Finova Investor Digest

Global Indices

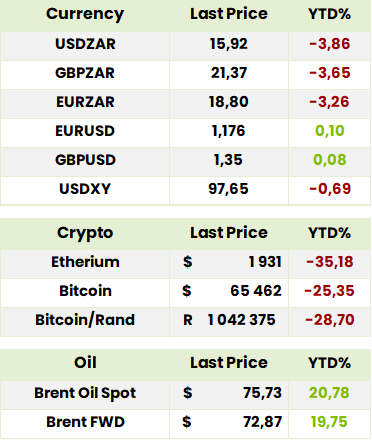

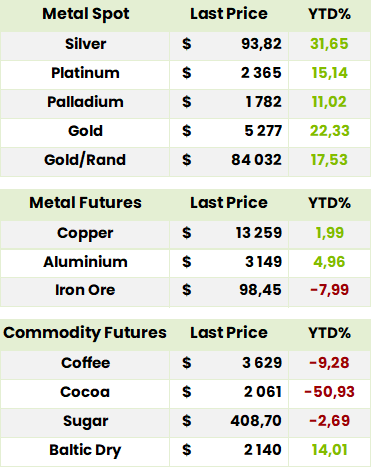

Currency, Crypto & Commodities

SA Indices

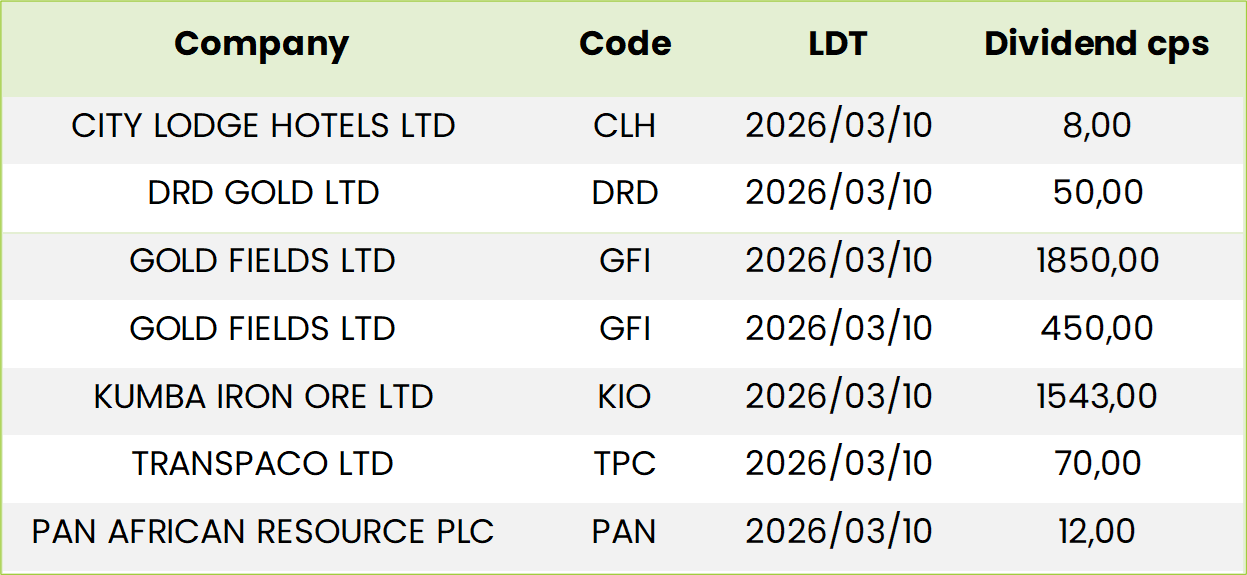

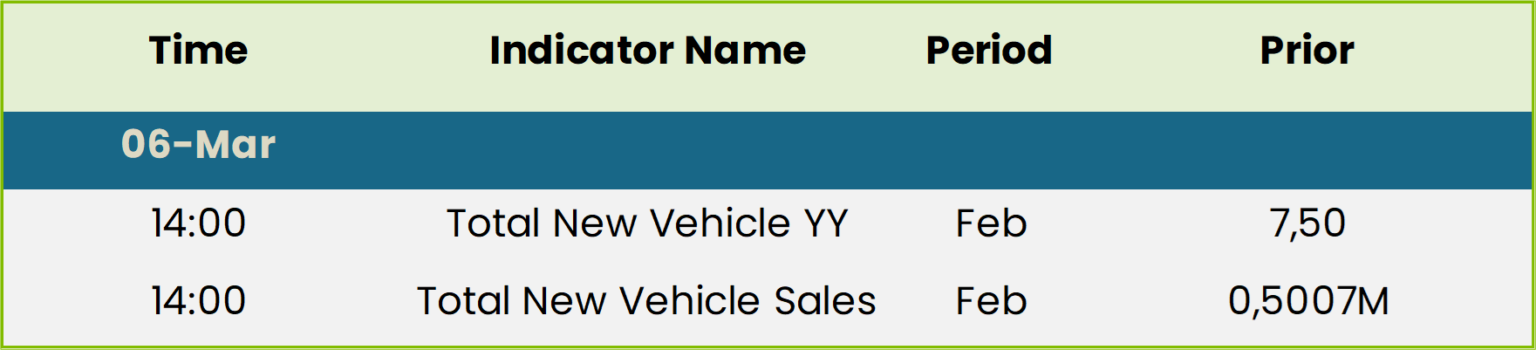

SA Upcoming Indicators & Dividends

SA Equity

*Denotes companies held in the Finova Flagship Portfolio and/or the Finova Retirement Portfolio

