Finova Investor Digest

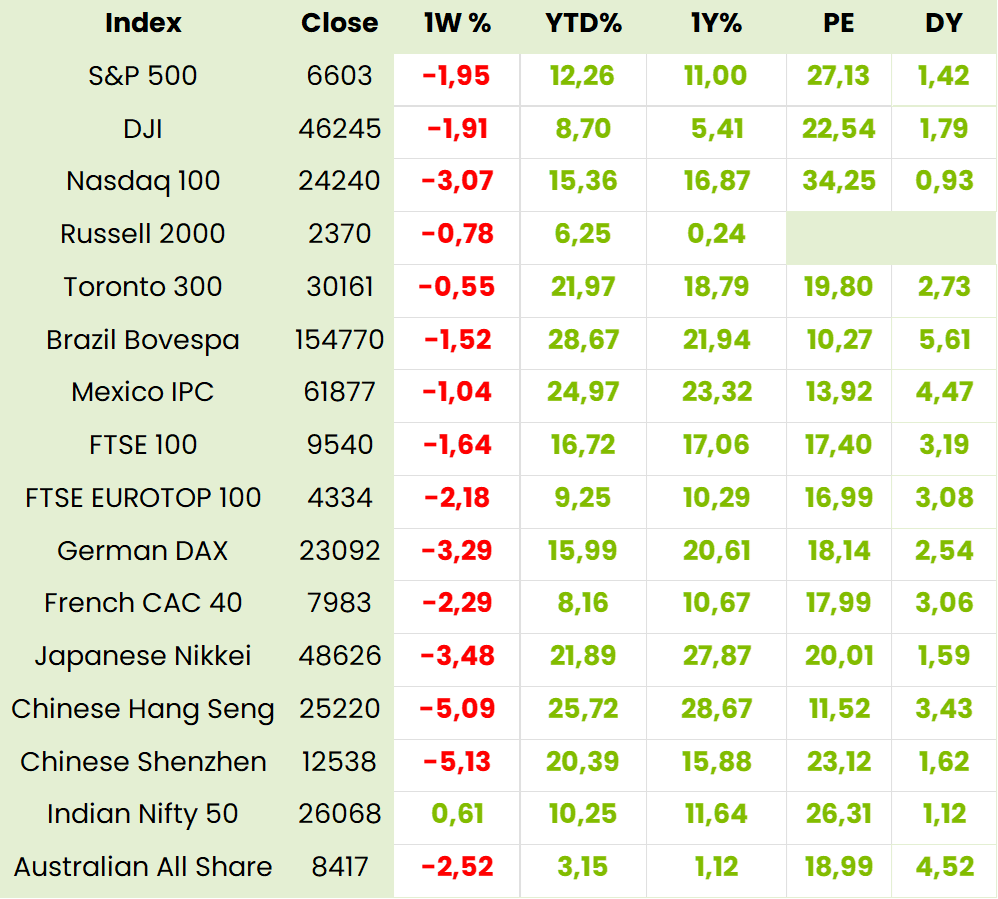

Global Indices, Currencies, Crypto & Commodities

Global Indices 1 year to Date

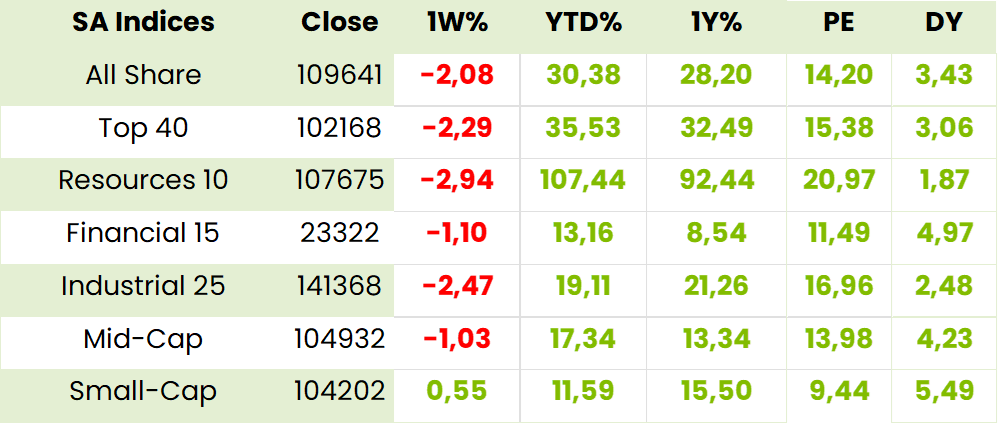

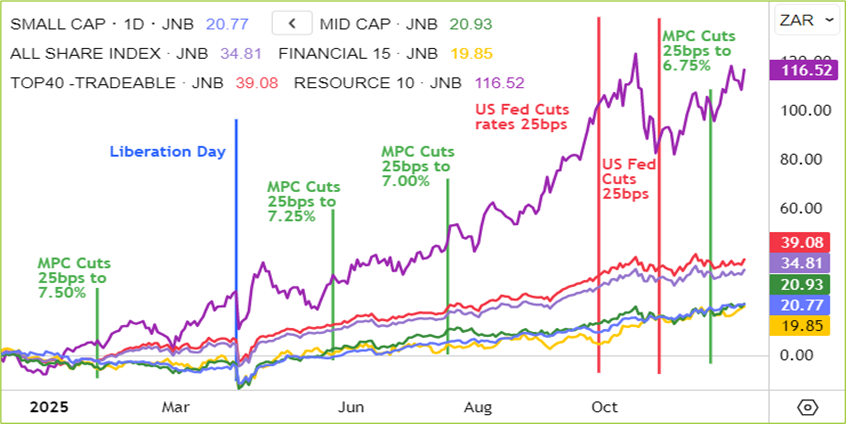

SA Indices

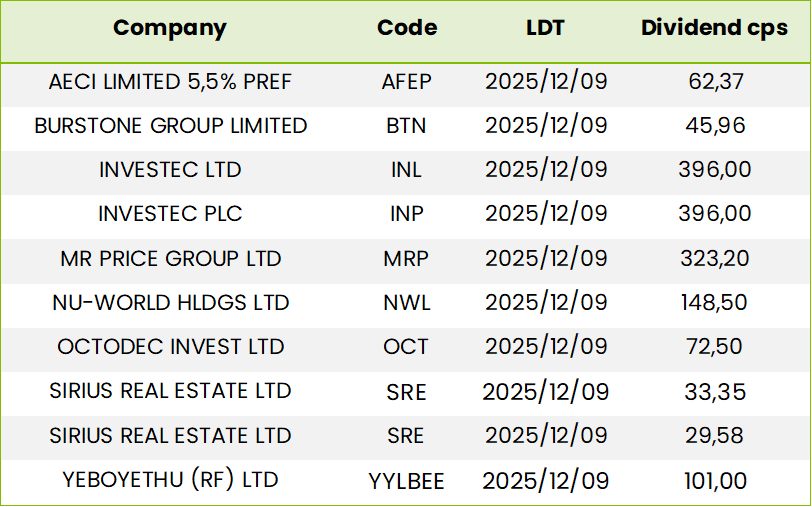

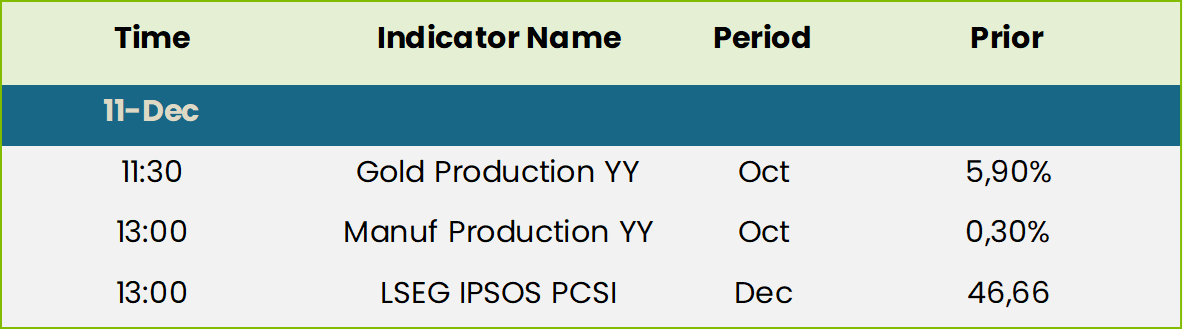

SA Upcoming Indicators & Dividends

SA Equity

Naspers (NPN) & Prosus (PRX) leadership transition at JET

On 11 November, not long after Prosus took control of Just Eat Takeaway (JET), its founder Jitse Groen stepped down as CEO and was replaced by Roberto Gondolfo who had joined Prosus in 2025 as Head of Prosus Europe. Prior to that he had spent more than a decade at iFood where he took monthly orders from 1 million to 120 million working with 400000 merchant partners and delivering to 60 million annual customers. Prosus CEO Fabricio Bloisi commented “We will move fast to transform JET through a focus on product, customer and innovation, creating a true European tech champion that will reshape the future of food delivery” Having himself founded iFood in Brazil, Bloisi would have seen exactly where Jitse Groen had got to with JET and why, with Gandolfo, he