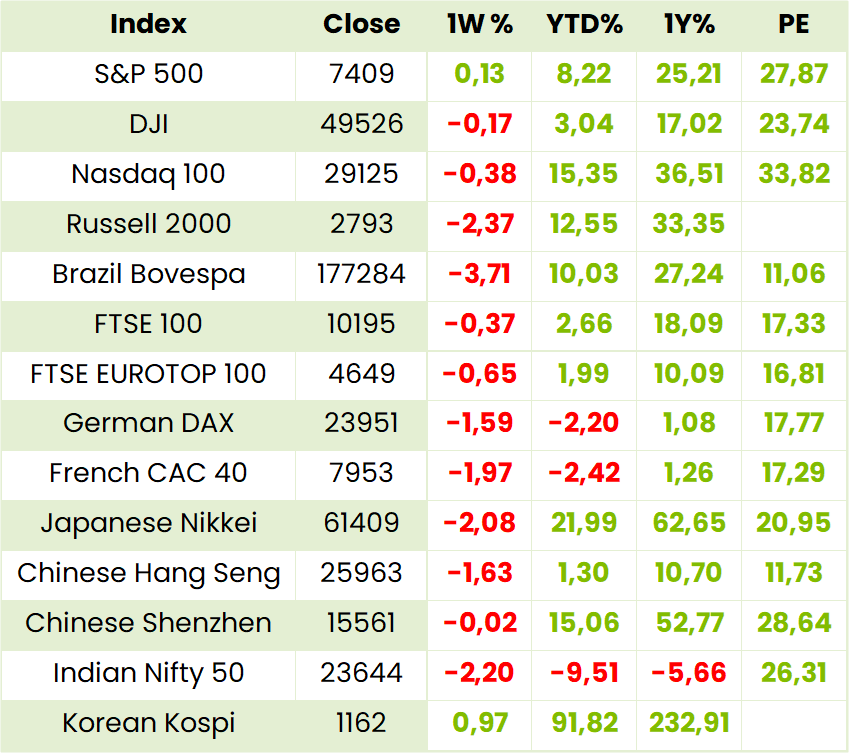

Global Indices

Currencies, Crypto & Commodities

SA Indices

SA Upcoming Indicators & Dividends

Global Equity

Tencent (0700.HK) Q1 Results Mar ‘26 (4555HKD)

HEPS: 7.517 (12% ↑ from 6.735)

EPS: 6.431 (22% ↑ from 5.252)

Operating Profit: RMB67.4bn (17% ↑ from RMB57.6bn)

Revenue: RMB196.5bn (9% ↑ from RMB180.0bn)

Gross Profit: RMB111.3bn (11% ↑ from RMB100.5bn)

EBITDA: RMB84.2bn (14% ↑ from RMB73.8bn)

Dividend: Not declared

Revenue growth was driven by strong performance in domestic and international games, AI-enhanced marketing services (+20% YoY), and FinTech & Business Services (+9% YoY). Gross margin improved to 57% (from 56%). Non-financial highlights include evergreen games hitting lifetime highs, Video Accounts’ time spent rising 20% YoY, and WorkBuddy becoming China’s most popular productivity AI agent. Tencent launched its Hy3 preview large language model in Apr ‘26, now top-ranked on OpenRouter. Outlook emphasises scaling AI-native products while leveraging cash flow from core businesses.

“Tencent is committed to advancing AI innovation while sustaining growth in our core businesses, ensuring long-term shareholder value.” – Pony Ma, Chairman & CEO.

Comment: after peaking pre-covid the share price peaked for the second time in September 2025 at similar levels and, with consensus still for a Strong Buy, it is now likely to resume its positive trend as the results were only a slight miss due to the timing of the Chinese New Year. So, just as Prosus/Naspers prices suffered headwinds in the downswing, they are likely to benefit now.

Prosus* (PRX) CEO Letter – 12 May ’26 (75243c)

Revenue: +$7.3bn (FY26)

Ecommerce aEBITDA: +$1.1bn

Share Buybacks: $5bn annually

Disposals: $2bn of non‑strategic assets

AI Deployment: 20+ assistants live, Zapia AI with 6m users

AI Agents: 5,000 agents completing ~4m tasks monthly

Cash Flow: Free cash flow growth across ecosystems

Highlights: Large Commerce Model expanded from Brazil to India and Europe.

OLX delivered >$450m aEBITDA; JET turnaround targeting $3.6bn revenue and $100m aEBITDA. PayU profitable, integrating ecosystem investments in India.

iFood diversified into quick commerce, fintech, ads, and vouchers, with advertising now a meaningful EBITDA contributor. Despite strong growth, FY27 adjusted EBITDA is expected to fall to $100–150m due to stepped‑up investment to defend market share against $1.5bn competitor spend.

CEO Outlook: “FY27 is a year of execution… building something special with results that will compound for many years.” – Fabricio Bloisi.

Comment: this year will be an acid test of Bloisi’s strategy and, as with many a major capex project, the outcome is uncertain. In addition, however, to the iFood diversifications mentioned above it is into pets, beverages and pharmaceuticals while 17% of Despegar’s net revenue is from iFood referrals. In the meantime, while awaiting the FY27 outcome, Bloisi will be giving his usual upbeat presentation on 29 June on the FY26 results. In addition, the share is more likely to experience upside this year than downside from Tencent itself.

