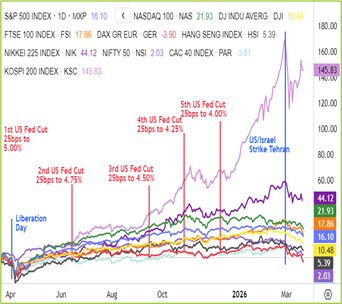

Global Indices

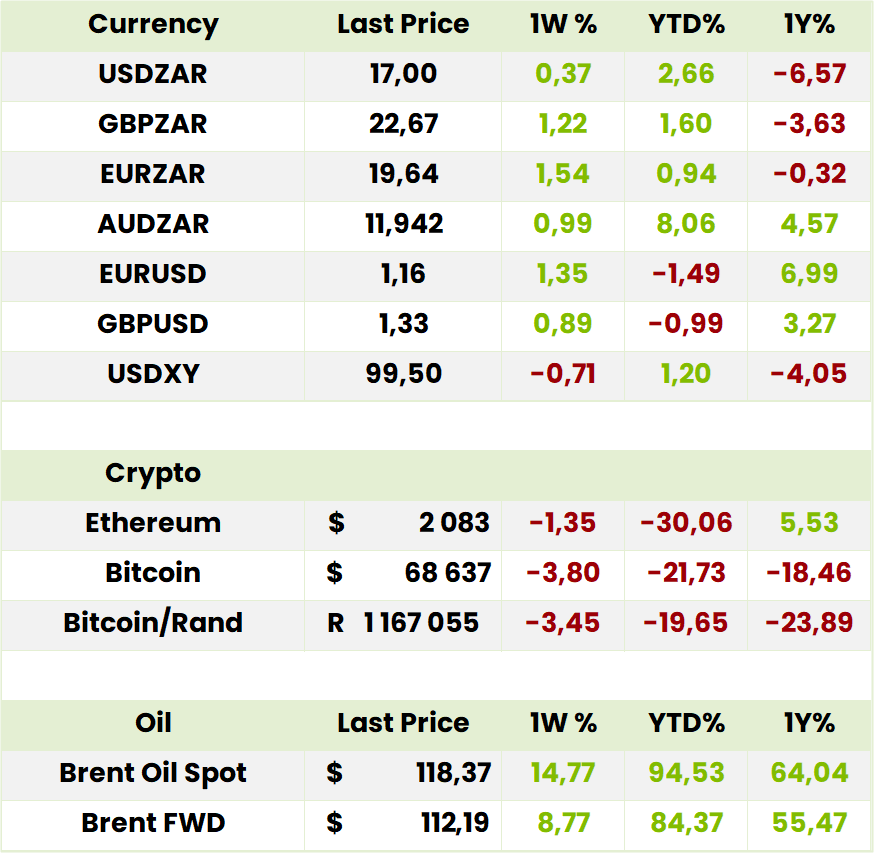

Currencies, Crypto & Commodities

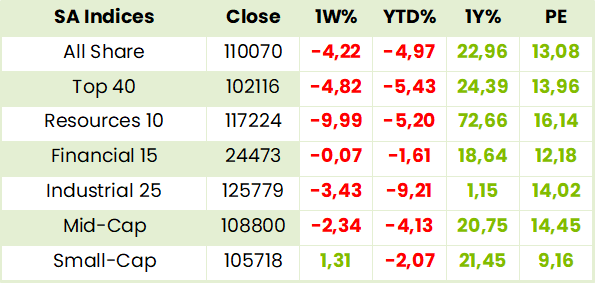

SA Indices

SA Upcoming Indicators & Dividends

Sun International* (SUI) Financial Results FY25 (4255c)

HEPS: 412c (+18% from FY24)

EPS: 405c (+17% from FY24)

Operating Profit: R2.1bn (+12%)

Revenue: R12.4bn (+9%)

Gross Profit: R6.8bn (+10%)

EBITDA: R3.5bn (+11%)

Dividend: 524c per share (interim was 172c; final ordinary 252c+ special 100c)

Sun International delivered strong growth across casinos, hotels, and online betting, with SunBet expanding rapidly. Improved occupancy and gaming revenues supported earnings, while debt reduction enhanced cash generation. Inflationary and power supply pressures were managed through cost discipline. “We are confident in sustaining momentum through diversified income streams and disciplined capital allocation.” – Ulrik Bengtsson, CEO. Outlook remains positive, with focus on digital gaming and hospitality asset optimisation.

