Finova Investor Digest

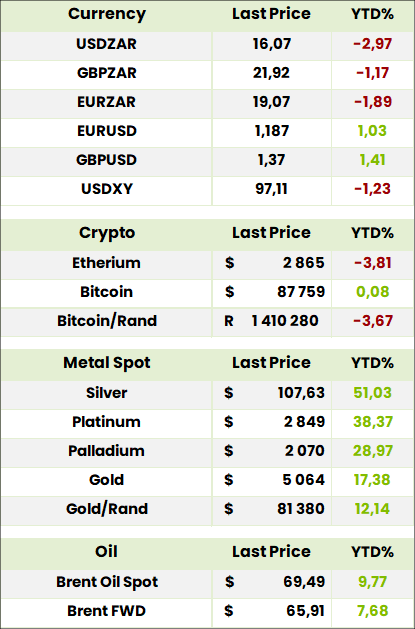

Global Indices, Currencies, Crypto & Commodities

Global Indices 1 year to Date

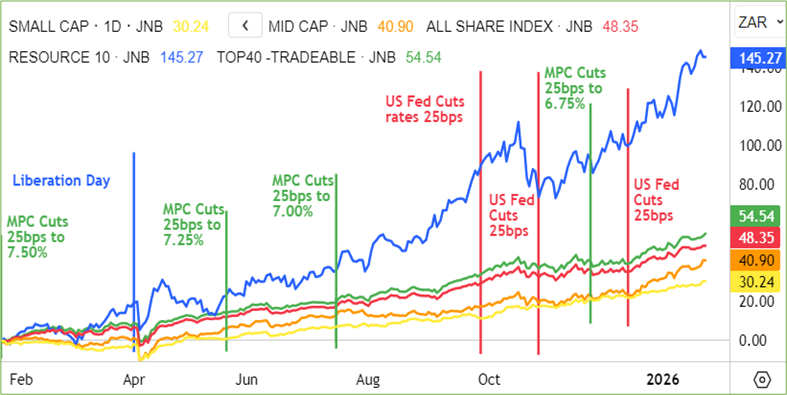

SA Indices

SA Upcoming Indicators & Dividends

SA Equity

Nedbank (NED) Proposed Acquisition of NCBA (27355c)

Nedbank intends to acquire 66% of NCBA for ~R14bn, split ~R11bn in shares (80%) and ~R3bn cash (20%). The deal implies ~9% dilution and ~3% NAV impact, totalling ~11% of market cap. Valuation equates to ~1.4x Jun ’25 NAV, a premium of ~10% to current NCBA price and ~40% to pre‑speculation levels.

NCBA, formed from the merger of NIC Group and Commercial Bank of Africa, operates 122 branches across East Africa, holds KES665bn in assets, and disburses over KES1tn in digital loans annually. It has averaged 19% ROE since 2021, with FY24 profit up 2% but PBT down ~1% due to weaker core banking, offset by strong digital (+74%) and non‑banking (+37%) growth. H1 ’25 performance improved with PBT +11%. Nedbank highlights complementary strengths in NCBA’s regional brand, digital reach, and customer base, aligned with its corporate banking expertise and balance sheet. “The Proposed Transaction brings together two organisations with highly complementary strengths.” — Jason Quinn, CEO.

Comment: Jason Quinn is following his exit from the stagnant West African investment in Ecobank with better growth prospects in the East African NCBA. The generous dividend yield makes its worth holding despite the initial earnings dilution.

Pepkor (PPH) Banking Strategy Update (2655c)

Pepkor’s planned entry into banking leverages its retail footprint, brand strength, and customer acquisition engine. Analysts estimate potential cost savings of ~R380m (~6.4% of Group earnings) through efficiencies in payments and funding, alongside revenue opportunities in Value Added Services, insurance, and retail credit. Competition with Capitec is expected to intensify, particularly in the sub‑R15k/month income segment, though initial impact may be muted. Risks include capital intensity, regulatory hurdles, and execution complexity, but Pepkor believes its Cloudbadger platform offers a cost‑effective base.

Comment: the latest entrant into the low cost mass banking arena certainly warrants consideration at a time when investors are increasingly beginning to price in the prospects of somewhat faster growth than seen for years.