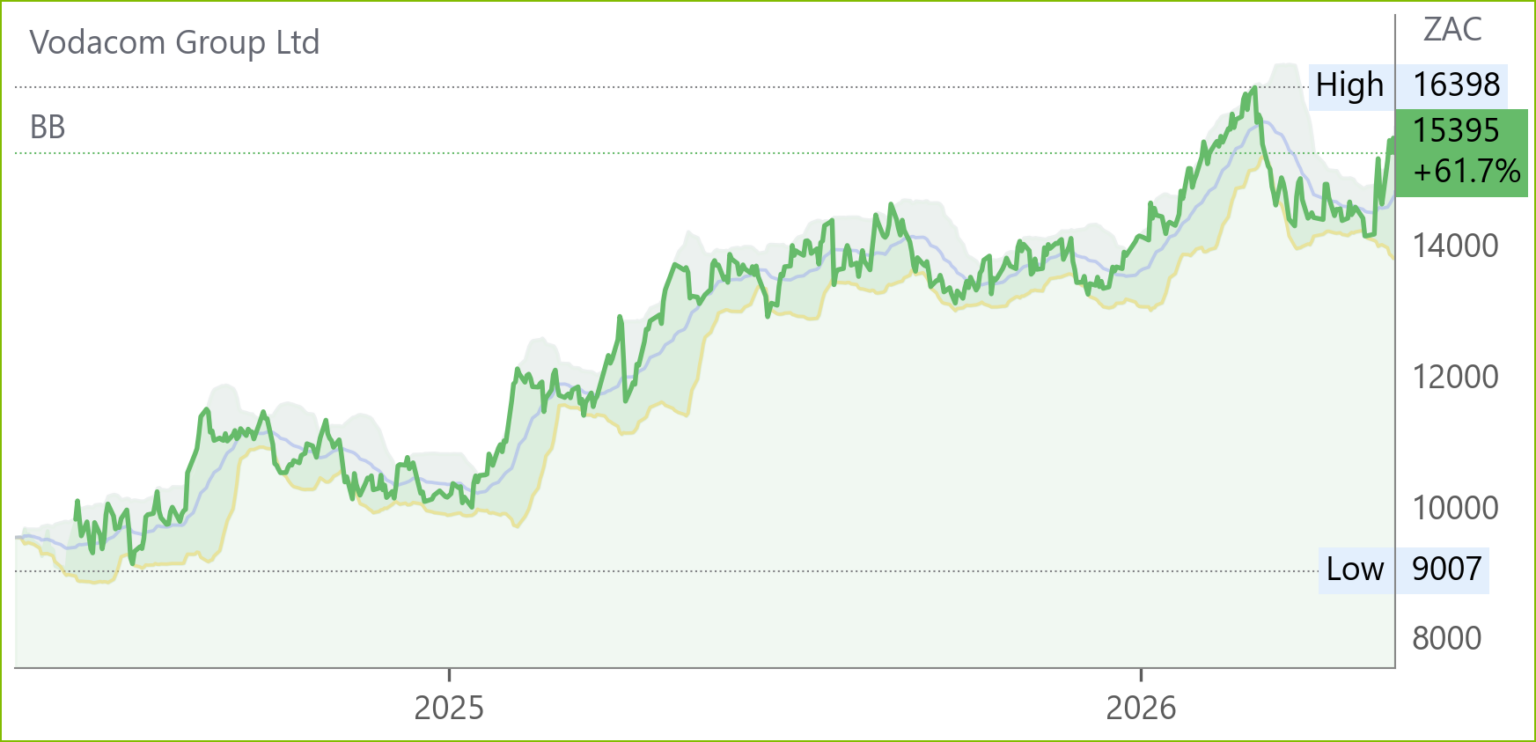

Vodacom* (VOD) Financial Results FY26 (15395c)

HEPS: 1053cps (↑22.9% from 857cps)

EPS: 1069cps (↑24.4% from 859cps)

Operating Profit: R44.1bn (↑23.2% from R35.8bn)

Revenue: R167.7bn (↑10.1% from R152.2bn)

EBITDA: R62.6bn (↑12.8% from R55.5bn)

Dividend: 735cps (↑18.5%), final dividend 405cps

Vodacom added 26m customers, taking its base to 237.3m, more than double its Vision 2030 annual target. Financial services customers rose 17.4% to 103m, with transaction values reaching US$525.6bn. Strong growth came from Egypt, Tanzania, DRC and Safaricom, which contributed R4.6bn to operating profit. Capital expenditure increased 16.5% to R23.6bn, supporting 6 160 new 5G sites and lifting smartphone penetration to 68.6%. ROCE expanded to 27.5%. Strategic acquisitions of Safaricom and Maziv are expected to materially enhance scale, diversification and fibre reach. Outlook remains resilient despite macroeconomic uncertainty, with upgraded Vision 2030 ambitions for 275m customers and 130m financial services users.