Comment: much to the consternation of the retail industry and fiscus, lower LSMs are increasingly resorting to online gambling, seemingly out of desperation with indications that even those on the meagre state pension and NFSAS students’ allowances are joining in. With the casinos and slot machines seemingly now ex-growth, management has been pivoting to double its 4.2% share in this fast growing R50bn market, which is also expected to double, by 2030. To this end specialised management and technology are being deployed supported by the stable cash flows from casinos and hotels. Meanwhile, waiting for heps growth to pick up pace will be rewarded by the exceptional dividend yield (8.6% historic excluding the special and the share being cum the 352c final and special until 7 April)

MTN Group* (MTN) Financial Results FY25 (19832c)

HEPS: 1 050c (+22% from FY24)

EPS: 1 030c (+20% from FY24)

Operating Profit: R68bn (+15%)

Revenue: R210bn (+12%)

Gross Profit: R98bn (+14%)

EBITDA: R91bn (+13%)

Dividend: 330c per share (final)

MTN achieved double‑digit growth driven by data and fintech services, with subscriber expansion in Nigeria and South Africa. A R5bn share buyback was announced, reflecting confidence in cash flow. Fintech transactions surged, reinforcing Ambition 2025 strategy. Network modernisation and spectrum investments improved service quality. “We are accelerating our Ambition 2025 strategy, focusing on digital services and financial inclusion.” – Ralph Mupita, CEO. Outlook emphasises scaling fintech, strengthening infrastructure, and navigating regulatory challenges in key markets.

Comment: the stock has enjoyed a full recovery from the Nigerian economic travails induced losses of 2024. Adjusted Heps of 1359c places it on a 14.1x PE and Net Debt: ebitda has improved to 0.3xfrom 0.7x. Ironically, with Nigeria having contributed 33% to FY25 Ebitda and Ghana 24.9%. It is the former laggards that will continue to grow if the oil price remains elevated. Together with Uganda’s 9.8% and SA 17.9% these four African states contributed 86% of ebitda and the other 12 markets in which it operates 14%. With the SA market intensely competitive we think the stock if fully priced for now.

Momentum (MTM) Interim Results for 6M Dec ’25 (3570c)

HEPS: 274.4c (+13% from 243.6c)

EPS: 259.9c (+6% from 244.3c)

Operating Profit: R3.1bn (+10% from R2.8bn)

Revenue: R43.3bn (+11% from R38.9bn, PVNBP basis)

Dividend: 110c per share (interim, +29% from 85c)

Embedded Value: R44.55 per share (+13% from R39.29)

ROE: 24.0% (vs 24.6%)

Momentum delivered resilient earnings growth with NHE up 8% to R3.7bn, supported by strong underwriting in Guardrisk, Momentum Insure and Corporate, alongside improved profitability in Metropolitan Life. Retail earnings were impacted by yield curve shifts, while Africa operations turned profitable. A share buyback of 21.7m shares at R36.73 enhanced per-share metrics. CEO Jeanette Marais stated: “We remain committed to delivering value for our clients and stakeholders, maintaining sales growth and improving VNB outcomes.” – Jeanette Marais, Group CEO. Outlook highlights cautious optimism, with easing inflation and improved energy supply supporting growth, though unemployment and logistics remain constraints. Comment: the sprightly 29% increase in final dividend moved the total DPS to 200c or 40% of Normalised Headline Earnings, near the bottom of the target 40% to 60% range. Africa is profitable but far from moving the needle for Group results as is currently the case for India. Momentum has maintained its ROE at a commendable level of 20%. On a 7.4x PE and 5.6% DY the stock is fairly valued as it has enjoyed re-rating since successful implementation of the “Reset and grow” strategy of previous management so it can be held for long term growth.