could take it so much further. This will be no mean task as JET is also in 16 European countries. Bloisi has, however, also repeatedly stressed the importance of AI which no doubt will also assist in addressing the nuances of different regions. The market has already adjusted for concerns as regards Prosus’ dependence on the Tencent share sales and dividend for its share buy back campaign and this is likely to have been the down leg of the J curve with the up leg to be driven by the rejuvenation of JET in Europe and other ecommerce businesses in the Latam and India regions. This confirms our view that the current retracement in Prosus and Naspers prices is a Buying opportunity.

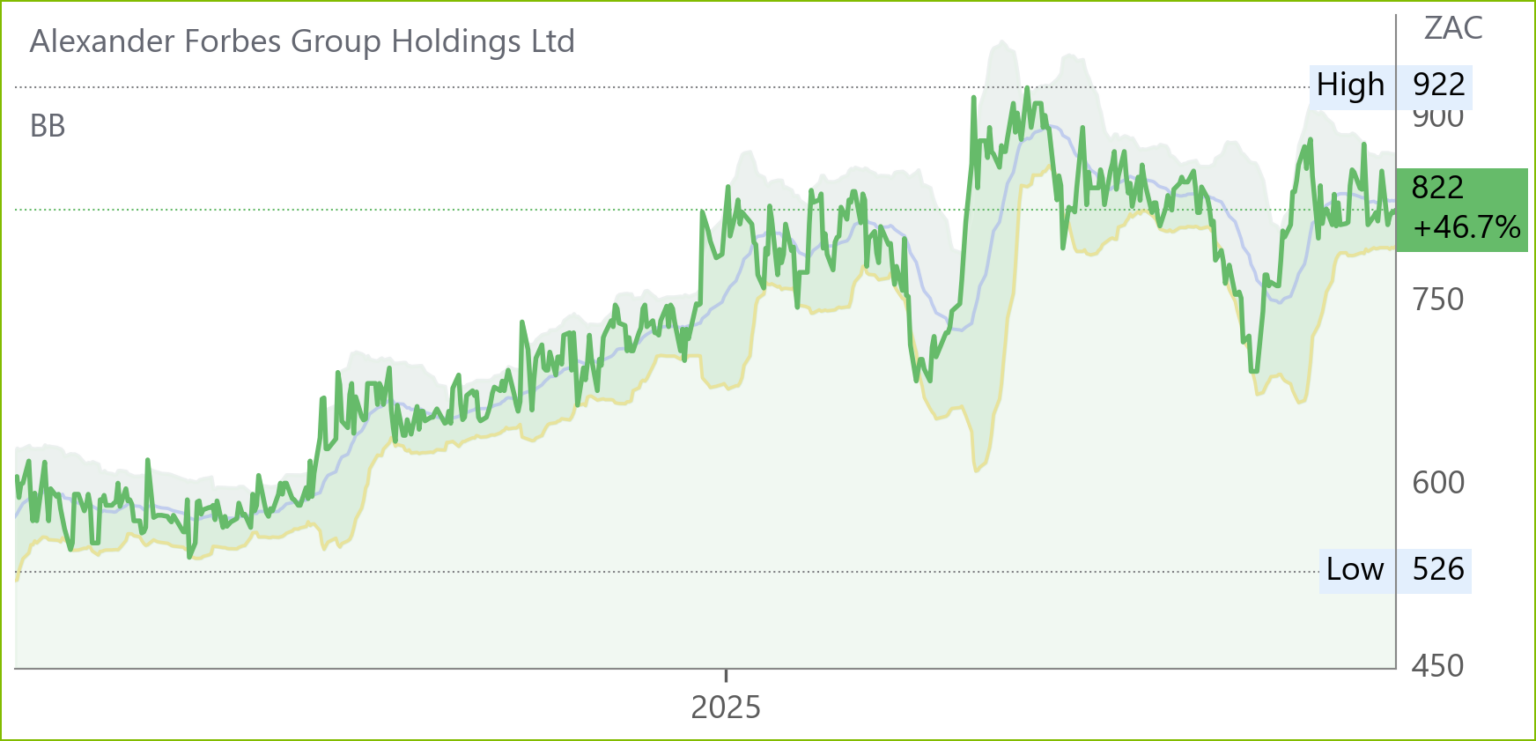

Alex Forbes (AFH) Interim Results for 6M Sep 25 (822c)

HEPS: 33.2c (↑17% from 28.4c)

EPS: 26.1c (↓9% from 28.7c)

Operating Profit: R443m (↓1% from R447m)

Revenue: R2 329m (↑9% from R2 140m)

EBITDA: R446m (↑18% from R377m)

Dividend: 24cps interim (↑9% from 22cps)

HEPS and EPS differ driven by discontinued operations settlement and IFRS 16 lease adjustment. Revenue and EBITDA growth reflect higher AUM, strong client retention, and new business flows.

