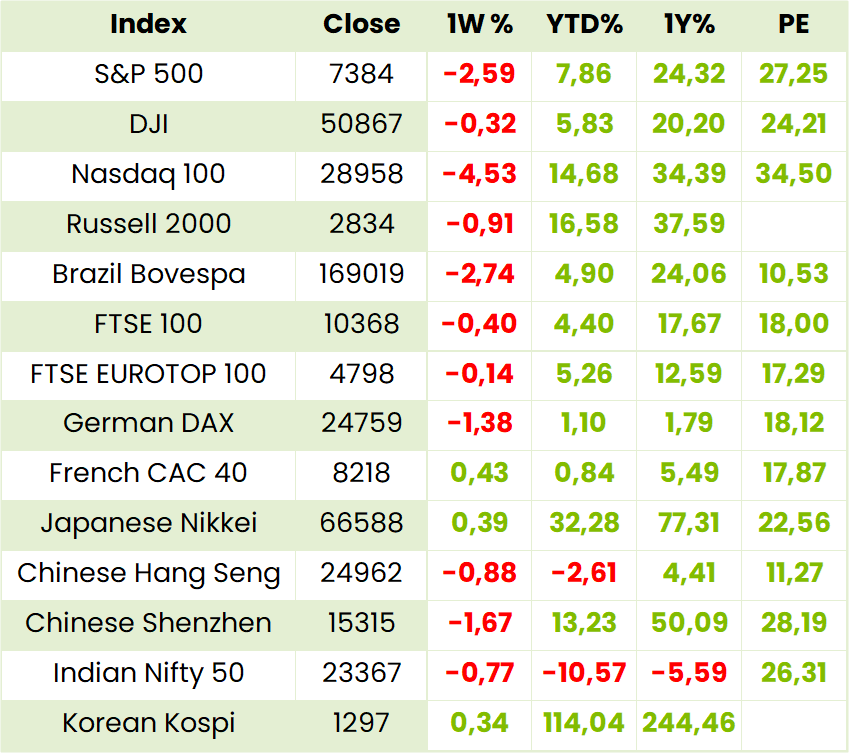

Global Indices

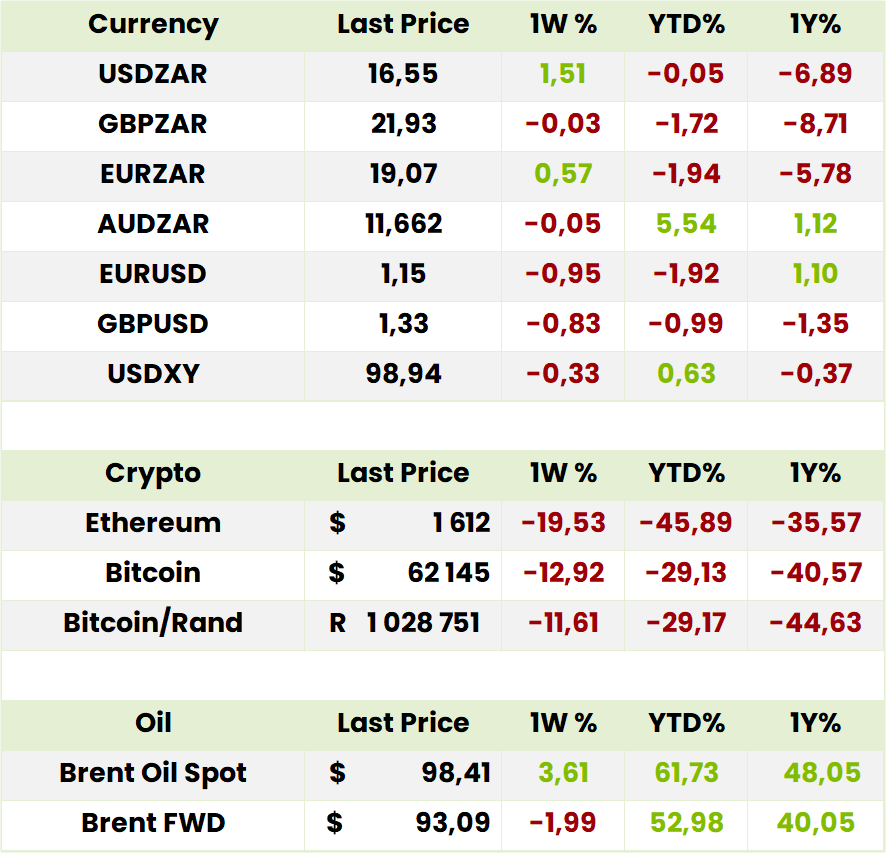

Currencies, Crypto & Commodities

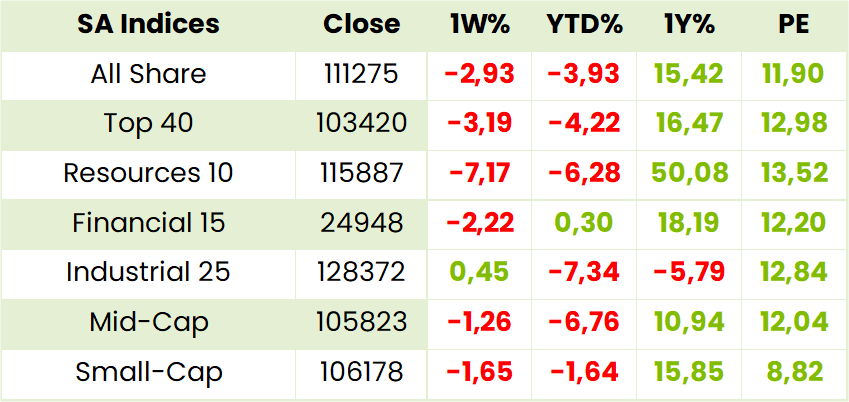

SA Indices

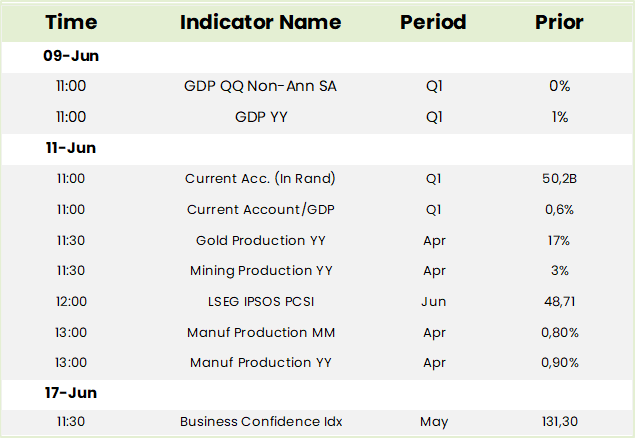

SA Upcoming Indicators & Dividends

*holding in a Finova portfolio

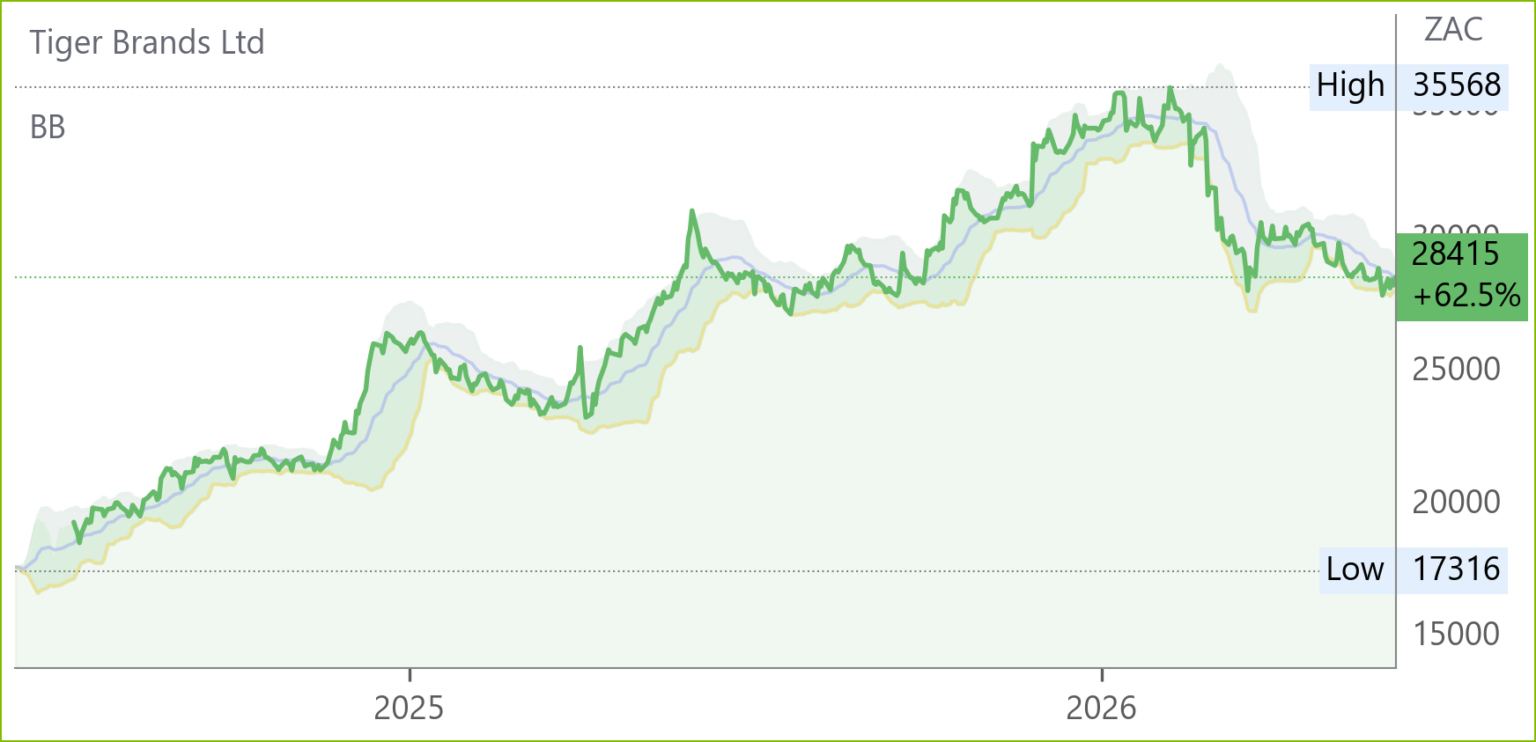

Tiger Brands (TBS) Financial Results for 6M Mar ’26 (28145c)

HEPS: 1 001c (↑6.5% from 940c)

EPS: 1 077c (↓19.4% from 1 336c)

Operating Profit: R2.1bn (↑26.1% from R1.6bn)ps

Revenue: R17.9bn (↑1.3% from R17.7bn)

Gross Profit: Margin ↑ to 32.1% (H1 ’25: 29.8%)

Dividend: 430c interim (↑3.6% from 415c)

Strong volume growth of 4.5% and efficiency gains lifted operating income, despite EPS decline from prior year disposals. Grains delivered standout operating profit growth (+91.7%), while Culinary and Snacks also improved margins. Portfolio optimisation continued with Randfontein disposal and Beacon chocolate sale agreement. Net debt rose to R1.7bn due to capital allocation strategy, but ROE improved to 26.3%. CEO TN Kruger stated: “Our focus on affordability and efficiency continues to underpin sustainable growth.” Outlook highlights cost leadership, innovation in Grains and HPC recovery, and completion of Chococam disposal by FY26.