Clicks (CLS) Trading Update for 20W to 11 Jan ’26 (31470c)

Group turnover rose 7.4% to R19.5bn, driven by pharmacy sales up 9% and strong Black Friday and festive demand. Retail sales increased 6%, with comparable sales up 3.7% on 2.4% price inflation and 1.3% volume growth. Distribution turnover grew 11.4%, though bulk agency turnover fell 20.2% after contract losses. A warehouse system delay in Cape Town reduced product availability, impacting sales by ~R120m, but recovery is underway. “Performance was supported by robust pharmacy growth and festive trading, despite competitor discounting and operational challenges.” — Bertina Engelbrecht, CEO.

Comment: Clicks is one of the no name brand “culprits” Tiger Brands CEO Jaart Kruger was saying were impacting sales of the established brands. The recent downtick in share price, presumably on the warehouse system hiccup, offers an opportunity to acquire the stock on what for it is an unusually attractive PE.

Truworths (TRU) Business Update for 26W Dec ’25 (6036c)

HEPS: 489–499c (0% to 2% vs Dec ’24)

EPS: 489–499c (0% to 2% vs Dec ’24)

Revenue: R12.5bn (flat vs Dec ’24)

Retail sales were unchanged at R12.5bn for the 26 weeks to 28 Dec ’25. Truworths Africa sales fell 3.6%, with cash sales down 5.8% but online sales up 23.3%, now 7.4% of segment turnover. Credit discipline reduced gross trade receivables by 2.1% to R6.9bn. Office UK grew sales 6.4% in Sterling, supported by store remodelling and online growth (+7.5%), lifting Rand sales to R4.5bn. Macro conditions in SA remain challenging, though early signs of improvement are evident. Results due 26 Feb ’26

Operating Updates & Trading Statements

BHP (BHG) Operational Review HY26 (54060c)

EBITDA: Negative EBITDA reported for WA Nickel and Potash (~US$100m, ~US$150m impact)

Copper output held steady at 984 kt, with guidance lifted to 1,900–2,000 kt for FY26. Escondida achieved record concentrator throughput, while Antamina raised guidance on stronger grades. Iron ore production rose 2% to 134 Mt, with WAIO delivering record shipments. Steelmaking coal output increased 2% despite geotechnical challenges at Broadmeadow, while energy coal rose 10%. A US$2 bn WAIO power network transaction with Global Infrastructure Partners bolstered balance sheet flexibility. BHP’s Jansen potash project in Saskatchewan is a multi stage development targeting first production by mid 2027. Phase 1 will deliver 4.35 Mtpa capacity, with long life reserves supporting expansion. Construction progress remains on track, with shafts and surface infrastructure advancing. Positioned to meet rising global fertiliser demand, Jansen underpins BHP’s diversification strategy and long term growth in crop nutrients. “We’re investing for the decade ahead, with a significant copper growth pipeline and a pathway to ~2 Mt of attributable copper production in the 2030s.” — Mike Henry, CEO. Results due 17 Feb ’26

Comment: while Mike Henry is right about BHP’s copper prospects, it is not the only copper play, the outlook for iron ore is somewhat muted and questions are being asked about the rising costs at the massive Jansen potash project in Saskatchewan where production is scheduled to commence in mid-2027 with breakeven planned for 2027.

South32 (S32) Quarterly Report Dec 25 (4879c)

Dividend: US$117m ordinary dividend (fully‑franked); US$35m buy‑back in H1 FY26

Alumina output rose 3% to 1,893 kt, with Brazil Alumina achieving record volumes. Aluminium production increased 2%, while Hillside tested maximum capacity despite load‑shedding. Sierra Gorda delivered strong copper and by‑product volumes, generating US$180m distributions. Manganese surged 58% in Australia, aided by recovery post‑Cyclone Megan. Cerro Matoso divestment simplified the portfolio, while Hermosa construction advanced with US$338m invested in shafts and surface infrastructure. Mozal Aluminium will enter care and maintenance in Mar ’26 due to power constraints. “Our consistent operating performance, combined with strengthening market conditions, enabled us to maintain a strong financial position while investing in growth options and delivering returns to shareholders.” — Graham Kerr, CEO.