Alexforbes delivered consistent performance, supported by robust investment flows and resilient client retention. Assets under administration rose 23% to R696bn, while active EPS members grew 12% to 1.2m. Liquidity remained strong with R466m cash and a capital cover ratio of 2.1x. Strategic initiatives included the launch of Alexforbes One, integrating retirement, healthcare, sustainability, and investments, and the acquisition of Paragon Impact to strengthen ESG advisory. Modernisation of fund administration platforms is underway across SA, Namibia, and Botswana. “We have focused on the implementation of our new operating model, which marks an inflection point in our journey.” – Dawie de Villiers, CEO.

Comment: Basic EPS for FY03/25 was 70.6c and 1H25 was 28.4c making for 2H EPS of 42.2c so, together with 1H26 EPS 33.2c the 12 month EPS is 75.4c making for a 10.8x PE.

Together with the FY03/25 final dividend of 33c the 12 month total of 57c makes for a 7% dividend yield which excludes the special dividend of 10cps at the time of the final. The strategic initiatives and modernisation of fund platforms do indeed, inter alia, lend credence to the CEO’s reference to a new inflection point. This make the stock attractively priced relative to its peers in the sector so it can safely be bought.

Nutun (NTU) Financial Results FY25 (122c)

HEPS: (113c) (↓33% from 170c)

EPS: (125c) (↓15% from 146c)

Operating Profit: R1 304m (↓5% from R1 378m)

Revenue: R2 953m (↓3% from R3 046m)

Gross Profit: Not disclosed

EBITDA: R1 304m (↓5% from R1 378m)

HEPS and EPS fell driven by once‑off restructuring costs, option liabilities, and impairments. Revenue and EBITDA declines reflect subdued consumer payment behaviour, portfolio amortisation, and recalibration of Nutun International’s client base.

Nutun completed a two‑year restructure, streamlining into Nutun South Africa (collections and recovery) and Nutun International (BPO services). South Africa faced weaker consumer payments and reduced portfolio acquisitions, while International grew billable seats by 7% and diversified clients. Liquidity improved with refinanced facilities and disposals, leaving R1bn unutilised. Technology investments in AI and automation are expected to enhance efficiency. “Nutun has entered a new phase focused on profitability and growth with FY26 starting from a solid base.” – Jonathan Jawno, CEO.

Comment: Since the announcement the market has taken CEO Jawno at his word with the share price picking up from 98c to 121c which if FY09/26 Heps of, say, 10c is achieved, implies PAT of R94m. It would also imply a turnaround from a loss from continuing operations in FY25 of 14.4c and 18.7c in FY24. Our guess is that the UK, USA and Australia based business process outsourcing teams will do somewhat better than the SA debt collections business, but both will improve. Jawno, when he used the words “has entered” the new phase of profitability was telling us they are already profitable. Again, taking him at his “growth” word, a shortfall on the 10cps heps level would be more than made up in FY27. On this basis, the share is a, somewhat speculative, BUY.

Zeda (ZZD) Financial Results FY25 (1380c)

HEPS: 361c (+15.7% from 312c FY24)

EPS: 360c (+12.5% from 320c FY24)

Operating Profit: R1.62bn (+10.8% from R1.47bn FY24)

Revenue: R10.65bn (+1.7% from R10.47bn FY24)

Gross Profit: R4.35bn (+3.9% from R4.19bn FY24)

EBITDA: R3.36bn (+0.4% from R3.35bn FY24)

Dividend: 181cps (final dividend 126cps)

HEPS and EPS rose double‑digits, supported by leasing growth (+15.7%) and improved fleet utilisation. Operating profit expanded 10.8% as expenses were contained below inflation, while revenue growth was modest at 1.7%. Net debt increased to R5.18bn, with net debt/EBITDA at 1.5x, reflecting fleet expansion. Strategic focus on subscription and Greater Africa operations under extended Avis Budget licences strengthened regional positioning.

Outlook highlights expansion into East, West and Central Africa, supported by strong balance sheet capacity and IT/data strategies to drive customer‑centric innovation. “Our disciplined execution and diversified model underpin sustainable growth and strong shareholder returns. We are well positioned to capitalise on transformative opportunities across Africa.” – Ramasela Ganda, CEO.

We struggle to find out why this stock is so cheap apart from only being listed for 3 years. On a PE of 3.1x and 16% DY it has to be a BUY in anybody’s language. Just btw it is Avis’s biggest partner/licensee outside the US and both entities have their eyes very much on African opportunities. Also, it is cum the final 126c until 3 February 2026.