“We have delivered a strong start to our Vision 2030 strategy, staying true to our strengths while confidently stepping into the next phase of our growth journey.” – Shameel Joosub, Group CEO. Comment: like its peer MTN, with which it competes head to head in SA but not elsewhere, growth for Vodacom came from its other African operations with Egypt in particular delivering 38.5% ebitda growth. SA ebitda declined 1.5% to R33bn while Vodacom Group grew 12.8% to R62.6bn with International growing 27.8% to R12.1bn. Safaricom, in which Vodacom had a 29% interest, grew ebitda 21.6% to R29.5bn but, following the December 2025 transaction whereby Vodacom is to increase its interest to 55%, growth with M Pesa around Kenya will be significantly enhanced. While energy costs will affect consumers and businesses in varying degrees, the bulk of SA energy requirements are met by the grid and the rest of Africa has lots of renewables. Diesel costs are 4% of service revenue and advance procurement of supplies and hedging will further mitigate the effect. SA operations will be enhanced by the successful conclusion of the multiyear Maziv deal process. The stock remains an attractive participant in ongoing African growth together with an acceptable dividend yield given its commitment to the 75% payout ratio.

Redefine* (RDF) Interim Results for 6M Feb ’26 (622c)

HEPS: 34.24cps (↑85.8% from 18.43cps)

EPS: 51.66cps (>100% from 21.72cps)

Revenue: R5.59bn (↑3.7% from R5.39bn)

Dividend: 21.83cps (↑6.9%), interim dividend declared

LTV: 40.3% (improved from 41.5%)

NAV: 815.09cps (↑4.3% from 781.50cps)

Redefine reported distributable income growth of 7.4% to R1.9bn, supported by property assets of R101.2bn and undrawn facilities of R5.4bn. Net operating profit margin stood at 77.2%. Management raised FY26 guidance, expecting distributable income per share to grow 6–7% to 55.55–56.07cps, with a dividend payout ratio of 80–90%. Strategy remains focused on portfolio diversification, asset recycling, cost containment and embedding sustainability. Outlook acknowledges global uncertainty but highlights resilience and earnings visibility. “Durability is not built in a crisis, it is revealed by one. Since 2019, Redefine has consistently emerged stronger and 2026 will be no different.” – Management commentary.

Comment: CEO Andrew Konig ascribes the steady performance of the portfolio to a flight to quality given that its buildings are mostly A grade and, he perhaps inferred, they aren’t building so many of them now. On his forecast the stock is on an 11.1x DIPS ratio and 7.6% FDY. The sector has had a good run since GNU but this is an acceptable yield with steady growth for income portfolios.

Octodec (OCT) Interim Results for 6M Feb ’26 (1682c)

HEPS: 88.22c (+15.4% from 76.42c)

EPS: 100.61c (+17.5% from 85.59c)

Revenue: R1.08bn (+2.4% from R1.05bn)

Dividend: 64.5c per share (interim, +4.0% from 62.0c)

NAV: R25.49 per share (+2.4% from R24.90)

LTV: 37.3% (improved from 37.9%)

Portfolio of 209 properties valued at R11.2bn delivered higher distributable income (R246.4m, +11.1%). Leasing activity improved, though vacancies rose due to two large tenant exits. Consumer confidence strengthened post-GNU formation, but geopolitical risks and rising oil prices pose inflationary pressures. Guidance revised to 3–5% distributable income growth with a minimum 77.5% payout ratio.

“Octodec remains committed to achieving its strategic objectives and creating increased long-term value for shareholders.” – Jeffrey Wapnick, CEO.

Comment: there have been many changes in recent years as management disposed of non-core holdings with the most significant being that of the Killarney Mall. More change is now likely with Emira having acquired 62.5m shares at prices around 1664cps to 1670cps for a holding of 27.5%. The PIC has also just acquired a holding of 6.063% at 1699cps. The 64.5cps interim dividend, together with the FY25 final of 72.5c makes for an 8% DY. The company claims to have the most significant REITS residential portfolio although its CBD properties (mainly in Tshwane but also in Johannesburg) include offices and street shops. The company is currently guiding for 3-4% growth although generally it has been in the mid-teens. The share price has recovered to near pre-covid levels. The share can be held currently for yield and to await further developments.

Balwin (BWN) Financial Results FY26 (384c)

HEPS: 47.72cps (↑4% from 45.9cps)

EPS: 52.36cps (↑5% from 49.9cps)

Revenue: R2.7bn (↑21% from R2.2bn)

Gross Profit: Margin 27% (↓ from 30%)

Dividend: No dividend declared

LTV: 38.1% (↓ from 40.4%)

NAV: 976.89cps (↑7% from 913.9cps)

Balwin delivered resilient growth with revenue up 21% to R2.7bn, driven by a 22% increase in apartment sales and 17% more handovers. Profit rose 9% to R254.5m, though gross margin fell to 27% due to land disposals. Recurring HEPS surged 41% to 56.44cps, reflecting core operations. The group advanced its rental strategy with The Eastlake achieving 99% occupancy, while investment property grew to R506.9m. Developments under construction rose to R6.9bn, supported by strong demand in the Western Cape. Cash generation improved to R198.7m, reducing LTV to 38.1%. No dividend was declared, with focus on debt reduction amid global uncertainty.