Comment: with much of portfolio optimisation achieved, the 3926c total ordinary and special dividend of FY25 will not be repeated leaving the stock nevertheless on an attractive trailing 6% DY and 13.2x PE. Management, understandably, went to some lengths to explain the need to retain Jelly Babies and not Beacon Chocolate which does not fit in to the Snacks portfolio and is also confident it has taken strong measures to mitigate expected inflationary pressures.

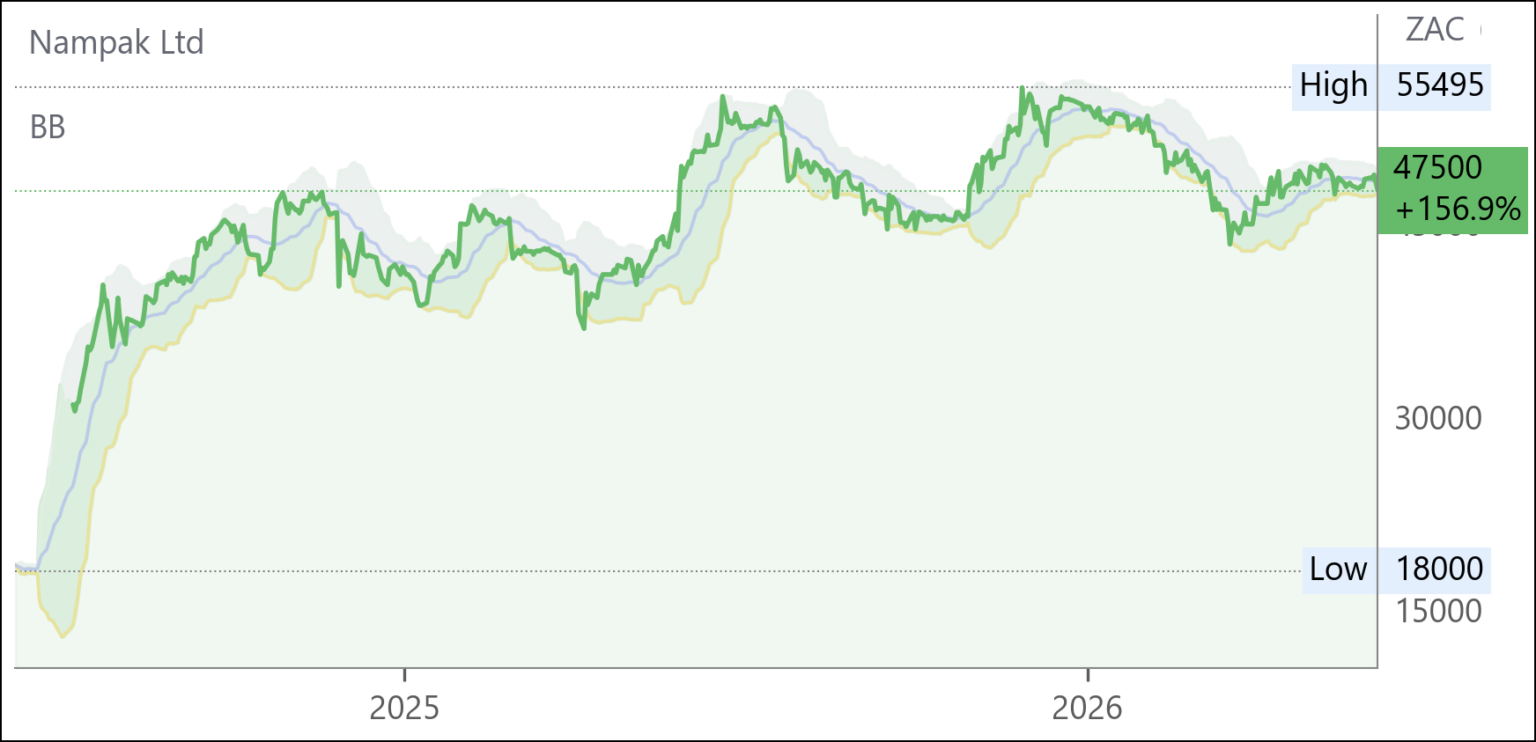

Nampak (NPK) Financial Results for 6M Mar ’26 (47500c)

HEPS: 3399.5c down 40%

EPS: 5517.8c down -85%

Operating Profit: Lower due to weaker Diversified contributions and Angolan can‑line relocation costs

Normalised HEPS rose 8 %, to 4131.6c aided by lower finance costs, but headline earnings fell sharply. EPS benefited from a R239m impairment reversal in Beverage Angola, though total EPS plunged on the absence of prior year disposal gains and a R70m impairment in Zimbabwe. The prior period included a R2.5bn profit on disposals, inflating comparatives.

Comment: with the plant relocated from Angola to Springs in production by December the SA beverage division outlook is “relatively resilient” with can end imports from China being addressed by duty application. The outlook in Angola is positive and the business is expected to remain a growth driver with no capex imminent. The sale of the 51.4% interest in Zimbabwe is progressing and proceeds will used for further debt reduction from the 2.2x Ebitda, excluding Angola, level down from 2.9x in 1H 25. The

Board remains “focused on resuming a dividend declaration from the year-end, subject to full year performance.” No rush to buy but can be Held for continued recovery.