Comment: with aluminium, copper and manganese prices unlikely to recede soon the FY06/26 interims can safely be awaited despite the share price action. The likely closure of Mozal Aluminium, despite its highly important contribution to the Mozambican economy, comprised only 1% of Group Ebit. Hillside Aluminium, which still enjoys a decades old low power price with Eskom, contributes only 1.5% to group Ebit.

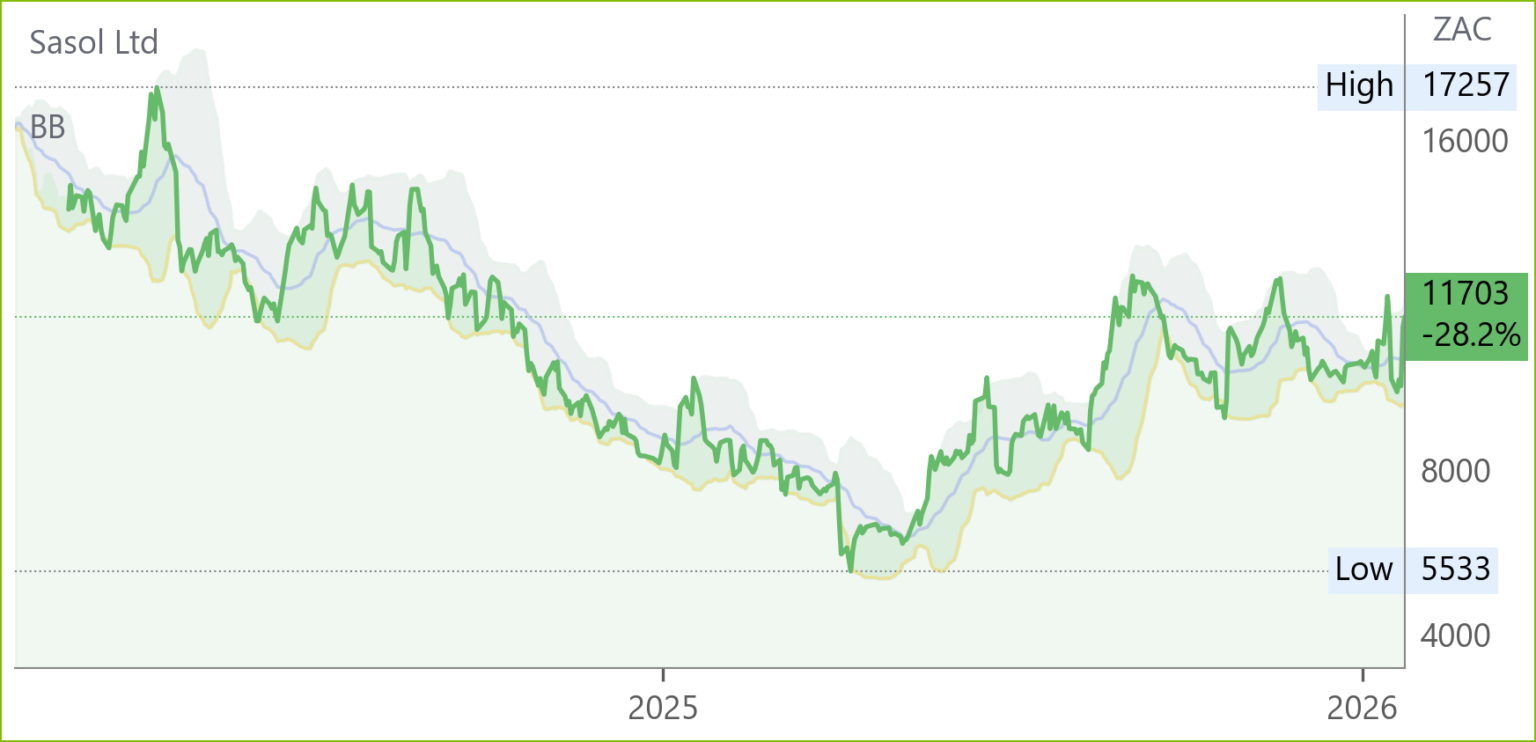

Sasol (SOL) Business Performance Metrics for 6M Dec 25 (10853c)