Comment: on an 8x PE and 61% discount to its 977c NAV the stock can hardly be accused of being overpriced even if the prospect of lower interest rates has receded. For the first time, sales in the Western Cape have taken first place although management has full confidence in the resurgence of Gauteng where it has just sold some land (in Waterfall) to keep debt within covenant levels. While the company has begun renting on a modest scale, the bulk of sales (60%) are to investors with most of the rest to owners. The slashing of the dividend produced an analyst’s grumble that, with the share price way below where it was years ago, shouldn’t the directors’ R55m in fees be slashed too? Apart from Nedbank’s c.5% holding, institutional holders still appear to be absent leaving the free float, with founder and CEO Steve Brookes holding 33% and MD Rodney Gray c.10%, a little problematical for building up stakes. For private investors who don’t want the hassle of buying units and managing tenants themselves, however, the stock as its attractions.

Raubex (RBX) Financial Results FY26 (5000c)

HEPS: 611.3cps (↑1.9% from 599.8cps)

EPS: 610.2cps (↑1.4% from 601.7cps)

Operating Profit: R1.74bn (↑11.6% from R1.56bn)

Revenue: R22.05bn (↑4.6% from R21.08bn)

Dividend: 121cps (↑16.3%), final dividend declared

Raubex delivered resilient results despite geopolitical and local challenges, supported by a strong balance sheet and robust order book, which rose 11.6% to R31.46bn. Cash generated from operations fell 30.3% to R1.75bn, while NAV increased to R7.87bn. Capital expenditure eased to R1.20bn. The Group’s diversification strategy across multiple sectors continues to underpin growth opportunities. CEO Felicia Msiza highlighted the strength of the order book, providing meaningful earnings visibility, and praised the workforce’s dedication and management’s strategic leadership. Outlook remains positive, with diversification and a high-quality order pipeline expected to sustain growth momentum.

Comment: Raubex has five divisions: Materials Handling and Mining; Construction Materials; Roads and Earthworks; Infrastructure and Australia (by far the smallest) most of which themselves comprise several different businesses. The broad picture is, however, clear: after a lacklustre first half, momentum picked up in the second half. Not only will FY27 Heps therefore be much better, but the order book has grown by 12% to R31.5bn and the pipeline is growing steadily with indications that this will continue for some years to come as the company benefits from reforms boosting infrastructure spending. Most contracts will provide for recovery of costs such as fuel hikes although this is bound to have some effect. Nevertheless, it is not hard to see FY27 heps growing by 30 % to around 792c for a FPE of 6.7x which, bearing in mind the promising multiyear pipeline, makes BUY a serious consideration.

Boxer Retail (BOX) Financial Results FY26 (8652c)

HEPS (351.67c, ↓15.0%) and EPS (343.50c, ↓15.5%) fell because of share dilution from the IPO. Although headline earnings in absolute terms grew 13.2% to R1.6bn, the larger number of shares in issue reduced the per‑share metrics.

Operating Profit: R2.64bn (↑17.3% from R2.25bn)

Revenue: R46.7bn (↑12.3% from R41.6bn, 52/52w)

Dividend: 95.37cps (140.67cps total, including interim)

Explanation: EPS and HEPS declined >30% due to IPO share issuance dilution, despite headline earnings growth.

Turnover rose 12.3% on a 52/52w basis, supported by 51 new stores and 4.5% like-for-like sales growth. Trading profit grew 17.3% with margin expansion to 5.7%. Employment increased by 3,400 to 35,314, while net cash improved to R709m from net debt of R180m. ROIC reached 26% (66.7% ex-IFRS16), underscoring operational strength. IPO-related dilution reduced per share metrics, though absolute headline earnings grew 13.2% to R1.6bn. Outlook for FY27 is clouded by elevated oil prices and Persian Gulf conflict, expected to pressure food inflation and logistics. Boxer remains focused on long-term growth and value delivery. “Boxer will continue to build the business for the long term by remaining resolutely focused on providing value to its customers.” – Marek Masojada, CEO

Comment: the recent price spike has in effect rewarded Boxer for the creditable performance which will continue as it can open many more stores without cannibalisation. The terrain is, however, intensely competitive: it remains for example to be seen whether fuel price hikes work to the benefit of its informal and other

small competitors embedded in townships beyond walking distance of Boxer outlets.

In any event, unless Heps growth is going to settle in the twenties rather than, as seem likely, the mid to upper teens, it would appear to be fully valued albeit still a long term Hold.