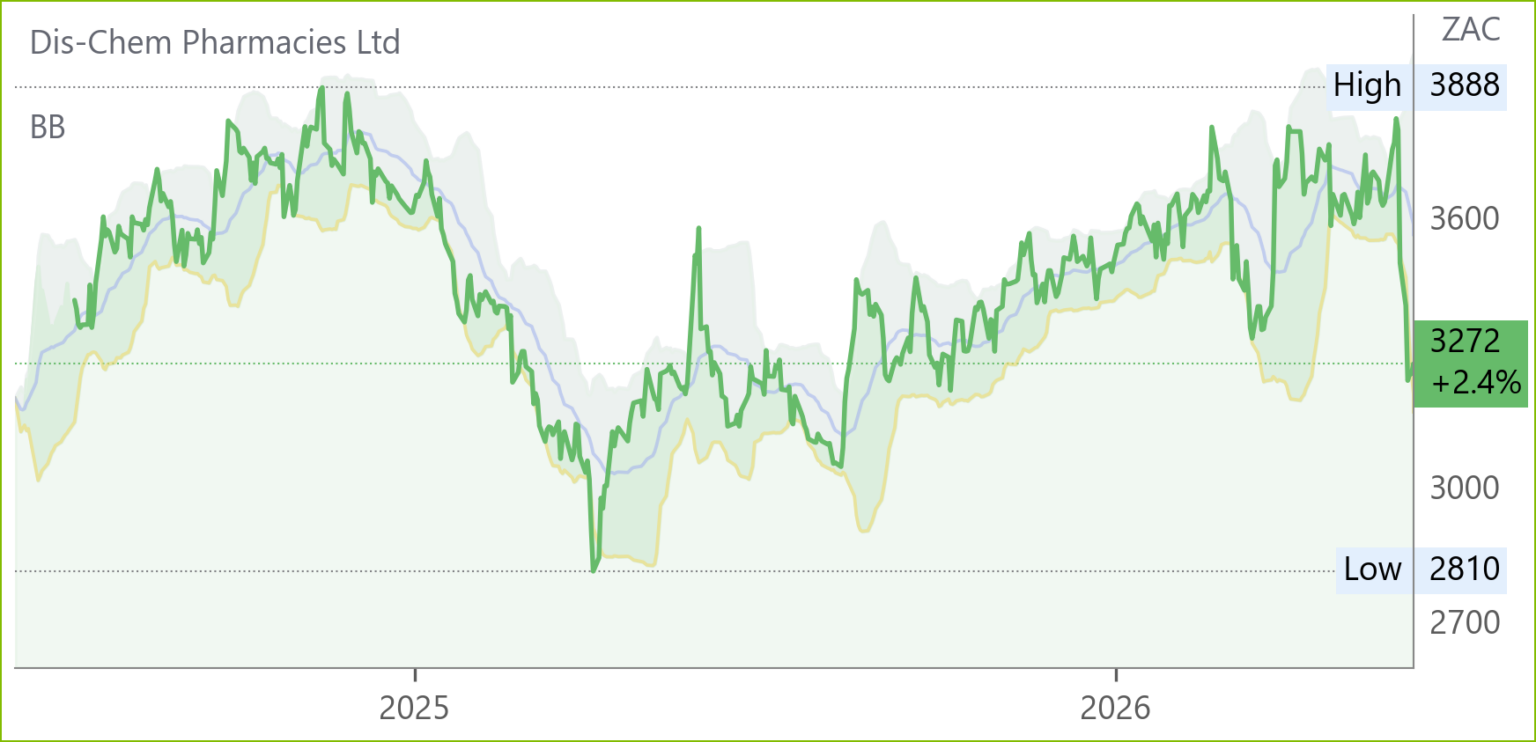

Dis‑Chem (DCP) Financial Results for FY26 (3272c)

HEPS: 113.7c (-17.3% from 137.65c)

EPS: 114.2c (17.1% from 137.6c)

Operating Profit: R2.9bn (↑6.8% from R2.7bn)

Revenue: R36.2bn (↑9.2% from R33.2bn)

Gross Profit: R9.6bn (↑8.5% from R8.8bn)

EBITDA: R3.6bn (↑7.1% from R3.4bn)

Dividend: 45.34c per share (total)-17.3%

Growth was driven by strong retail sales, particularly in health and beauty, and continued expansion of pharmacy services. Wholesale operations contributed positively despite margin pressure from logistics costs. Store footprint expanded with 20 new outlets, enhancing market share. Digital channels saw double‑digit growth, reinforcing omnichannel strategy.

Comment: Trading performance of the core retail business, when excluding R445 million invested in the ecosystem and eliminating non-recurring expenses, was pleasing, with core retail profit before tax increasing by 27.1% over the comparable period. CEO Rui Morais is candid about the risks involved in the strategic aim of creating “an ecosystem that positions the Group to play the dual role of healthcare provider and funder; using an innovative operating model to reimagine and disrupt the manner in which South Africans access healthcare”. He says, however, that the option of “staying safe” would end in stagnation. No doubt he has a point with the share price having gone nowhere in nearly nine years and bearing in mind what happened to SA’s leading retailer when it let things slide. Meanwhile, risk averse investors should rather await early signs of success.