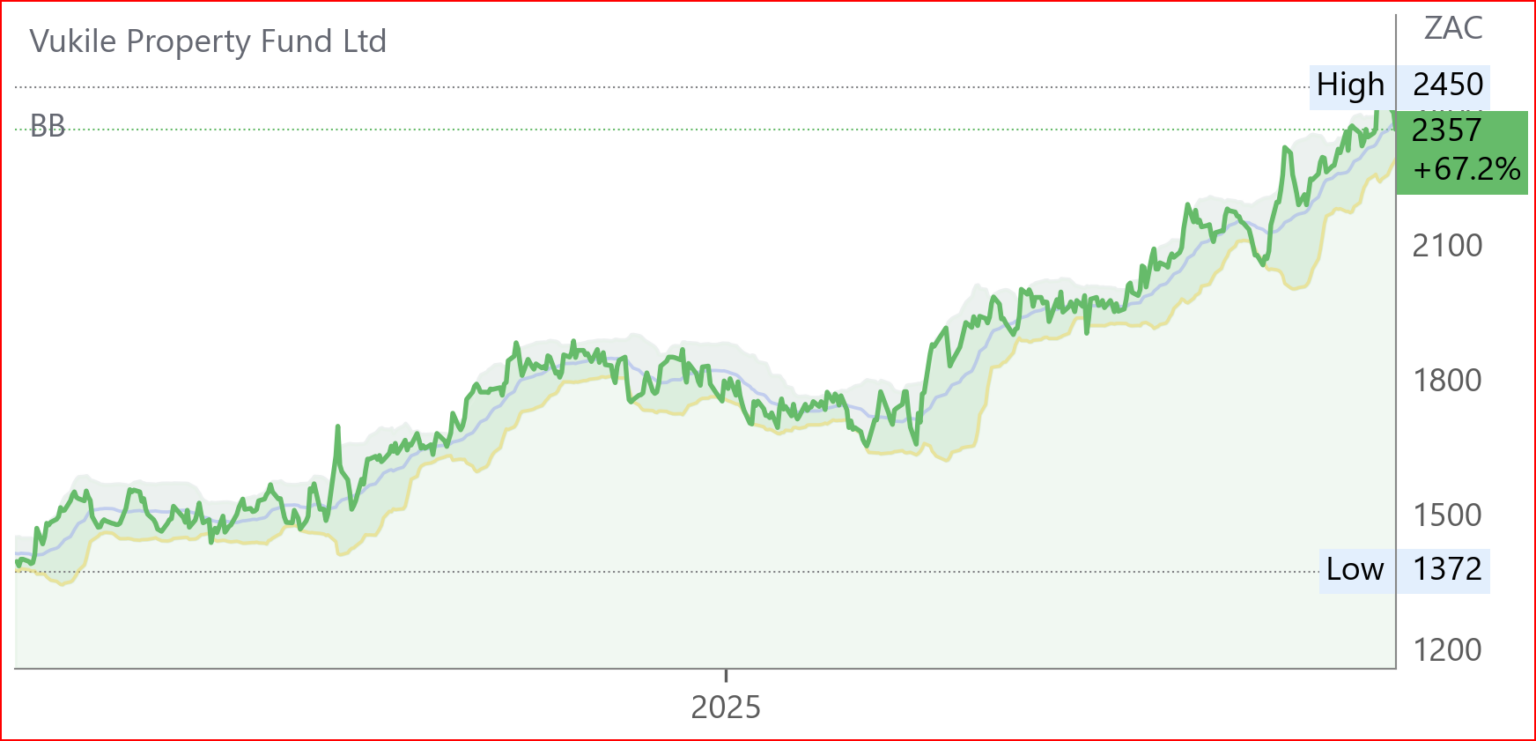

Vukile (VKE) Interim Results for 6M Sep 25 (2357c)

HEPS: 85.2c (↓2.5% from 87.4c)

EPS: 190.c (↑73% from 109.8c)

Operating Profit: R1.67bn (↓5.6% from R1.77bn)

Revenue: R2.90bn (↑36.9% from R2.12bn)

Dividend: 60.2cps interim (↑9% from 55.2cps)

LTV: 41.6% (flat vs prior period)

EPS rose sharply (+73%) due to Iberian acquisitions and FX gains, while HEPS was flat, reflecting normalised earnings. Revenue surged (+36.9%) from new assets, but operating profit dipped slightly on prior one-off income.

Operational excellence was evident in South Africa with NOI growth of 10% and stable vacancies at 1.8%. Iberian acquisitions contributed meaningfully, with portfolio vacancy at 1.3% and WALE of 8.9 years. Efficiency gains from solar PV reduced the cost-to-income ratio to 12.5%. Liquidity was bolstered by a R2.65bn oversubscribed equity raise, while credit ratings were upgraded. Guidance for FY26 was lifted to ≥9% growth in both FFO and dividends. “Momentum has continued and is reflected in very strong trading metrics across our key markets… positioning us well for sustained growth in the years ahead.” – LG Rapp, CEO.

Comment: At the outset of his presentation CEO Rapp emphasized the very strong operating performance, successful integration of acquisitions, and number of transactions being worked on, for which funds were fully available, as key factors for investors to note. While he was particularly optimistic with Spain and Portugal as being the “growth engine of Europe” with current and expected GDP growth around 2 to 2.5% for 2025-2026 he said the SA portfolio was in a sweet spot with its rural malls operating successfully in 8 of the 9 provinces. Culturally appropriate promotional activities and focus on tenants in non-discretionary spending areas were features of the SA businesses. The forecast 173.1cps FFO and 143.6c DPS put the stock on a 6 month FPE of 13.9x and FDY of 6% which means Vukile is one of the most highly rated JSE REITS. Given its proven ability to mobilise and successful deploy meaningful sums of capital, investors can safely stay with, or, BUY, the stock. In addition to the deals currently expected to be finalised late in FY26 or early FY27, the company is exploring opportunities beyond SA and Iberia.

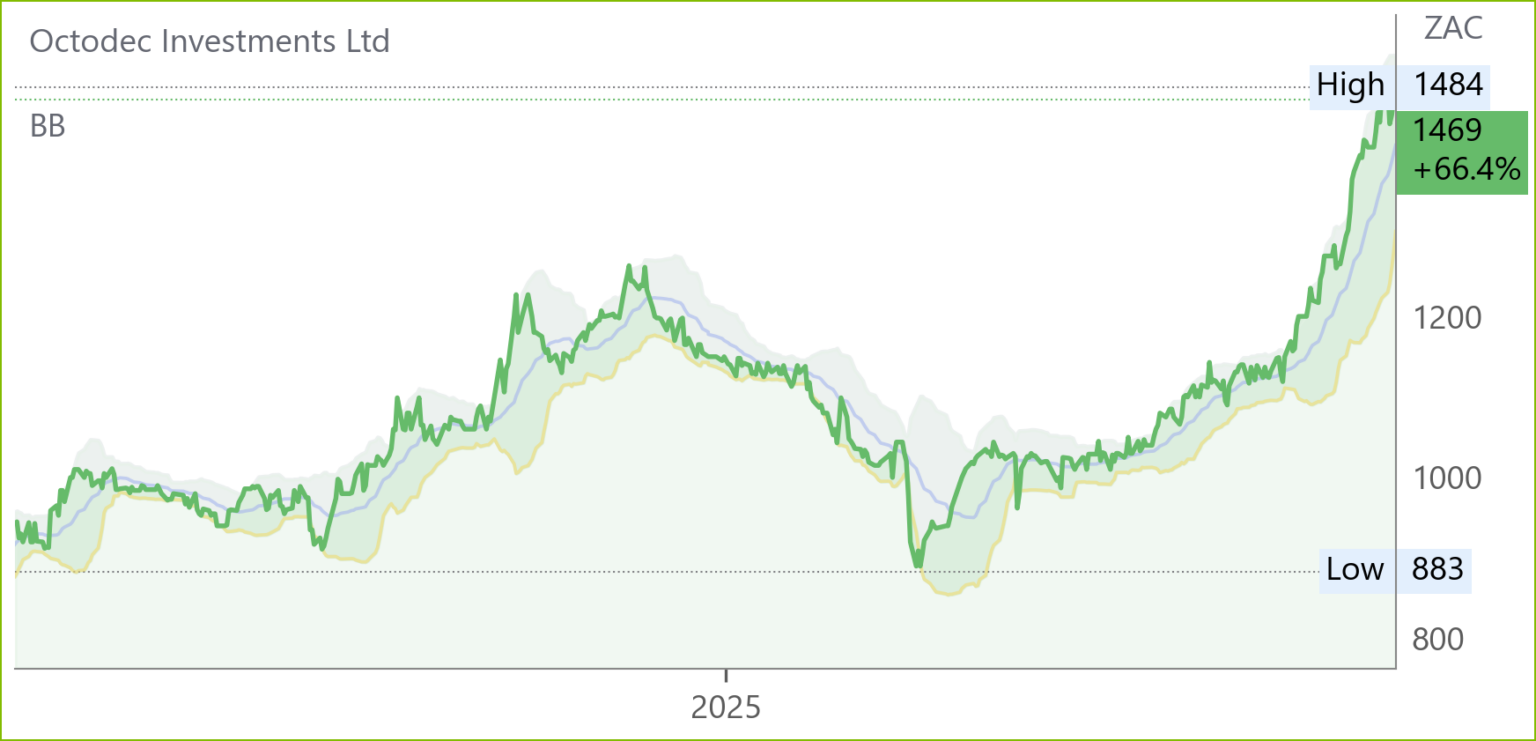

Octodec (OCT) Financial Results FY25 (1469c)

HEPS: 163.4c (+15.2% from 141.9c FY24)

EPS: 184.5c (+127.5% from 81.1c FY24)

Revenue: R2.17bn (+4.6% from R2.08bn FY24)

Dividend: 134.5cps (dividend of 72.50cps for the 6M ended 31 Aug ‘25)

Octodec’s FY25 EPS was boosted by non‑recurring items excluded from HEPS. Gains stemmed from property revaluations, disposals of non‑core assets, and fair value adjustments on financial instruments. These once‑off effects inflated EPS by over 120%, while HEPS rose only 15%, reflecting core rental income growth and reduced vacancies. EPS therefore captures exceptional gains, not sustainable trading performance.