Bytes Technology Group (BYI) Annual Results FY26 (7785c, 345.8GBp)

HEPS: 21.4p (‑6.1% from 22.8p)

EPS: 21.4p (‑6.1% from 22.8p)

Operating Profit: £62.7m (‑5.6% from £66.4m)

Revenue: £220.5m (+1.6% from £217.1m)

Gross Profit: £167.3m (+2.5% from £163.3m)

Dividend: 7.0p final (full‑year 10.2p, +1.4%)

Gross invoiced income rose 11.5% with strong services growth (+24.6%). Public sector gross profit increased 7.4%, while private sector was marginally lower due to sales structure refinement. Cash conversion remained robust at 105%, with £74m returned to shareholders including a £25m buyback. Headcount grew 6.9% to 1,331, reflecting investment in sales and service delivery. Recognition included ranking 14th in the FT’s UK Best Employers list and multiple vendor awards. Outlook points to high single-digit to low double-digit gross profit growth in FY27, with operating profit broadly flat as cost normalisation occurs. “This has been a year of adaptation and evolution against a more challenging market backdrop… We are well positioned, as a Microsoft Frontier Partner, to be the partner for our customers on this journey.” – Sam Mudd, CEO. Comment: despite its South African origins, Bytes enjoys an offshore rating as evidenced by JP Morgan’s post results acquisition of a 5.4% holding. It has recovered from the Microsoft change in partnership arrangements hiccough and can now be bought.

Karooooo (KRO) Financial Results for FY26 (75435c)

HEPS: ZAR32.17 (↑8% from ZAR29.81)

EPS: ZAR32.17 (↑8% from ZAR29.81)

Operating Profit: ZAR1,415m (↑8% from ZAR1,312m)

Revenue: ZAR4,844m (↑19% from ZAR4,068m)

Dividend: USD38.6m paid Aug ’25

Cartrack subscribers rose 16% to 2.66m, with record net additions of 360k. Subscription revenue grew 19% to ZAR4.8bn, while Logistics DaaS revenue advanced 29% to ZAR540m. Operating profit increased 8% despite margin pressure from growth investments. Adjusted free cash flow surged 90% to ZAR809m, supported by strong collections and reduced capital outflows. CEO Zak Calisto highlighted accelerated annual recurring revenue (ARR) growth in South Africa (+23%) and new product launches including Cartrack-Tag and AI-powered video. FY27 guidance points to subscription revenue of ZAR5.7–6.0bn, EPS growth of 18%–23%, and operating margins of 27%–30%.

Comment: other metrics belie the strong ZAR affected Heps growth of 8% and the current 21.8x PE is well below the Nasdaq average of 29.2x. It is only a matter of time before the rating of this stock moves more in line which makes it a BUY.

KAL (KAL) Interim Results for 6M Mar 26 (4470c)

HEPS: 441.36c (↑12.5% from 392.47c)

EPS: 513.87c (↑30.3% from 394.29c)

Operating Profit: Not disclosed

Revenue: R11.36bn (↑5.0% from R10.82bn)

Gross Profit: R1.81bn (↑8.8% from R1.66bn)

EBITDA: R599.7m (↑7.7% from R557.1m)

Dividend: Interim 70c per share (↑25% from 56c)

Revenue growth of 5% and stronger gross profit supported a 30% rise in EPS, while HEPS increased 12.5%. Debt metrics improved significantly, with net interest-bearing debt to equity reduced to 32.9% from 48.4%. Cash generation remained solid at R575m. The board declared a 70c interim dividend, reflecting confidence in cash flows. Management highlighted operational resilience and disciplined capital allocation, positioning the business for sustainable growth. Outlook remains constructive, with focus on margin improvement and balance sheet strength.

Trading Statements & Updates

MTN* (MTN) Quarterly Update for 3M Mar ’26 (20810c)

Revenue: Service revenue +20.0% (constant currency +21.1%)

EBITDA: +27.9%* (margin 47.6%, +3.0pp)

Subscribers rose 5.4% to 312.7m, with active data users up 8.7% to 175.6m and MoMo MAU up 8.2% to 67.4m. Data traffic surged 20.2% to 6,827PB, while fintech transaction value climbed 32.8%* to US$163bn. Nigeria (+41.7%* service revenue) and Ghana (+35.7%) led growth, offsetting muted South Africa (+0.7%). Capex of R9.6bn supported network resilience, with leverage at 0.2x and HoldCo liquidity of R42.6bn. Strategic progress included fintech separation approvals in Ghana and Nigeria, and advancement of the IHS tower acquisition. Digital infrastructure revenue was resilient, with fibre external revenue up 34.6%. Outlook remains positive, with medium-term guidance reaffirmed: Group service revenue growth ‘at least high-teens’, Nigeria ‘low-20%+’, SA ‘low to mid-single digits’, and Fintech ‘high-20% to low-30%’.

“MTN Group has reported a strong overall performance and resilient financial results despite an uncertain geopolitical and macro-economic environment.” – Ralph Mupita, Group President & CEO.

Foschini (TFG) Trading Statement FY26 (5807c)

HEPS: 609.4–710.9cps (↓40% to ↓30% from 1 015.6cps)

EPS: 343.2–441.3cps (↓65% to ↓55% from 980.6cps)

Revenue: R62.4bn (↑7.1% from R58.3bn)

Group sales grew 7.1% (7.7% constant currency), supported by strong growth in London (+29.4% in GBP) and Africa (+5.0%), while Australia contracted (-1.5% in AUD). White Stuff contributed positively, with pro forma sales up 4.3%. EPS was heavily impacted by c.R750m impairments in Phase Eight, Tarocash and yd., alongside weaker margins in Africa and higher interest costs. HEPS declined 30–40%. Outlook remains cautious, with geopolitical uncertainty and consumer pressure expected to weigh on trading, though management emphasises cost discipline and operational efficiencies. Results due 5 Jun ’26.