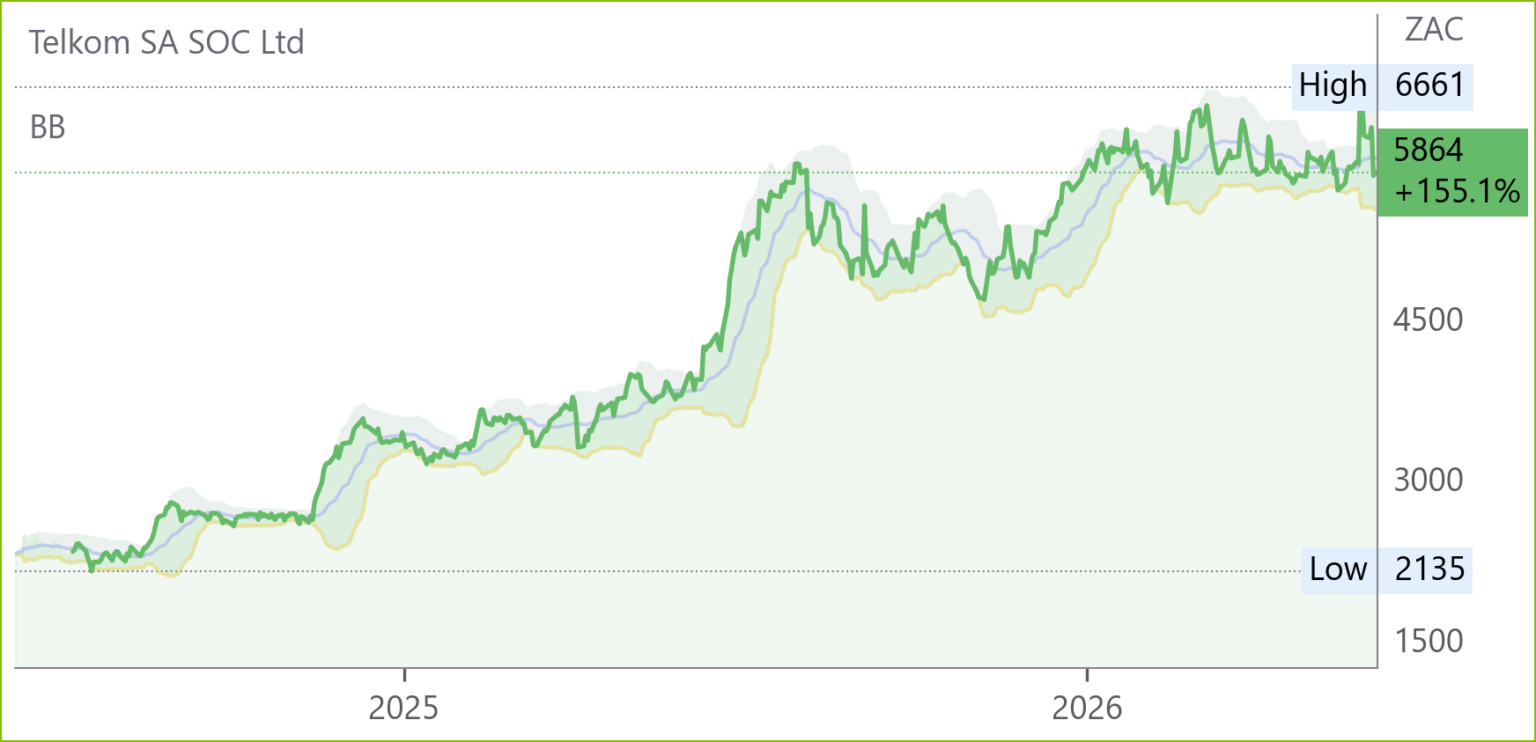

Telkom (TKG) Financial Results FY26 (5864c)

HEPS: 708.5c (↑21.5% from 583.2c)

EPS: 719.5c (↑5.5% from 681.7c)

Operating Profit: R3.55bn (↑5.9% from R3.35bn adjusted)

Revenue: R44.48bn (↑1.4% from R43.88bn)

Gross Profit: Margin expansion in Consumer and Openserve; BCX stable

EBITDA: R12.48bn (↑5.8% from R11.79bn adjusted)

Dividend: 270c per share (↑65.7% YoY payout ratio uplift)

Data‑led strategy drove growth, with mobile data revenue up 10.5% and fibre‑related data up 6.3%. Consumer mobile subscribers surpassed 25m, sustaining service revenue growth for 14 consecutive quarters. Openserve achieved full‑year revenue growth for the first time in nine years, signalling fibre transition completion. Free cash flow rose 10.4% to R3.07bn, supporting a higher dividend payout ratio of 40–60%. CEO Serame Taukobong stated: “These results validate our transformation strategy as we position Telkom for consistent quality earnings and enhanced shareholder returns.” Outlook highlights disciplined capex allocation (12–15% intensity), cost efficiencies, and continued focus on mobile and fibre expansion.

Comment: Telkom continues to leverage its legacy assets so as to achieve solid, if unspectacular, growth in the intensely competitive South African market which is something which its bigger peers struggle with despite spectacular growth elsewhere.

Sirius Real Estate (SRE) Financial Results FY26 (2130c)

HEPS: 6.56c (↓18.6% from 8.06c)

EPS: 15.16c (↑24.3% from 12.20c)

Operating Profit: €211.4m (↑4.9% from €201.6m)

Revenue: Rent roll €224.2m (↑6.4% from €210.8m)

Dividend: 6.40c per share (↑4.1% YoY, interim 3.22c)

LTV: 36.1% (↑ from 31.4%)

NAV: Adjusted NAV per share 124.78c (↑5% from 118.89c)

Funds from Operations rose 8.4% to €133.5m, supported by strong rent roll growth in Germany and the UK. Profit after tax surged 29% to €229.8m, aided by deferred tax releases. Portfolio value increased 20.5% to €2.97bn, driven by €463m of acquisitions, including €155m in defence‑related assets. Liquidity remains robust with €372.7m cash and a €300m undrawn facility, though net LTV rose to 36.1%. CEO Andrew Coombs stated: “Sirius has delivered another strong performance, with 12 consecutive years of rent roll growth above 5% and our 25th progressive dividend payout.” Outlook highlights further growth opportunities in defence and self‑storage sectors, with continued support from equity and debt markets. Comments: CEO Coombs ascribes ongoing success in achieving over 5% annual rental growth to 150 staff servicing customers, mostly small businesses, in 500 locations, with close attention and assistance in meeting their growth needs. Some €500m in acquisitions, which only contributed in 2H 26, will boost earnings for the full FY27. While the government in Germany, which contributes 75% of revenue, is business friendly the UK Labour government is less so. Further growth is, however, anticipated.