Revenue growth was modest, supported by reduced vacancies and stable rental escalations. Settlement of large tenant exits created short-term challenges, but management is optimistic about rationalising the portfolio and converting Capitol Towers North into affordable residential units. “We are cautiously optimistic about opportunities created by lower interest rates and remain focused on delivering sustainable returns.” – Jeffrey Wapnick, CEO.

Comment: Wapnick infers the CBDs are by no means to be written

off and certain nodes are doing particularly well. If, as seems likely, the Killarney Mall sale goes through, the conversion of Capitol Towers, previously occupied by the City of Tshwane, will be one such opportunity for profitable redeployment of capital. While this will take time to boost heps growth, Octodec will remain a steady performer and one of the higher yielding stocks in the sector. So, HOLD.

Accelerate (APF) Interim Results for 6M Sep 25 (54c)

HEPS 5,01c (from –5,67c)

EPS 2,59c (from –14,11c)

Revenue R452,2m (+15,1% from R392,7m)

LTV 47,1% (+0,4pp from 46,7%)

HEPS recovered strongly from a loss, while EPS also turned positive reflects insurance settlement gains and debt write-offs. Asset disposals, a R100m rights issue, and debt reduction improved balance sheet resilience. Fourways Mall vacancies fell to 10,7% with Walmart opening in Nov ’25, boosting footfall. Insurance settlement of R82,5m supported revenue, while disposals of Eden Meander and Cherry Lane reduced retail rental income. Finance costs dropped by R28,4m due to debt settlement and new swaps hedged 68,1% of borrowings. Outlook: “Accelerate is focused on stabilising its portfolio and enhancing shareholder value through disciplined capital management and improved operational performance.” – Directors

Comment: Despite the successful opening of Walmart and 69% discount to NAV it is too early to consider this min-market cap (c. R800m) stock with outstanding debt of R3.7bn.

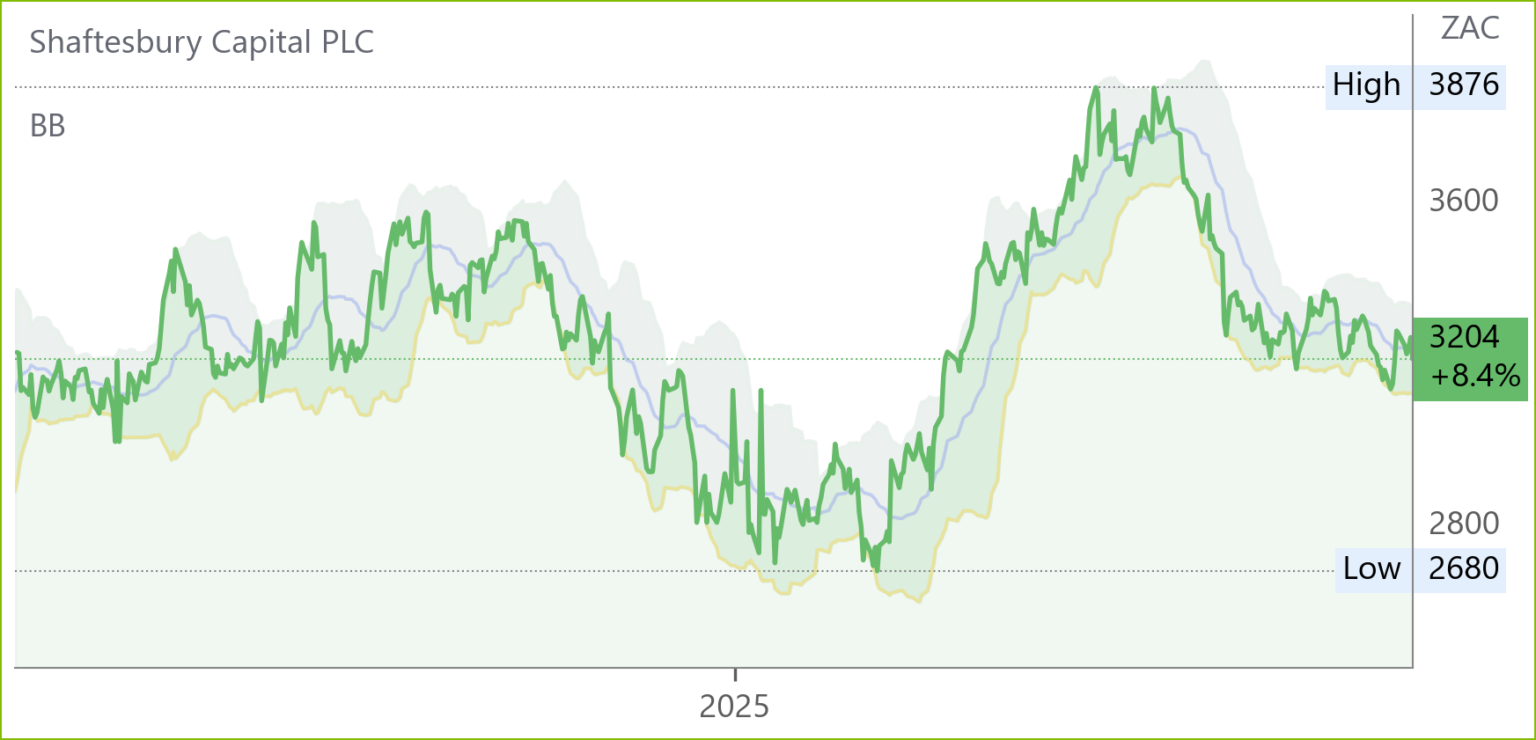

Shaftesbury Capital (SHC) Trading Update for 4M Oct 25 (3204c)

LTV: 17% (pro forma, based on Jun ’25 valuations)

367 leasing transactions year‑to‑date added £30,2m contracted rent, 9% ahead of Dec ’24 ERV. Occupancy remains high with only 2,6% ERV available to let. Covent Garden, Carnaby, Soho and Chinatown saw strong footfall and new openings, including Charlotte Tilbury, Harry’s Bar and Sushinoya. £80m invested in prime acquisitions, while a £300m revolving credit facility was secured and a £200m term loan repaid early. Liquidity exceeds £975m. Outlook: “Our exceptional West End portfolio is well positioned for the Christmas trading period and beyond.” – Ian Hawksworth, CEO

Copper 360 (CPR) Interim Results for 6M Aug 25 (74c)

HEPS: –18.74c (↓54.1% from –12.16c)

EPS: –18.74c (↓54.1% from –12.16c)

Operating Profit: Loss before interest & tax –R120.5m (↓31.3% from –R91.8m)

Revenue: R67.9m (↓3.2% from R70.1m)

EBITDA: –R111.5m (↓24% from –R90.2m)

Revenue fell 3% despite concentrate sales rising 163%, as cathode operations remain suspended. Losses widened due to higher mining costs and transitional ore feed, which reduced recoveries.