Old Mutual* (OMU) Financial Results FY25 (1376c)

Old Mutual* (OMU) Financial Results FY25 (1446c)

HEPS: 256.3c (+8% from FY24)

EPS: 249.7c (+7% from FY24)

Operating Profit: R12.4bn (+6% from FY24)

Revenue: R198.6bn (+5% from FY24)

Gross Profit: R41.2bn (+4% from FY24)

EBITDA: R15.8bn (+9% from FY24)

Dividend: Final dividend of 56c per share declared (FY25 total dividend 93c, interim 37c)

Earnings growth was supported by premium expansion, stronger investment returns, and disciplined cost management. Digital adoption across customer channels accelerated, improving efficiency and client engagement. Capital strength remained resilient, with solvency comfortably above regulatory requirements. “We are confident in our ability to deliver sustainable value creation, supported by a resilient balance sheet and diversified earnings streams.”, CEO. Management anticipates continued growth in Africa, improved capital efficiency, and further progress in digital transformation initiatives. Comment: it’s been a long journey following the fruitless decades long foreign foray from the mid-nineties followed by the top management tussle with Peter Moyo’s short lived tenure as CEO in 2017 and subsequent stabilisation and consolidation under Iain Williamson. Under CEO Gerrie Strydom, however, it has at last laid the foundation for a coherent multi-faceted new growth strategy. With South Africa contributing 67.2% to Profit before tax, Southern Africa 29.6% and E. Africa 2.2%, it is decades behind Sanlam with its Africa-Allianz partnership and Discovery with its multiple sources of offshore earnings. Nevertheless, on a 5.3x PE and 6.8% dividend yield it will enjoy the benefits of a steady re-rating over the next five years.

Exxaro* (EXX) Financial Results FY25 (22000c)

HEPS: 3 247c (+8% from 3 016c)

EPS: 3 178c (-0.4% from 3 192c)

Operating Profit: R7.1bn (-7% from R7.6bn)

Revenue: R41.8bn (+3% from R40.7bn)

Dividend: 1 000c per share (final, +15% from 866c): interim was 843c so 1843 for FY25.

Exxaro’s FY25 performance reflected resilient revenue growth despite weaker coal demand and lower operating profit. HEPS rose 8% on cost discipline, while EPS was marginally lower. The group declared a final dividend of 1 000c per share, payable 11 May ’26. Non-financial highlights included progress on renewable energy investments and continued focus on decarbonisation. Chairperson Mvuleni Geoff Qhena noted: “Exxaro remains committed to sustainable value creation, balancing shareholder returns with investment in energy transition.” – Mvuleni Geoff Qhena, Chairperson. Outlook points to cautious optimism, with diversification into clean energy expected to offset coal market volatility.

Comment: The manganese acquisition from Ntsimbintle Holdings marks a meaningful step in Exxaro’s diversification strategy, reducing long‑term reliance on coal while adding exposure to structurally attractive transition metals (manganese is critical in steel production). Combined with a strong safety record, 40 fatality‑free months, and a disciplined capital allocation framework supporting consistent dividends for the past 20 years, Exxaro remains a well-positioned, income‑generating core holding despite sustained downward pressure on coal prices over the last 3 years. Notably, the war in Iran has caused an upward spike in coal futures prices. Although this has provided meaningful gains to the share price this is neither reflecting the benefits of a possibly prolonged period of high coal prices nor the additional earnings to come in due course from manganese. So, on a 8.3% and 6.8x PE the stock is undervalued.