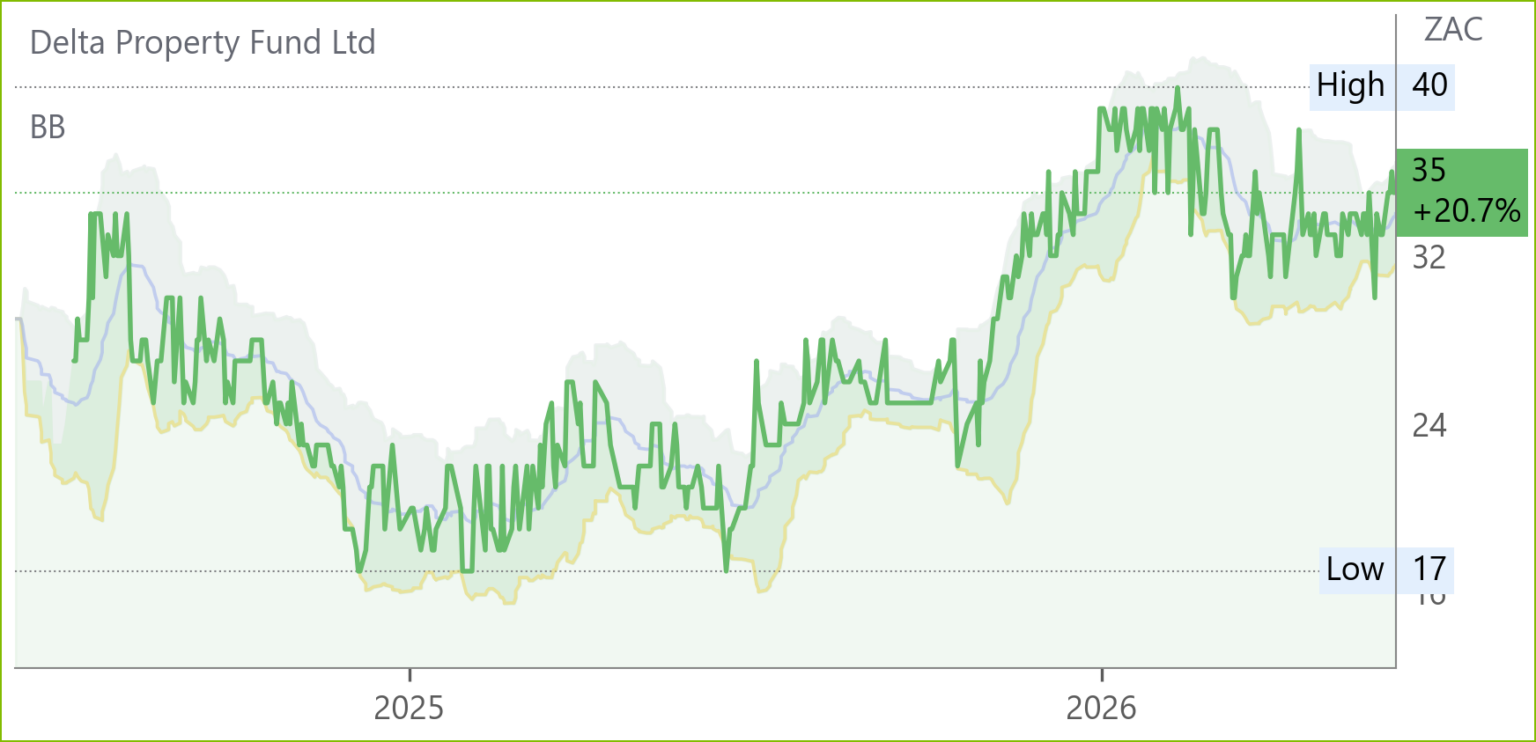

Delta Property Fund (DLT) Financial Results FY26 (35c)

HEPS: 14.9c (↑43.3% from 10.4c)

EPS: 17.8c (↑43.3% from 12.4c)

Net Operating Income: R674.9m (↓6.4% from R721.4m)

Revenue: R1.15bn (↑0.9% from R1.14bn)

LTV: 56.7% (↓ from 59.5%)

NAV: R3.6/share (↑5.3% from R3.4)

The Group’s property portfolio was independently valued at year-end, resulting in a fair

value gain of R20.4m (FY25: loss of R178.3m)

Net profit surged 221.9% to R127m, reversing a prior loss of R104m, supported by disposals, lower finance costs and improved collections (99.8%). Vacancies reduced to 27.3% from 31.9%, aided by lease renewals and non‑core asset sales worth R186m. Debt fell to R3.6bn, with covenant metrics improving. Management emphasised disposals, debt reduction and cost optimisation to sustain recovery. Outlook remains cautious given inflationary pressures, high municipal charges and competitive leasing conditions, but continued progress on portfolio optimisation and balance sheet strengthening is expected to support recovery. Comment: Delta has been in the throes of disposals and debt reduction for years and the share price is still where it was six years ago. The “SA REIT net asset value per share (is) R3.6 (February 2025: R3.4)” but the market doesn’t seem to believe it. Judging by the above it could still be a while!

Mediclinic Financial Results for FY26 (no JSE listing – delisted, announced by Remgro (REM)

HEPS: Adjusted earnings $345m (↑45% from $239m)

EPS: Loss $(733)m (vs $(4)m) due to impairments

Operating Profit: Adjusted $538m (↑30% from $415m)

Revenue: $5 356m (↑11% from $4 818m)

EBITDA: $842m (↑14% from $737m); margin 15.7% (FY25: 15.3%)

Dividend: Not declared

Performance was underpinned by strong patient activity, favourable mix changes, and efficiency gains. Adjusted earnings rose sharply, but statutory earnings were hit by $555m impairment on Hirslanden (Swiss division) and $689m further Swiss asset impairments. Net debt remained stable at $2.27bn with leverage reduced to 2.7x. A restructuring agreement will see Remgro acquire Mediclinic Southern Africa for $950m and MSC take full ownership of Hirslanden, with both divisions classified as discontinued operations. Management highlighted resilience despite geopolitical and macroeconomic challenges, with cash conversion at 106%.