Tharisa (THA) Trading Statement – Interim Results for 6M Mar 26 (2893c)

HEPS: US 16.1–16.6c (↑455%–472% from US 2.9c)

EPS: US 15.3–15.8c (↑512%–532% from US 2.5c)

Earnings surged on stronger commodity prices and improved operational performance, with EPS and HEPS rising more than 450% year-on-year. The uplift reflects robust chrome and PGM markets alongside disciplined cost control. Strategic projects, including the Karo Platinum development in Zimbabwe and downstream beneficiation initiatives, reinforce growth prospects. Sustainability commitments remain central, with targets to cut carbon emissions by 30% by 2030 and achieve net neutrality by 2050. Proprietary Redox One battery technology highlights innovation in energy storage. Interim results due 21 May ’26

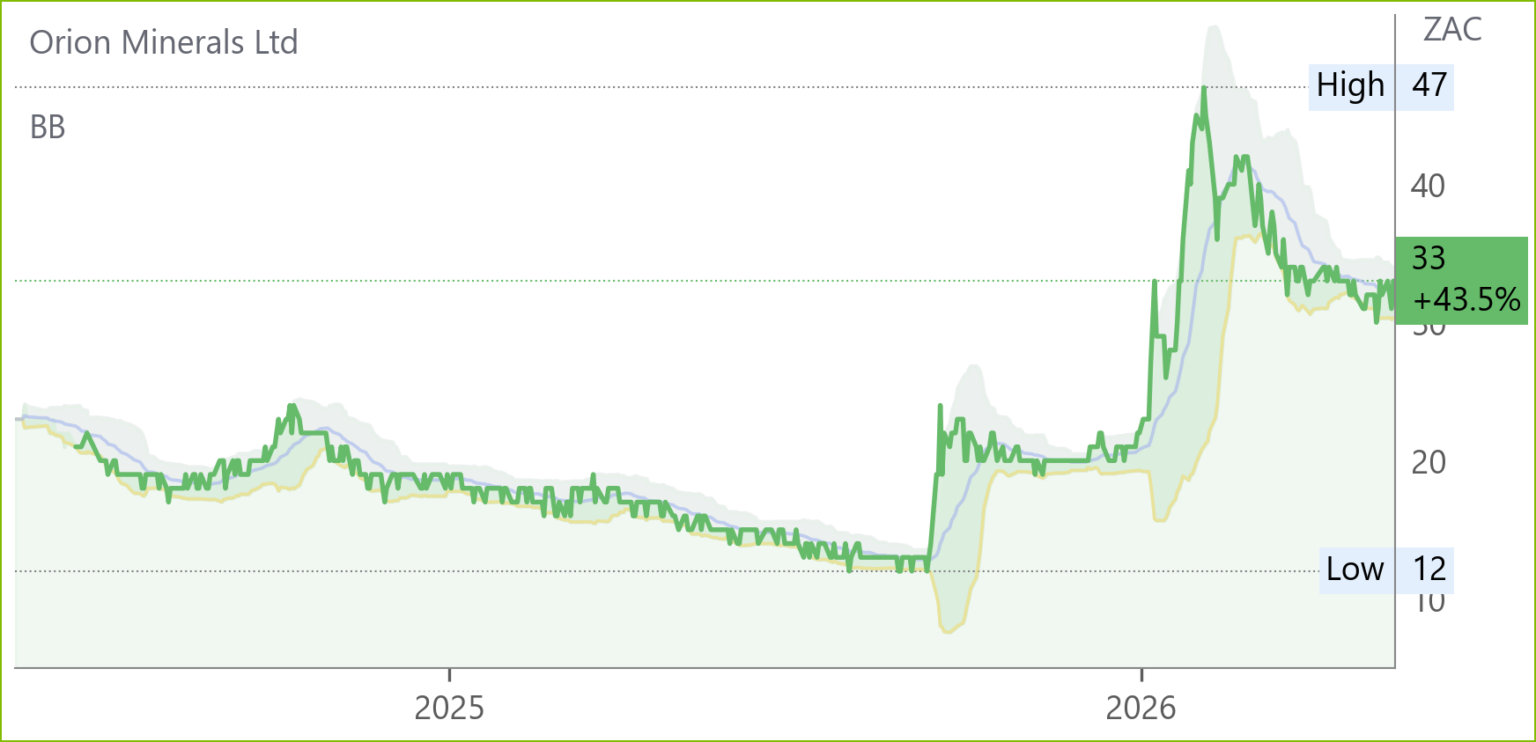

Orion Minerals (ORN) Resource Optimisation – Okiep Copper Project (33c)

Recent drilling at Flat Mine East intersected 7.88m of visible copper sulphide mineralisation (OFMED157) 36m down‑dip from OFMED154 (15m @ 4.80% Cu). Results confirm continuity with OFMED153 (49.35m @ 5.05% Cu). Updated Flat Mines resource stands at 10Mt @ 1.3% Cu. Mineralisation remains open down‑dip, with assays due in three weeks. CEO Tony Lennox highlighted strong growth potential, reinforcing Flat Mines as a cornerstone of Orion’s Okiep strategy.