Operational stability improved with Secunda production supported by the destoning plant reaching beneficial operation in Dec ’25. Natref delivered stronger output, aided by Prax SA capacity, while fuels sales volumes rose through higher‑margin channels. Chemicals Africa volumes increased, though global softness and outages at the Louisiana JV weighed on revenue. A third low‑carbon boiler was commissioned at Natref, advancing decarbonisation. Sasol secured an electricity trading licence, reinforcing integrated power ambitions. Fuel sales guidance lifted to 5–10% above FY25, though gas volumes revised down due to PSA and CTT delays. “We remain focused on what is within our control and responding proactively to changes in the operating environment.” — Simon Baloyi, CEO. Comment: the improvement in mining operations and fuel sales volumes is indeed encouraging as well as the fact that performance is mostly in line with the Capital Markets Day guidance for ebitda growth from R60n in FY24 in SA to R64-71bn in FY2. Sasol is, however, more sensitive to the ZAR/$

exchange rate than to the oil price which no doubt is one of the reasons for the reference to the operating environment “remaining challenging”. Current strength in the oil price

and ongoing operational improvement, however, warrant holding for the interims.

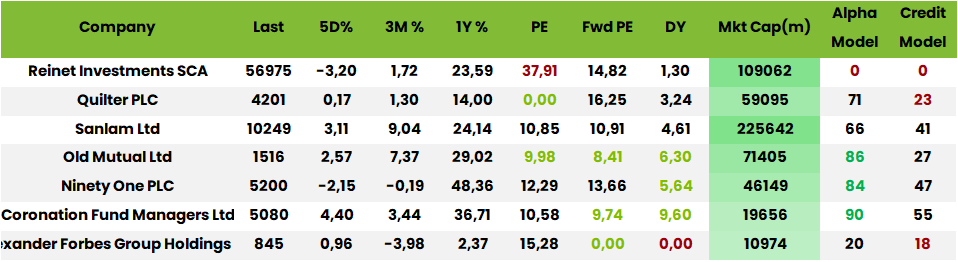

Reinet (RNI) Management Statement Q3 Dec ’25 (56975c)

Net asset value (NAV) at 31 Dec ’25 was €6.6bn, down €69m (‑1%) from Sep ’25, equating to €36.24 per share (Sep ’25: €36.62; Dec ’24: €38.12). NAV has compounded at 8.4% p.a. since Mar ’09, including dividends. €15m of commitments were funded during the quarter. In Jul ’25, Reinet agreed to sell its entire holding in Pension Insurance Corporation Group to Athora Holding, with completion expected in 2026. The portfolio remains diversified across financial services, luxury, and private equity.

Comment: the NAV discount is 17% and following the deal completion this year the portfolio will be in Swiss francs and very cash heavy. Regardless of whether Johann Rupert winds it up or not it is now a highly defensive investment.