Copper concentrate output rose 107% to 466.9t, driven by higher feed volumes and improved grades. Recoveries improved to 61.4% but remain constrained by transitional ore. A concurrent claw‑back offer, rights issue and debt restructuring aims to raise R1.15bn, strengthening the balance sheet and funding expansion. “Copper 360’s multi‑mine strategy positions us to diversify ore sources and deliver sustainable shareholder value.” – Copper 360 Board.

Comment: with R825m borrowings at 3.05x the Equity of R271m the R1.15bn financing exercise may well get the company to first base but more will be needed. The auditors have provided a “Practitioners Compilation Report” on the interims as the accuracy and completeness of the information used remained the responsibility of the Directors. No need to bottom fish here yet.

Tharisa (THA) Financial Results FY25 (2025c)

– HEPS: US 27.5c (↓2.1% from US 28.1c)

– EPS: US 26.7c (↓3.6% from US 27.7c)

– Operating Profit: US$125.6m (↑5.0% from US$119.6m)

– Revenue: US$602.9m (↓16.4% from US$721.4m)

– EBITDA: US$187.3m (↑5.5% from US$177.6m)

– Dividend: US 3.0cps (↓33.3% from US 4.5cps)

Revenue fell sharply due to lower chrome and PGM volumes, but EBITDA and operating profit rose modestly on cost discipline and royalty credits.

Tharisa advanced its integrated resource model, spanning mining, beneficiation, and logistics, while reinforcing growth through the Karo Platinum Project in Zimbabwe. Chrome and PGM output declined, but reef mined rose 17%. The group is targeting a 30% carbon reduction by 2030 and net neutrality by 2050, supported by Redox One’s proprietary battery technology. Liquidity remains strong with dividend maintained, albeit reduced.

Comment: First ore from Tharisa’s Apollo $363m underground project in SA is expected in 2Q26 with steady state expected in 3QFY29. It will be followed by project Orion with first ore in 4Q31 and steady state in 3Q33. Apollo’s expected capex is $363m and Orion $173m and the projects are designed, in view of the ongoing depletion of open resources, to maintain production at 5.6mtpa. Waste stripping at the Karo project in Zimbabwe will commence in late 1Q26 with Tharisa’s capex of $178m to date to be followed by debt finance from various sources of $240m. With projected AISC of $850/oz and pgm spot prices @ $2024/oz profitability looks assured. While anticipating rather than following the money would be a good idea we recommend waiting until closer to the capex harvest times before buying at these levels.

Netcare (NTC) Financial Results FY09/25 (1523c)

HEPS: 137.2c (↑20.7% from 113.7c)

EPS: 135.3c (↑22.6% from 110.4c)

Operating Profit: R3.58bn (↑13.2% from R3.16bn)

Revenue: R26.34bn (↑4.5% from R25.20bn)

EBITDA: R4.93bn (↑9.7% from R4.49bn)

Dividend: 85.0c per share (final dividend 49.0c, interim dividend 36.0c)

Growth in HEPS and EPS was driven by improved operational efficiency, higher patient volumes, and disciplined cost management, supported by stable demand for healthcare services.

Operational performance was supported by enhanced clinical governance and investment in digital health platforms. Patient volumes increased across acute hospitals, with strong demand for specialised care. Netcare maintained a focus on safety, achieving high standards in infection control and clinical outcomes. Cash generation remained robust, enabling debt reduction and dividend growth.

“Netcare is advancing its transformation journey, and we remain committed to delivering safe, quality care while creating long-term shareholder value.” – Richard Friedland, CEO.

Comment: this was a steady set of results in line with expectations and investors can take note of CEO Friedland’s commitment to long-term shareholder value and the upper end of revenue growth guidance for FY26 at 4.2%. On a 10.9PE and 5.7% FY the stock is correctly priced and will benefit from its planned expansion, somewhat improved economy and the ongoing ageing of a substantial portion of its target market.

Life Healthcare (LHC) Financial Results for FY09/25 (1120c)

HEPS: 88.9c (↓20% from 112.1c)

EPS: 263.0c (↓20% from 328.8c)

Operating Profit: R4.6bn cash generated (↑119.6% of normalised EBITDA)

Revenue: R25.1bn (↑6% from R23.7bn)

EBITDA: Normalised EBITDA implied at c. R3.8bn (↑c.10%)

Dividend: 35.0cps final (↑12.9% from 31.0cps), plus special dividend of 235cps paid Sep ‘25

HEPS and EPS diverged >30% due to disposal of Life Molecular Imaging (LMI) and related accounting adjustments. EPS reflects discontinued operations, while Normalised earnings per share (NEPS) increased by 10.1% to 100.3 cents and better captures underlying growth.

Activity growth in paid patient days lifted occupancy to 69.7%, with c.72% excluding remediated assets. Disposal of LMI generated USD355m upfront and contingent proceeds through 2034, funding a R3.4bn special dividend. Net debt/EBITDA fell to 0.01x, highlighting strong liquidity. “Life Healthcare continues to grow its asset base in strategic locations, adding capacity and expanding diagnostics to deliver sustainable shareholder value.” – PG Wharton-Hood, CEO.

Comment: Normalised EPS from continuing operations was 10.1% up at 100.3 from 91.1c making for a 11.3x PE and 4.9% DY with the stock cum the final 35c until 15 December. In addition to the complex LMI transaction, LHC sold two smaller hospitals as part of its asset optimisation with expansion in “growth geographies” such as Paarl. This includes, in addition to hiring net 98 specialists, a 9 year R450m programme to train, 40 surgical specialists, 35 medical specialists and 40 sub specialists-with an expected return of 22% (current ROCE 17.8%). CEO Peter Wharton-Hood points to 5% revenue growth and, to achieve bottom line growth, cost savings of R400m planned over the next 3 years. At this stage we recommend “seeing is believing” and to wait until, at least the interims, for signs of progress in this regard.