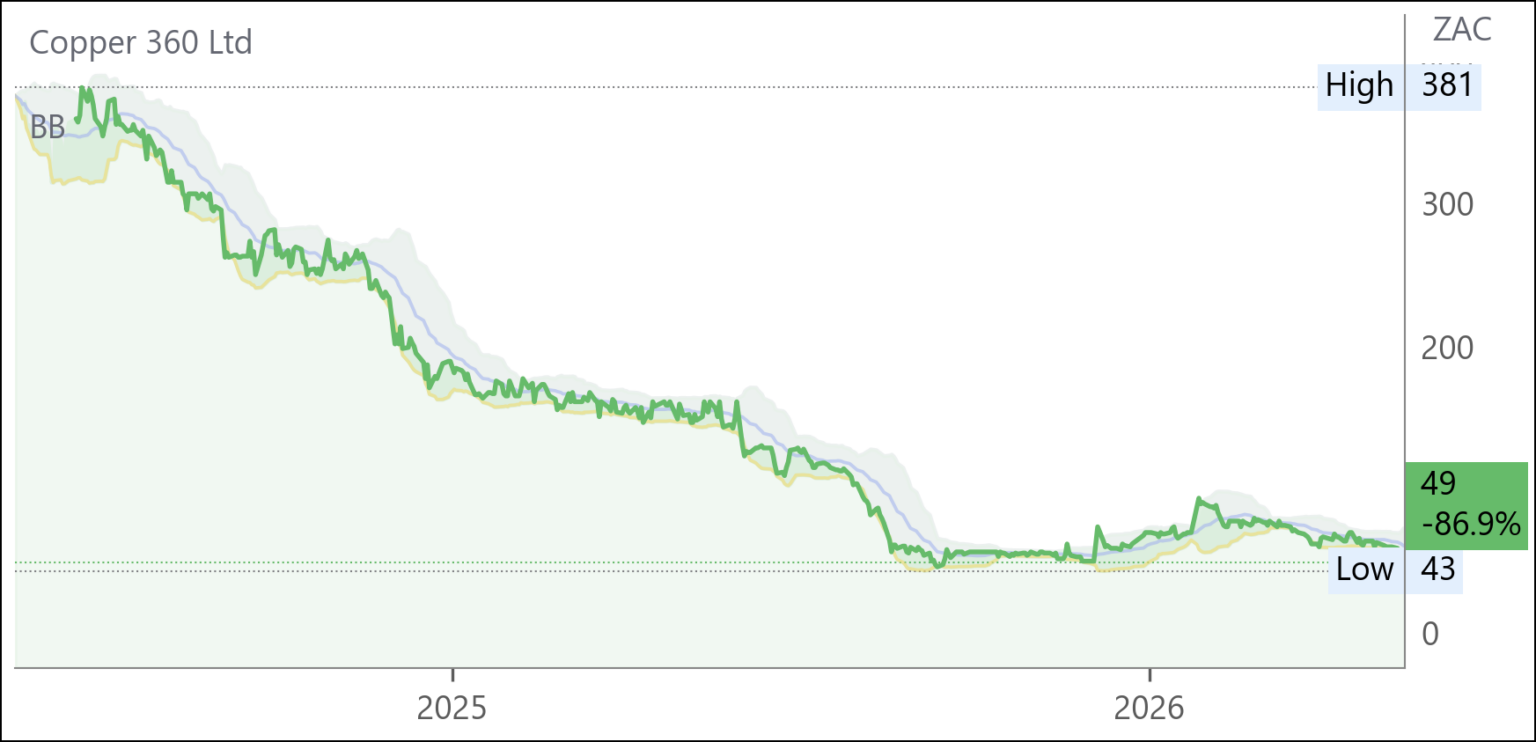

Copper 360 (CPR) Strategic Repositioning Update (49c)

Copper 360 has approved a restructuring to prioritise higher‑grade in‑situ ore at Rietberg, suspending lower‑grade stock processing. Capital will be redirected to underground development over 4–5 months, aiming to improve economics and sustainability. Labour consultations are underway to align workforce structures. Operational optimisation initiatives target efficiency gains, while optionality remains through the SX‑EW and near‑complete MFP1 plant, which could double processing capacity.

“Our conclusion is that this restructuring is a necessary and decisive step to preserve capital and reposition the Company in a sustainable operating model.” – Rupert Smith, Chairman.

