ore reserve development. “Collaborative partnerships in logistics reform are restoring performance and delivering competitive, value-accretive solutions for long-term sustainability.” – Mike Schmidt, CEO.

Optasia (OPA) Trading Statement FY25 (2001c)

HEPS: 3.31–3.46USc (+7–12% from 3.09c)

EPS: 3.31–3.46USc (+7–12% from 3.09c)

Revenue: $261.6m–$269.1m (+73–78% from $151.2m)

EBITDA: $112.7m–$116.5m (+50–55% from $75.1m)

Optasia, listed on the JSE in Nov ’25, reported strong FY25 growth with revenue up over 70% and EBITDA rising more than 50%. Normalised EPS increased 45–50% after excluding IPO-related costs. Momentum was driven by airtime credit and micro-financing solutions. Management highlighted resilience and scalability of its AI-powered fintech model. Results due 16 Mar ’26.

Afrimat (AFT) Business Update and Pre-Close Briefing Session (3482c)

Revenue: Growth in Aggregates; Cement volumes up; Iron ore stable

Operational execution remained strong, with notable progress in aggregates and moderated cement losses. Non-core brick, block, and readymix businesses were sold, generating cash for debt reduction. Domestic iron ore sales to AMSA improved, while international iron ore volumes were constrained by rail capacity. Anthracite volumes fell due to ferrochrome smelter shutdowns, partly offset by higher exports. Rare earths project testing advanced, positioning Afrimat for global competitiveness. “Afrimat has invested significant time to ensure each segment is positioned to navigate South Africa’s new realities, while Lafarge acquisition strengthens our quarrying roots.” – Management statement.

ADvTECH (ADH) Trading Statement FY25 (3971c)

HEPS: 229.9–241.0c (+14–19% from 202.2c)

EPS: 229.9–241.0c (+14–19% from 201.7c)

NEPS: 229.9–241.0c (+14–19% from 202.5c)

ADvTECH anticipates double-digit earnings growth for FY25, driven by continued student enrolment expansion across its education divisions. NEPS is disclosed to exclude one-off transactions and corporate action costs, providing a clearer view of underlying performance. Enrolment momentum into 2026 remains strong, supporting revenue visibility. “Our growth trajectory reflects the resilience of our education model and the demand for quality learning solutions.” – Roy Douglas, CEO. Results are expected to be released on 23 Mar ’26.