Reunert (RLO) Financial Results for FY25 (6235c)

HEPS: 649c (-5% from 685c)

EPS: 654c (-5% from 690c)

Operating Profit: R1.52bn (-8% from R1.64bn)

Revenue: R13.88bn (-2% from R14.23bn)

Dividend: 293c final dividend (+6% YoY)

Reunert reported softer FY25 results with HEPS down 5% and operating profit 8% lower, reflecting weak Electrical Engineering volumes, tariffs on US exports and FX losses in Zambia. Defence delivered record radar and fuze performances, ICT restructured to align costs, and renewable energy assets expanded 22% to 95MW. Nashua remained stable despite reduced loadshedding-related sales, while cash generation of R1.17bn supported a higher dividend. Management anticipates steady improvement in 2026, driven by infrastructure investment, offshore defence growth and ICT recovery. “Positive financial performance and strong cash flows have generated meaningful momentum,” said Chairman Mohamed Husain.

Comment: post results price action has adjusted appropriately to a 9.6x PE and 6.1% DY for the “steady improvement” management expects for FY 26. While defence related businesses continue to forge ahead the power cable business awaits the accelerated Transmission Development Plan (TDP) rollout which, however, appears fairly imminent. This is an SAInc stock with a growing export business which will also benefit when infrastructure spending picks up. It will also be interesting to see whether it benefits from fresh insights from the new CEO. Timing wise, investors could await signs of an infrastructure before buying.

Invicta (IVT) Interim Results for 6M Sep 25 (3607c)

HEPS: 265c (↑15% from 231c)

EPS: 268c (↑7% from 251c)

Operating Profit: R243m (↓11% from R274m)

Revenue: R4.24bn (↑6% from R4.00bn)

Dividend: none declared (board intends year-end dividend with 2.75–3.25x cover on sustainable earnings)

HEPS rose 15% while EPS increased 7%, supported by sustainable earnings growth despite once‑off costs. Invicta acquired UK‑based Spaldings in Sep ’25, strengthening its agricultural and ground care distribution footprint. Cash reserves of R901m and a 17% NAV uplift underscored balance sheet resilience. Operations remained reliable, with efficiency gains and strategic discipline driving performance. Management anticipates continued growth through acquisitions and operational optimisation. CEO Steven Joffe stated: “Our core operations remain strong and reliable, and we are positioning Invicta for sustainable growth while maintaining disciplined capital allocation.” – Steven Joffe, CEO. Dividend declaration expected at FY25 year‑end.

Frontier Transport (FTH) Interim Results for 6M Sep 25 (620c)

HEPS: 50.77c (↓13.7% from 58.81c)

EPS: 51.50c (↓14.2% from 60.01c)

Revenue: R1.39bn (↓5.7% from R1.48bn)

Dividend: 27.7cps interim (↑6.9% from 25.9cps)

HEPS and EPS declined c.14%, reflecting softer trading conditions and higher costs. Revenue fell 5.7% y/y, but dividend payout increased 6.9%, signalling confidence in cash generation.

Net asset value rose 12.3% to R1.67bn, strengthening the balance sheet. Fleet optimisation and operational efficiencies supported resilience despite revenue pressure. Management emphasised continued investment in transport infrastructure and service reliability.

Operating Updates & Trading Statements

Nedbank (NED) Pre-Close Investor Update FY25 (25895c)

HEPS: Flat to low single-digit growth (FY24 base: 3 106c)

EPS: Flat to low single-digit growth (FY24 base: 3 120c)

Operating Profit: Growth in line with expectations

Revenue: NII +3–5% (vs +2% in H1 ’25); NIR +2–4%

Net interest income rose 3–5% y/y, supported by household credit demand and mid-to-upper single-digit advances in Personal and Private Banking. Corporate advances grew above mid-single digits, though drawdowns shifted into 2026. Deposits outpaced loans, sustaining liquidity. Credit loss ratio improved to below midpoint of 60–100 bps target range. Expenses grew 6–9%, moderated by staff and IT costs, excluding a once-off R600m Transnet settlement. The CET1 ratio remained >12%, with R2.4bn share buybacks (10.54m shares at R229.53 average). “We are on track to deliver ROE of 15% or higher for FY25.” – Mike Davis, CFO. Results due 3 Mar ’26

Standard Bank (SBK) Trading Update for 10M Oct 25 (27737c)

Revenue: Mid‑to‑high single‑digit growth (vs 10M Oct ’24)

Net interest income: Growth supported by book expansion and strong origination in Investment Banking; offset by lower average interest rates.

Non‑interest revenue: Robust, with strong net fee and commission growth from larger client base and activity.

Trading revenue: Momentum remained strong, supported by uncertainty and volatility.

Costs: Activity‑related costs increased, but overall cost growth contained and below revenue growth.

Credit loss ratio: ~70–100bps (mid‑range of through‑the‑cycle guidance).

Corporate & Investment Banking: Higher off a low base.

Personal & Private Banking: Lower due to slowdown in arrears formation and fewer inflows into NPLs.

Business & Commercial Banking: Lower, driven by improvements in SA and Africa Regions.

Insurance & Asset Management: Higher earnings YoY, supported by improved persistency and claims ratios; absence of catastrophic weather events aided short‑term insurance.

Outlook: Guidance unchanged — banking revenue growth mid‑to‑high single digits, cost‑to‑income ratio flat to lower, ROE anchored at 17–20%. (HEPS growth 8–12%, ROE 18–22%). Results due 12 Mar ’26.

FirstRand (FSR) Trading Update for 6M Dec 25 (8674c)

Interest rates: Two 25bps cuts in Jul and Nov ’25 supported household affordability.

Advances growth: Large corporate lending margins improved under originate‑and‑distribute; commercial advances grew across SME portfolios. Retail lending volumes picked up, expected to exceed FY24 levels.

Deposits: All franchises growing at similar levels to FY24.

NIR: Trending higher than FY24, driven by insurance momentum, global markets rebound, and private equity realisations.

Credit: CLR remains at bottom of through‑the‑cycle range; retail credit improving, commercial within range, large corporates resilient.

Costs: Guided 2–3% above inflation, anchored to 5% salary inflation negotiated in Jun ’25.

Outlook: Full‑year earnings growth expected in high mid‑teens, above long‑term target range; ROE guided towards upper end of 18–22%. “The group expects to deliver full‑year earnings growth in the high mid‑teens, above its long‑term target range, with ROE trending towards the upper end of 18–22%.” – Management. Results due Mar ’26.

Exxaro (EXX) Pre-Close Update FY25 (17150c)

Operating Profit: Stable, supported by optimisation efforts

Revenue: Coal export price US$89/t (FY24: US$105/t); iron ore US$100/dmt (FY24: US$109/dmt)

Share repurchase of 7.39m shares (2.12% of issued capital) completed Oct ’25

Exxaro reported coal product volumes of ~39.5Mt for FY25, in line with FY24, with export sales steady at ~7Mt. Domestic thermal sales rose 30% to 22.6Mt, offsetting weaker international demand. Metallurgical coal sales fell 49% to 351kt due to softer steel sector activity. Cennergi generated 695GWh electricity, down 4% y/y, with plant availability exceeding 97%. Capital expenditure increased 7% to R2.23bn, driven by Grootegeluk’s Truck and Shovel strategy and Belfast’s Double Benching. Net cash stood at R18bn at Oct ’25, excluding energy debt. Social investment reached R1.28bn, supporting 362 black-owned MSMEs with R926.9m procurement spend. FerroAlloys disposal yielded R250m, while manganese acquisitions advanced with ministerial and competition approvals.