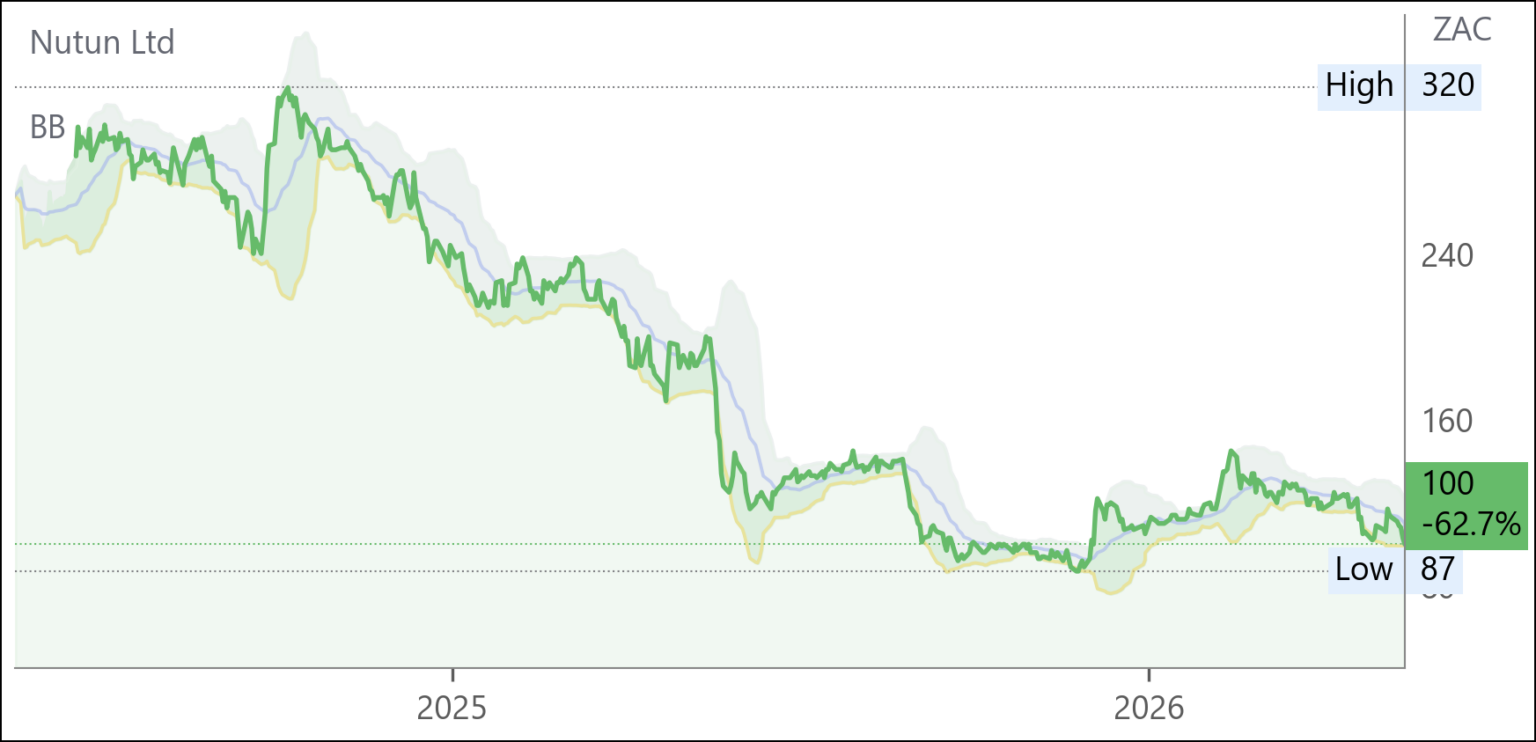

Nutun (NTU) Trading Statement for 6M Mar 26 (100c)

HEPS: -7.5c to -8.6c (↓44–52% from -15.6c)

EPS: -7.5c to -8.6c (↓44–52% from -15.6c)

Losses narrowed significantly, with headline loss per share halving compared to the prior period.

Operational performance was strong, particularly in South Africa, supported by streamlined structures and established client bases. Earnings were negatively impacted by Rand strength and accelerated amortisation linked to macroeconomic assumptions, including elevated interest rate forecasts. Headline loss reduced to between R59m and R68m, compared to R122m in the prior period, reflecting improved trading momentum. International operations remained resilient, with focus on profitability in the short-to-medium term and sustainable growth over the long term. Results due 18 May ’26.

Snippets

Naspers* (NPN) announced that Prosus (PRX) sold a 5% stake in Delivery Hero to Aspex Management for €22.00 per share, raising gross proceeds of c.€335m. The deal represents a 10% premium to the closing price and a 22% premium to the 30‑day VWAP. This follows the April 2026 sale of 4.5% to Uber and advances commitments to the European Commission.

Spear REIT (SEA) sold Hamilton and Chiappini House in Cape Town for ~R107m, up from the R80.75m acquisition in Oct ’24. The disposal yield was 7.5%, adding 5c to NAV. Competition authority approval makes the deal unconditional, crystallising R26m value uplift. The disposal reduces exposure to decentralised offices, aligning with Spear’s capital recycling strategy into higher‑yielding Western Cape assets.

MAS (MSP) is in advanced negotiations with two independent parties regarding the potential disposal of either a wholly owned enclosed mall or six wholly owned open‑air malls. Due diligence is largely complete, and the company aims to conclude at least one transaction subject to pricing, certainty, and execution risk. Flexibility remains to proceed with multiple disposals.

Labat Africa (LAB) issued a cautionary announcement on plans to acquire the remaining 24.45% stake in Classic International Trading. The deal, subject to agreements and approvals, could materially affect Labat’s share price. Classic’s strong performance has boosted Labat’s results, and full ownership aligns with its strategy to consolidate high‑growth subsidiaries.