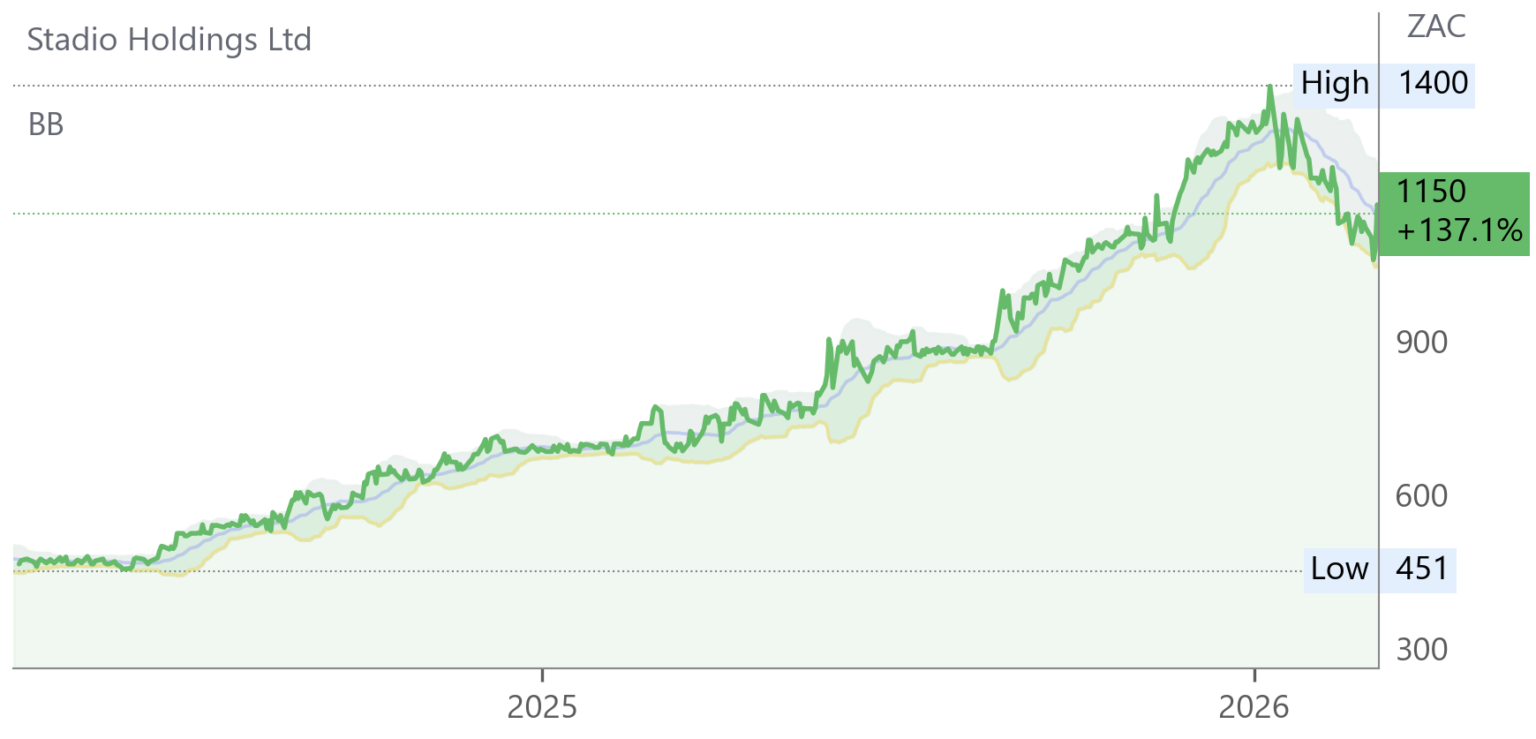

Stadio (SDO) Trading Statement FY25 (1150c)

HEPS: 36.9–40.1c (↑17.5–27.7% from 31.4c)

EPS: 37.0–40.1c (↑19.7–29.8% from 30.9c)

Stadio reported strong earnings growth, with both EPS and HEPS rising by over 17% year-on-year, reflecting resilient demand for private higher education. Core HEPS also increased, signalling underlying operational strength. CEO Chris Vorster noted that the group continues to expand its reach and enhance student offerings, while CFO Ishak Kula highlighted disciplined financial management. Results due 17 Mar ’26.