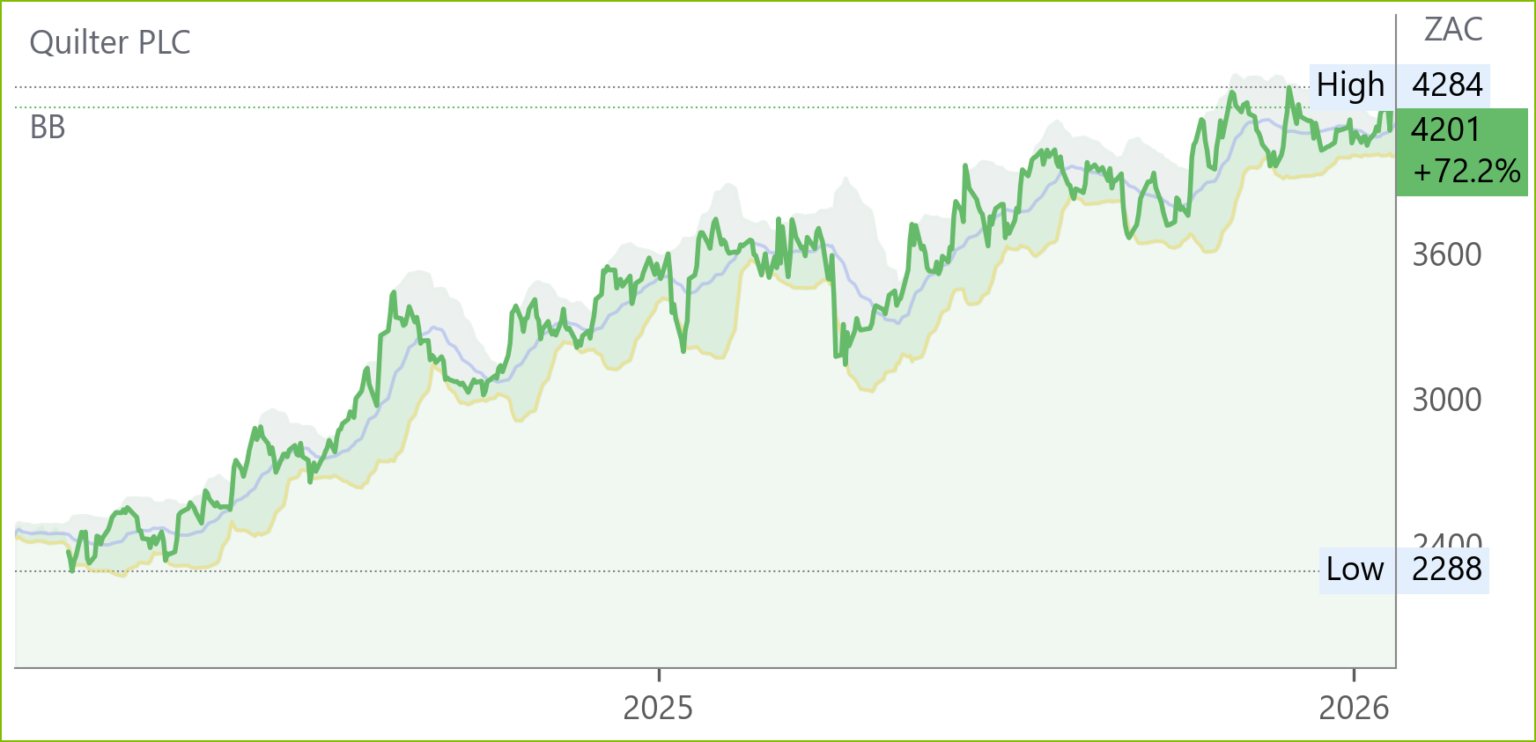

Quilter (QLT) Trading Statement Q4 FY25 (4201c)

Core net inflows surged 75% year‑on‑year to £9.1bn in FY25, with Q4 delivering a record £2.4bn despite UK Budget uncertainty. Assets under Management and Administration rose 18% to £141.2bn, supported by strong Platform flows which surpassed £100bn for the first time. Affluent segment inflows grew 92% in the IFA channel, while High Net Worth net inflows reached £686m. Persistency improved and adviser productivity rose 12%. “Our scale, distribution reach and compelling propositions make us uniquely positioned to meet customers’ needs and benefit from the secular growth opportunity in the UK Wealth market.” — Steven Levin, CEO. Results due 4 Mar ’26

Comment: with this kind of (secular) growth the stock is probably worth buying on a PE of 18.2x.

Merafe (MRF) Production Report FY25 (115c)

Ferrochrome output fell 63% in FY25 due to smelter suspensions under adverse market conditions. Chrome ore production declined 2% following temporary equipment breakdowns, while PGMs concentrate rose 5% on stronger feed tonnages. Management highlighted operational resilience despite market headwinds, noting that production diversification supported PGMs growth. Outlook remains cautious, with focus on stabilising smelter operations and leveraging ore and PGMs streams to offset ferrochrome weakness.

Eskom signed an MoU with Samancor Chrome and the Glencore‑Merafe JV to stabilise South Africa’s ferrochrome sector, hit by 900% tariff hikes since 2008. The agreement aims to suspend retrenchments, restore 40% smelter capacity, and create a long‑term competitive pricing framework. CEO Dan Marokane emphasised collaboration with government, labour, and industry to safeguard jobs and industrial capacity.