Optasia (OPA) Audited Annual Results FY25 (1970c)

HEPS: 3.38c (+9% from FY24)

EPS: 3.38c (+9% from FY24)

Normalised EPS: 4.64c (+48% from FY24)

Operating Profit: $114.5m (+52%)

Revenue: $265.4m (+76%)

EBITDA: $114.5m (+52%)

Optasia (Channel VAS Investments) delivered exceptional FY25 growth, with micro‑financing overtaking airtime credit as the largest revenue contributor. Service users rose 43% to 432m, distributed value increased 44% to $5.5bn, and revenue surged 76% to $265.4m. EBITDA grew 52% to $114.5m, while net income rose 57% to $57.8m. The JSE listing in Nov ’25 and FirstRand’s strategic stake marked key milestones, strengthening capital structure and credibility. “2025 was a milestone year… the listing enhance ZARs our visibility and credibility as a leading global fintech.” – Salvador Anglada, CEO. Outlook highlights geographic expansion, AI‑driven credit scoring, and product innovation, with ambitions for sustained low‑to‑mid‑20s growth across revenue and earnings.

Comment: the 48% increase in normalised EPS to USD 4.64c at ZAR 16.89/$ makes for a normalised ZAR EPS of 78.4x and a 25.4x PE. Metrics include: net debt to adjusted ebitda ratio 0.11; adjusted EBITDA margin of 43.2%; normalised net income margin of 21.8%; default rate 1.2%. FY 26 IPO guidance for revenue growth and adjusted ebitda growth have both been nudged up to 30%, net income growth maintained at 40% and capex maintained at 6% of revenues. Of the 38 countries in which Optasia operates only 6 are in the Middle East and Iran is not one of them. Given the guidance for ongoing growth and strong metrics we maintain our BUY recommendation.

IOCO (IOC) Interim Results for 6M Jan 26 (413c)

Revenue: R2.4bn (+18% from 6M Jan 25c)

Operating Profit: R310m (+22% from 6M Jan 25)

HEPS: 35c (+20% from 6M Jan 25)

EPS: 34c (+19% from 6M Jan 25)

IOCO’s growth was underpinned by strong demand for cloud migration, cybersecurity, and digital transformation services. Expansion into African markets added resilience, while contract renewals with key clients boosted recurring revenue. Management highlighted investment in AI-driven solutions as a differentiator. Outlook guidance points to sustained double-digit growth.

Stadio (SDO) Financial Results FY25 (1140c)

HEPS: 38.5c (+23% from FY24)

EPS: 38.6c (+25% from FY24)

Operating Profit: R341m (+24% from FY24)

Revenue: R1.8bn (+14% from FY24)

EBITDA: R553m (+21% from FY24)

Dividend: Final dividend of 18.4c per share declared (FY25 total dividend 18.4c)

NAV: 245c per share (+6% from FY24)

Student enrolments rose 9% in Semester 1 and 7% in Semester 2, driving revenue growth. Strong cash generation enabled a share repurchase of 6.9m shares worth R75.7m, immediately cancelled to limit dilution. Management reaffirmed its pre-listing ambition of 56,000 students by 2026, with a longer-term target of 80,000 students by 2030. “We are well positioned to deliver consistent growth, supported by robust demand for quality education and disciplined capital allocation.” – Chris Vorster, CEO.

Outlook: Expansion plans remain on track, with focus on scaling student numbers and enhancing digital learning platforms.

Comparable JSE peers in education: Curro (COH) now delisted, AdvTech (ADH)

Comment: management is already targeting 100000 students after 2030, more campuses and university status as soon as regulations permit. In addition, CEO Vorster is contemplating artisanal training and “short training” but also expects to announce “new and exciting developments” later this year. With Phase 2 of the Durbanville Campus due for completion in August 2026 and Phase 3 to come after that, Stadio has a strong balance sheet (Debt R120m and Shareholders Equity of R2.1bn) to cope with the capex currently envisaged of R294m. On a 29.5x PE Stadio is currently pricing in a CAGR well above 20% and while holders should certainly stay aboard, other investors should take advantage of any geopolitically induced price retracements.