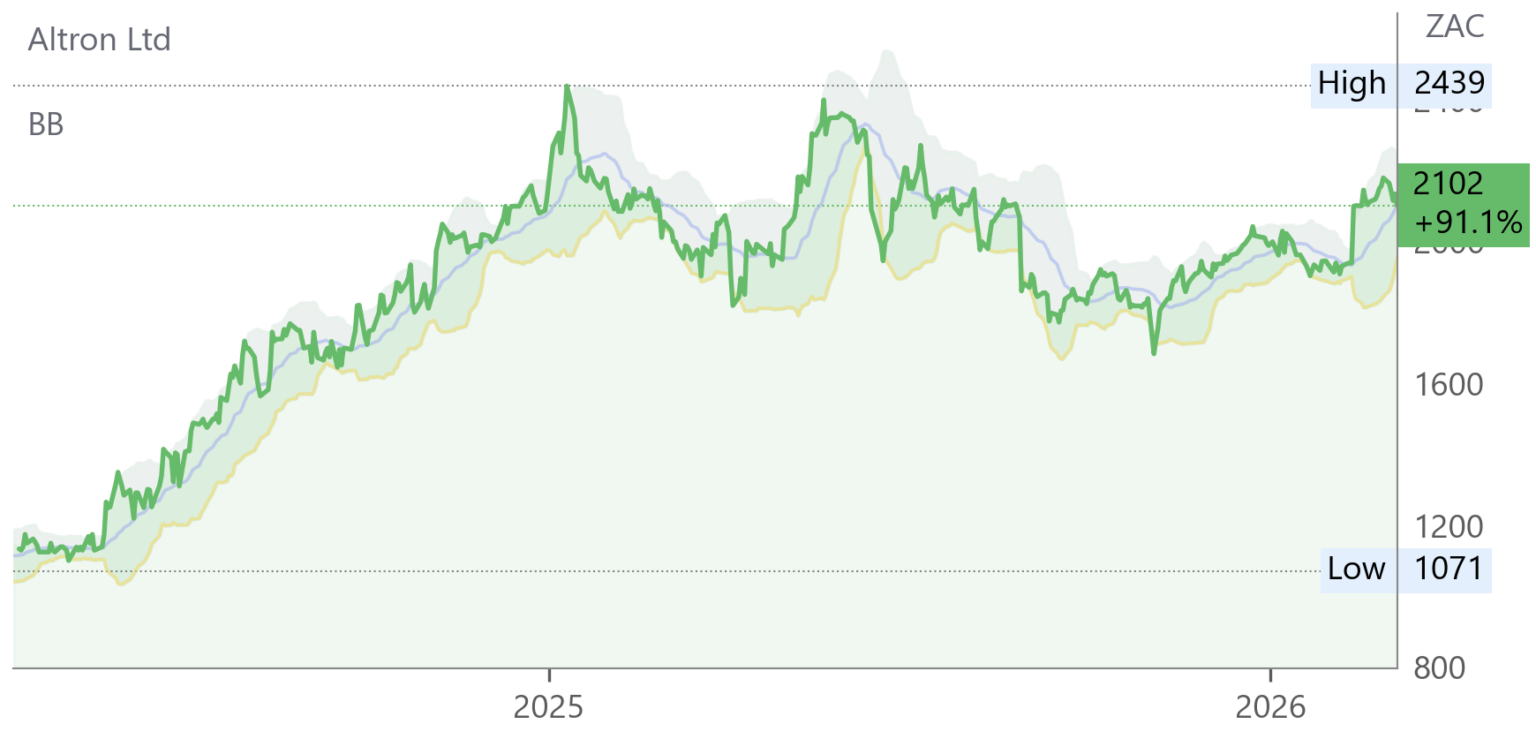

Altron (AEL) Voluntary Operational Update (2102c)

HEPS/EPS: Expected ↑ >30% YoY for FY26

Operating Profit: ↑ >20% YoY

EBITDA: Low double-digit growth

Momentum from H1 FY26 carried into H2, with Platforms contributing ~45% of revenue and ~90% of EBITDA. Netstar delivered strong growth in South Africa with early traction in Australia, while FinTech achieved high-teen revenue growth and >80% annuity income. HealthTech maintained double-digit profit growth. IT Services showed recovery after restructuring, with Digital Business returning to operating profitability. Cash generation strengthened, supported by >65% annuity-based revenue. Altron will conclude its Accelerated Growth phase in FY26 and transition to “Transformative Growth.” Results due 25 May ’26.

Snippets

Kore Potash (KP2) acquired a 0.46% stake in Sintoukola Potash SA (SPSA) from MGM for US$1m, funded from cash reserves. It now holds 97.46% of SPSA, with rights to buy MGM’s remaining 2.54% if a takeover offer completes within 12 months. Full ownership would strengthen control of the Kola Project, subject to the Republic of Congo’s 10% free carry entitlement.

KAP (KAP), holding company of Safripol, confirmed arbitration over ethylene pricing with Sasol was resolved in Safripol’s favour, validating its supply agreement interpretation. Sasol may seek limited High Court review, but pricing is largely settled. The volume commitment dispute remains under Competition Commission and Tribunal processes. As Safripol materially contributes to KAP’s earnings, outcomes are strategically significant and resolution is expected to be lengthy.

Merafe (MRF) confirmed in-principle support from Eskom and Government for a proposed 62c/kWh electricity tariff for ferrochrome smelters, subject to NERSA approval. Terms must be commercially viable to ensure long-term stability. The Glencore-Merafe Chrome Venture extended its s189 consultation deadline to 31 Mar ’26, but warned that if agreement is not reached, retrenchment processes will proceed. The Venture remains committed to constructive engagement with stakeholders.

Labat Africa (LAB) announced the acquisition of a 20% equity interest in Mondau, Lda, a Mozambique-based AI and advanced computing company, for R30m cash. Mondau specialises in generative AI platforms, GPU infrastructure, AI-driven security, and industrial applications, with FY25 pre-tax profit of USD 8m and NAV of R150m. The deal provides Labat exposure to hard currency revenue streams and positions it within Africa’s fast-growing AI-enabled mobile money ecosystem, where sub-Saharan Africa accounts for ~70% of global transaction value. No shareholder approval is required.