Comment: like its peers, who recently posted positive results, Mediclinic’s interims were satisfactory at the operating level and confirm our positive view of Remgro.

Mr Price (MRP) Annual Results for 52W Mar ’26 (17200c)

HEPS: 1453.9c (+2.1% from FY25)

EPS: 1449.5c (+2.3% from FY25)

Operating Profit: R6.0bn (+4.3%, normalised +8.0%)

Revenue: R42.7bn (+4.2% from FY25)

Gross Profit: Margin 41.2% (+70bps)

Dividend: 592.8c per share (final, payout ratio 63%): interim 323.2c for FY 916c total.

Retail sales grew 4.3% to R41.1bn, outperforming the RLC benchmark. Gross profit margin expanded to 41.2% despite a promotional environment. 196 new stores lifted trading space by 3.6%, with Power Fashion and Studio 88 contributing over R1bn operating profit. Online sales rose 4.9%, with 55% of orders collected in-store. CEO Mark Blair said: “The agility of our operating model and the strength of our value retailing DNA have enabled operating leverage in a challenging retail environment.” Outlook highlights resilience amid global inflationary pressures, with FY27 capex of R1.1bn planned for 180 new stores, revamps, and supply chain investment.

Comment: the solid results place the company on an 11.8X PE (at 17129c) and 5.3% DY which could normally call for a positive recommendation. Many SA foreign investing-debacle-weary investors are however, understandably, taking a wait and see attitude to the purchase of the NKD German discount chain.

Ninety One (NY1) Financial Results for FY26 (4633c)

HEPS: 17.5p (+2% from FY25)

EPS: 17.5p (+2% from FY25)

Operating Profit: £211.3m (+12% from FY25)

Revenue: £659.3m (+9% from FY25)

Dividend: 161c per share (final)

Assets under management rose 31% to £171.8bn, supported by net inflows of £2.8bn and the £18.3bn Sanlam transaction. Positive market and FX effects added £19.9bn. Equities and fixed income drove inflows, while South African multi-asset strategies saw outflows. Firm-wide one-year outperformance closed at 56%, with three-year at 69%Current page. CEO Hendrik du Toit stated: “Ninety One is a resilient and robust business with positive momentum. We are investing through the cycle in talent and technology to be future fit.”

Comment: apart from an upward blip to £144bn in FY21, assets under management languished around £130bn during FYs 20 to 25. Unsurprisingly the share price back in August 2020 was around where it is now. But with the move to £172bn expect some traction in FY27!

Trading Statements & Updates

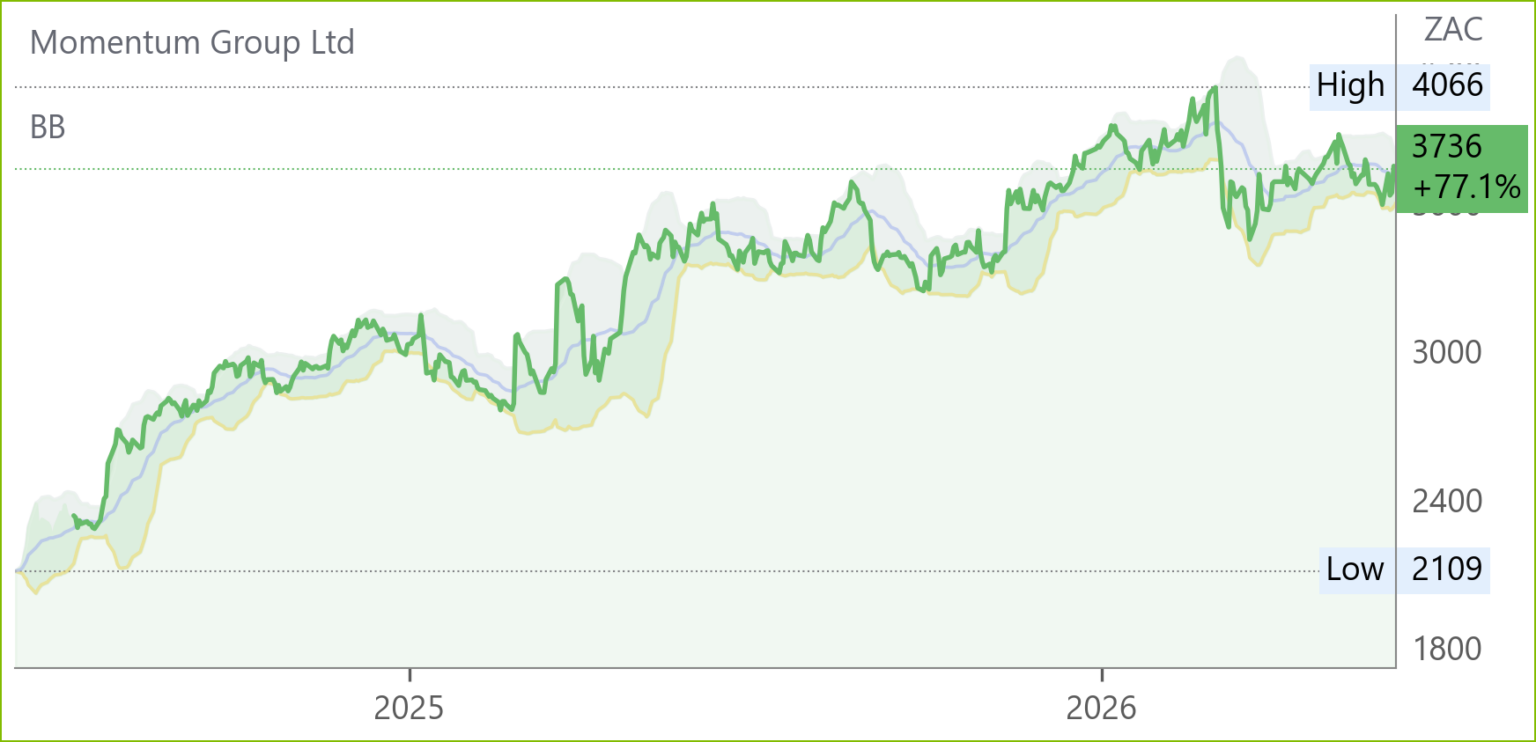

Momentum Metropolitan (MTM) Operating Update for 9M Mar ’26 (3736c)