Trading Statements & Updates

Remgro* (REM) Trading Statement for 6M Dec ’25 (18593c)

HEPS: 914c–948c (↑36%–41% from 672c)

Headline earnings are expected to rise sharply, driven by improved operational performances across most investee companies. The uplift reflects stronger contributions from healthcare, consumer, and financial services holdings, with diversified exposure supporting resilience despite macroeconomic headwinds. Management noted that more detail will be provided in the full results release. “Remgro continues to benefit from the operational improvements of its investee companies, reinforcing our commitment to sustainable shareholder value.” – Jannie Durand, CEO. Results due 25 Mar ’26.

Foschini (TFG) Trading Statement for FY26 (6850c)

HEPS: Expected decline >20% (vs FY25)

EPS: Expected decline >20% (vs FY25)

Revenue: Africa +5.2% YTD; London +31.0% YTD (incl. White Stuff); Australia -1.4% YTD

Gross Profit Margins normalised since Jan but remain below FY25 peak season levels

Sales growth in Africa (+7.6% Q4 to date) was supported by online and value-added revenues, while London benefited from White Stuff acquisition. Australia remained weak. Elevated input costs and cautious consumer behaviour weigh on outlook, though local manufacturing and cost discipline provide resilience. “Our diversification and operational efficiencies will help us navigate geopolitical uncertainty while maintaining a sound balance sheet.” – TFG Management. Results due 5 Jun ‘26