“Our focus on operational excellence and resilience ensures sustained delivery in a constrained environment.” – Riaan Koppeschaar, FD. Results due 19 Mar ’26

Glencore (GLN) Markets Day update (8649c)

Glencore outlined cost savings across headcount, energy, consumables, contractors, maintenance and administration, with over 50% locked in for 2025 and full delivery by 2026. Around 1,000 roles were eliminated under its devolved operating structure. Copper production guidance for 2026 was lowered to 840kt, rising from 2027, while zinc volumes step down to ~720ktpa over 2026–2029. Energy and steelmaking coal volumes are expected to remain steady. Alumbrera mine (copper and gold) restart capex is estimated at $0.23bn. Industrial capex will average $6.5bn annually between 2026 and 2028, excluding copper growth projects, reflecting disciplined capital allocation and operational efficiency. Glencore has mining and industrial operations across more than 35 countries worldwide, with a strong footprint in Africa, the Americas, Europe, Asia, and Australia.

Hyprop (HYP) Pre-Close Operational Update for 4M Oct 25 (5650c)

Revenue: SA tenants’ turnover ↑5.3% (vs 4M Oct 24); EE tenants’ turnover ↑2.9%

LTV: 34.3% (↑0.7pp from 33.6% Jun 25)

Strong turnover growth in SA and EE portfolios highlights resilience despite consumer headwinds. Solid trading metrics across its SA and EE portfolios, with SA turnover up 5.3% and trading density up 8.5%. Foot count rose 1.9% and vacancies improved to 3.2%. EE centres maintained 0% vacancy and steady growth. Capital projects included Canal Walk’s Otter Bridge, Somerset Mall’s expansion, and Clearwater Mall’s Walmart opening. ESG initiatives advanced with solar PV approvals, battery storage planning, and net-zero waste certification at five centres. Liquidity remains robust with R873m cash and R2.3bn facilities. “Hyprop offers investors a compelling opportunity, backed by resilient portfolios and distributable income growth of 10–12% guided for FY26.” – Morné Wilken, CEO. Results due 10 Mar ’26.

Equites (EQU) Trading Update FY25 (1780c)

– Dividend: 140–143cps guided for FY25

Operational pipeline highlights indicate strong development activity.

Equites secured a 10‑year lease with Tiger Brands for a 90,000m² Gauteng facility at a net yield of 9% on R1bn cost. It also won a tender for a 24,000m² logistics facility and expanded Premier FMCG’s Lords View site to 32,000m². Negotiations are underway for ~150,000m² of new developments worth R2bn. UK exit strategy remains, with disposals subject to value maximisation. Newport Pagnell completion is imminent, while Coton Park is on track for Sep ’26. “Our foremost commitment is to maximise shareholder value, with timing of UK disposals aligned to this objective.” – Management statement.

Snippets

Remgro (REM) Remgro and MSC agreed to restructure Mediclinic, granting Remgro full control of Southern African operations and MSC oversight of Switzerland’s Hirslanden, while retaining joint Middle East and Spire interests. The move sharpens local focus, enhances agility, and supports sustainable growth. Mediclinic’s interim results showed strong performance with 10% revenue growth and 23% EBITDA growth.

Sappi (SAP) and UPM signed a non‑binding LOI to merge their European graphic paper businesses into a 50/50 joint venture, expected to close by end‑2026. The deal, valued at €1.42bn, will unlock €100m annual synergies, reduce Sappi’s exposure to declining paper markets, strengthen cash flow, and provide €139m proceeds for debt reduction, pending shareholder and regulatory approvals.

Aveng (AEG) will retain McConnell Dowell after reviewing separation options, focusing on profitability and securing A$1.2bn new work with another A$1.2bn pending. Sale negotiations for Moolmans continue, with Pieter van Greunen appointed MD. About 1,000 roles were cut under the new structure. Half‑year results to Dec ’25 will be released 24 Feb ’26.

Labat Africa (LAB) Labat Africa will dispose of its entire CannAfrica stake to Africa Ntsha Trading Solution for R8m, completing its exit from cannabis and healthcare. The deal eliminates losses of R16.6m, strengthens working capital, and funds ICT, microelectronics, logistics, and AI strategy.

Jubilee Metals (JBL) signed a co‑operation and development agreement with Galileo Resources to accelerate exploration and development of the Molefe Mine in Zambia. Jubilee retains 71.25% ownership, Galileo can earn up to 23.75% through US$700k funding, and 5% is held locally. Production is ramping to 4 500tpm, with on‑site processing planned.

Sibanye‑Stillwater (SSW) concluded a three‑year wage agreement with AMCU, NUM, UASA and Solidarity at its SA gold operations. Effective 1 Jul ’25 to 30 Jun ’28, the deal provides average annual increases of 5,4%. Category 4–8 employees gain R850–R1 000 or 4,5–5,0% yearly, while miners, artisans and officials receive 4,5–5,0% increases, ensuring stability and sustainability.

Thungela (TGA) agreed to sell its Goedehoop North mining assets to GHN Resources and Bisichi for up to R700m. The deal includes a coal terminal, beneficiation plant, mining rights, and rehabilitation liabilities. A R15m deposit is secured, with deferred payments linked to infrastructure use. Operations at Goedehoop end in 2025, strengthening Thungela’s balance sheet and portfolio optimisation.

Merafe (MRF) issued conditional retrenchment notices and voluntary severance approvals effective 1 Dec ’25, following Eskom’s tariff proposal that only supports the Lion smelter. Without government intervention by 8 Dec ’25, retrenchments become binding and Boshoek and Wonderkop smelters will enter care and maintenance from 1 Jan ’26. Engagement with stakeholders continues to seek operational sustainability.

Spear REIT (SEA) finalised the R437,3m acquisition of Consani Industrial Park in Elsie’s River on 2 Dec ’25. The transfer lifted portfolio value to R6,8bn and market capitalisation to R4,9bn, with GLA expanding to 625 019m². Loan‑to‑value ratio stands at 26–27%, reinforcing balance sheet strength and Western Cape‑only asset strategy.

Raubex (RBX) announced it is evaluating the possible disposal of all or part of its stake in Bauba Resources. A transaction advisor has been appointed, but discussions remain preliminary with no certainty of outcome.

Vodacom (VOD) will acquire a further 20% stake in Safaricom, comprising 15% from the Kenyan government and 5% from Vodafone, for US$2.1bn (R36bn). This raises its holding to 55%. The deal consolidates Safaricom, strengthens fintech scale via M-Pesa, and supports Vision 2030 growth. Completion is expected in Q1 ’26, subject to regulatory approvals.