HEPS: 414c (↑20% from 343c)

EPS: 401c (↑17% from 343c)

Operating Profit: Normalised headline earnings R5.54bn (↑15% from R4.83bn)

Revenue: PVNBP R66.9bn (↑15% from R58.0bn)

Dividend: Interim dividend already paid; no new declaration

Earnings growth was broad‑based, with Momentum Investments (+53%) benefiting from annuity profits and equity markets, Metropolitan Life (+21%) aided by mortality gains and expense discipline, and Africa (+60%) boosted by scheme wins in Botswana and Lesotho. Guardrisk (+16%) and Momentum Insure (+9%) delivered underwriting gains. New business volumes rose 15% to R66.9bn, though VNB fell 4% to R347m as margins contracted to 0.5% amid industry shift from life to living annuities. Solvency cover strengthened to 1.81x SCR, supported by statutory earnings and higher yields. A R1bn buyback was completed at an 18% discount to embedded value. Management highlighted resilience despite geopolitical and macroeconomic headwinds, with diversified earnings streams positioning the Group for sustainable growth.

SPAR (SPP) Trading Statement for 26W Mar ’26 (5100c)

HEPS: 174–217c (↓50–60% from 434c)

EPS: 140–180c (↓55–65% from 399c)

Operating Profit: Substantial decline due to KZN underperformance, elevated Black Friday spend, and debtor impairments

Revenue: Group +2.1% YoY; SA +1.7%; Ireland +2.4% (EUR)

Gross Profit: SA margin ↓20–40bps; Ireland margin ↑

Earnings fell sharply as SA Groceries & Liquor margins compressed, KZN logistics missteps raised costs, and debtor impairments increased. Ireland offset some weakness with stronger supplier terms and mix. Extraordinary impairments of R128m were recognised. Net debt rose on festive season working capital but covenants were met. UK disposal to A.F. Blakemore will streamline the footprint. Outlook focuses on KZN recovery, cost realignment, and strengthening retailer partnerships. Management expects benefits to build through H2 FY26, though fuel costs, debtor risk, and competition remain headwinds. Results due 10 Jun ’26.

Pan African Resources (PAN) Operational Update FY26 (2360c)

Operating Profit: Record operating cash flow, net cash position US$220m (vs net debt US$46.2m Dec ’25)

Gold production rose ~40% YoY to 275koz, driven by strong output at Elikhulu, Mogale Tailings and Evander, offsetting slower Tennant Mines ramp‑up. Evander underground delivered 47koz (+68% YoY) with grades >11g/t, while Barberton rose 5% to 72koz. Tennant Mines produced 34koz, with White Devil deposit expected to lift FY27 output to 48–52koz. Group AISC held at US$1,870/oz despite inflationary pressures. Net cash strengthened to US$220m after strategic investments. CEO Cobus Loots commented: “It has been an exceptional year, with record gold output and a robust balance sheet positioning us to expand production beyond 300koz.” FY27 guidance: 280–302koz at AISC US$2,075–2,175/oz. Results due 16 Sep ’26.

Optasia (OPA) Trading Update (1691c)

Trading momentum remained firm in Q1 FY26, though Nigerian airtime lending operations were paused in Apr ’26 due to regulatory changes. The FCCPC has since suspended these rules pending legal proceedings, with gradual recovery in transaction volumes expected. Optasia launched merchant loans for SMEs, expanding its AI‑driven platform, and progressed its deployment pipeline into new markets. CEO Salvador Anglada emphasised: “We remain focused on deepening partner relationships, expanding product coverage and driving geographic diversification.” AGM Resolution 3 regarding the election of Manuel Sánchez Rodríguez was withdrawn, with a replacement independent director to be appointed.

Snippets

Merafe (MRF) NERSA approved a negotiated electricity tariff of 62c/kWh for ferrochrome smelters, securing long‑term viability for the Glencore‑Merafe Chrome Venture. Following this, the Section 189 labour consultation process has been withdrawn, reducing retrenchment risk. Discussions with Eskom continue to finalise tariff terms, which remain critical for commercial sustainability. Stakeholder collaboration was acknowledged as instrumental in achieving this outcome.

Tencent’s (0700.HK) planned WeChat AI agent positions the company to catch up with rivals in generative AI, boosting investor confidence. Integration into its dominant social platform could unlock new revenue streams and strengthen engagement. The announcement underscores Tencent’s pivot towards AI‑native products, reinforcing its long‑term growth narrative and driving a sharp rally in its Hong Kong‑listed shares.

SPAR (SPP) reaffirmed governance integrity following media reports alleging VAT fraud. The Board clarified that the BDO review was a limited, single‑store due diligence, not a systemic audit, and no irregularities were raised by PwC. Complaints lodged by former store owner Amaan Sayed were linked to his rejected Guild membership application. Chairman Mike Bosman enjoys full Board support, with allegations deemed baseless.

Aveng (AEG) appointed Murray Leslie Coleman OAM as Independent Non‑executive Director, bringing over 35 years’ infrastructure and construction leadership experience from Lendlease and Macquarie Capital. He joins the Risk, Safety, Audit, and Tender Risk Committees. Chairman Philip Hourquebie will step down in Aug ’26, succeeded by Graeme Bevans, while Nicholas Bowen will retire. Board expressed confidence in strengthened governance.