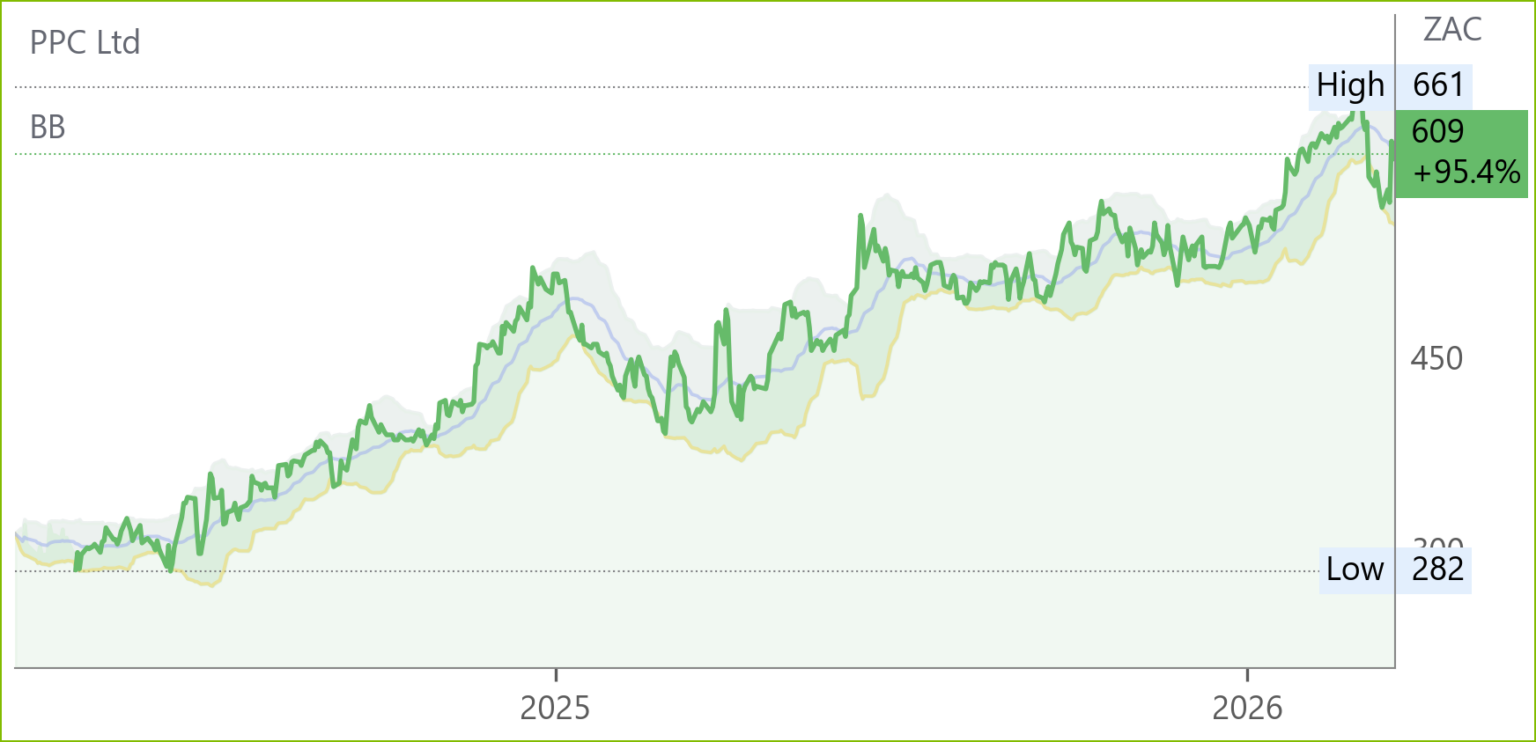

PPC (PPC) Operational Update for 10M FY26 (605c)

Revenue: R7.8bn (+6% from 10M FY25)

EBITDA: R1.2bn (+12% from 10M FY25)

Operating Profit: R950m (+10% from 10M FY25)

HEPS: 45c (+15% from 10M FY25)

EPS: 44c (+14% from 10M FY25)

Outlook: Cement demand in SA and Zimbabwe improved, supported by infrastructure projects. CEO Roland van Wijnen stated, “We are seeing encouraging momentum in regional demand, and remain focused on cost discipline and debt reduction.”

Astral Foods (ARL) Voluntary Trading Update FY26 (24869c)

Revenue: R9.5bn (+52% from FY25)

Operating Profit: R1.1bn (+60% from FY25)

Gross Profit: R2.8bn (+55% from FY25)

HEPS: 1,200c (+58% from FY25)

EPS: 1,210c (+59% from FY25)

Dividend: 400cps (interim)

Astral’s turnaround was driven by easing feed costs, improved poultry margins, and operational efficiencies across its production facilities. The company benefited from stabilised electricity supply and reduced diesel usage, which lowered input volatility. CEO Chris Schutte stated, “Operational efficiencies and easing input costs have restored profitability, positioning us strongly for the year ahead.”

Snippets

Labat Africa (LAB) announced that its subsidiary Ahnamu Investments has signed a five‑year global supply agreement with Dubai‑based Shafi Inc FZCO. The deal positions Ahnamu as an African supplier of advanced semiconductor and AI computing hardware into Shafi’s international distribution channels. Following Labat’s 51% acquisition of Ahnamu, the agreement marks a strategic pivot into ICT, enhancing revenue visibility and global reach.

Vukile (VKE) acquired a 50% stake in Splau Shopping Centre, Barcelona, strengthening its European retail portfolio. The deal diversifies income streams and enhances exposure to stable euro-denominated rentals. Management emphasised the strategic fit with existing assets and highlighted the centre’s strong tenant mix and footfall. The acquisition supports long-term growth and balance sheet resilience.

Woolworths (WHL) announced a voluntary acquisition of 100% of in2food Holdings, a leading supplier of prepared foods. The deal strengthens Woolworths’ vertically integrated food supply chain, enhancing innovation and quality control. Management highlighted strategic alignment with its premium food offering and growth ambitions. The acquisition is expected to improve efficiencies, broaden product capabilities, and support long‑term shareholder value creation.

SPAR (SPP) announced a voluntary operational update, introducing a severance programme in selected areas to reset its cost base and align with current trading conditions. The initiative aims to improve efficiency and competitiveness without affecting retailers or services to its independent network. Management emphasised strengthening operational performance and ensuring the group is structured for sustainable growth.

South32 (S32) placed its Mozal Aluminium smelter in Mozambique on care and maintenance from 15 Mar ’26 after failing to secure affordable power supply beyond that date. One‑off costs are estimated at US$60m, with ongoing annual care and maintenance costs of US$5m. Alumina from Worsley will now be sold to third parties. “While this is not the outcome we wanted, we are proud of Mozal’s 25‑year contribution to the local community and economy.” – Graham Kerr, CEO.