AngloGold Ashanti* (ANG) Financial Results FY25 (200789c)

– HEPS:537c (↑143% from 221c in FY24)

– EPS:519c (↑123% from 233c in FY24)

– Operating Profit: $4.3bn (↑156% from $1.7bn in FY24)

– Revenue: $9.7bn (↑72% from $5.7bn in FY24)

– Gross Profit: $4.9bn (↑136% from $2.1bn in FY24)

– EBITDA: $6.3bn (↑129% from $2.7bn in FY24)

– Dividend: 357cps (record $1.8bn declared for FY25)

Gold production rose 16% to 3.1Moz, supported by Sukari’s integration and stronger output at Obuasi and Siguiri. Free cash flow tripled to $2.9bn, while net cash improved to $879m, the strongest balance sheet in company history. Mineral reserves increased 17% to 36.5Moz, underpinned by exploration success and the first Merlin reserve at the Arthur Gold Project. Safety performance reached record lows in TRIFR. “We delivered growth and kept costs flat in real terms, which translated into record earnings, cash flow and dividends.” – Alberto Calderon, CEO.

Comment: Anglogold’s 6 Tier One assets produced 2139moz in FY25 and four of them are in Africa with Obuasi in Ghana, Geita in Tanzania.

Kibali (45% owned) in DRC and Sukari in Egypt. Cuiaba and Tropicana are in Brazil and Australia. The Tier 2 assets produced 899koz and comprise Siguiri in Guinea, Iduapriem in Ghana, Tropicana and Sunrise Dam in Australia and Cerro Vanguardia in Argentina. Their average AISC was $2040oz as against $1456oz for Tier One. For FY 26 management is guiding for production of 2800 -3170koz and, for FY27, 2850 -3220koz While most of the mines have significant growth potential, CEO Calderon is particularly optimistic about growing the reserves of the Arthur project in Nevada which is said to be one of the largest greenfields discoveries of the century in the US. Anglogold has a sound portfolio of assets which will enable it to maintain its policy of paying dividends equal to half free cash flow at the same time as growing reserves and production.

Valterra Platinum* (VAL) Financial Results for FY25 (186439c)

– HEPS: 6,348c (↑98% from 3,205c)

– EPS: 5,872c (↑119% from 2,683c)

– Operating Profit: R15.4bn (↑117% from R7.1bn)

– Revenue: R116.3bn (↑7% from R109bn)

– Gross Profit: Not disclosed

– EBITDA: R33.4bn (↑68% from R19.8bn)

– Dividend: 4,500c per share (↓37% from 7,175c)

HEPS nearly doubled, while EPS rose 119%, reflecting strong EBITDA growth from higher PGM basket prices and cost savings. Dividend payout fell 37% despite robust cash generation.

Valterra Platinum marked its first year post-demerger from Anglo American with strong operational and financial delivery. PGM production of 3.2m ounces was marginally above guidance, despite flooding at Amandelbult. EBITDA surged 68% to R33.4bn, supported by higher basket prices and R5bn in cost savings. Net cash recovered to R11.5bn, enabling a R45 per share dividend, including a special payout. Sustainability milestones included IRMA certification across all operations. “2025 was a defining year, with momentum, clarity and an unwavering focus on value creation for all stakeholders.” – Craig Miller, CEO.

Comment: the share price has understandably reacted, not only to pgm prices which have more than doubled from the levels below $1000/oz at which Platinum, for example, traded for years until around April 2025, but also to the announcement of major cost reductions under way as well new systems in place at all levels. These will also lead to substantial reductions in previously guided capex levels all of which bode well for healthy dividend payouts. CEO Craig Miller has for years been correct in forecasting pgm price strength and continues to do so. Should the current correction in pgm prices continue, investors would do well to add to holdings for the longer term.

Northam Platinum* (NPH) Interim Results for 6M Dec 25 (43335c)

– HEPS: 1 524.0c (>1 000% from 61.1c)

– EPS: 2 006.0c (>1 000% from 61.5c)

– Operating Profit: R5.84bn (+439.2% from R1.08bn)

– Revenue: R23.25bn (+60.0% from R14.53bn)

– Gross Profit: Not disclosed

– EBITDA: R7.45bn (+322.9% from R1.76bn)

– Dividend: 700.0c interim (vs 15.0c Dec 24)

Revenue surged 60% on stronger PGM basket prices and higher sales volumes, driving EBITDA and operating profit growth above 300%. EPS and HEPS exceeded 1 500c, reflecting exceptional profitability. A record interim dividend of 700c per share was declared, amounting to R2.8bn. CEO Paul Dunne noted: “Northam has delivered a step-change in earnings, underpinned by operational resilience and disciplined capital allocation.” Outlook highlights sustained demand for PGMs and continued focus on balance sheet strength.

Comment: the recent increase in revolving credit facilities from R2bn to R13.3bn mainly for solar photovoltaic plant and battery storage further ensures that balance sheet strength will be the least of Northam’s challenges. The 47% ramp up in production at Eland helped nudge 1H26 pgm production up 3.7% as the company heads for 910 to 930 moz for FY26. The gap in rating between it and sector leader Valterra is in our view overdone making Northam a Buy for anyone without a position in pgms.

Aveng* (AEG) Interim Results for 6M Dec ’25 (460c)

– HEPS: 3c (vs -309c Dec ’24)

– EPS: -13c (vs -293c Dec ’24)

– Operating Profit: R107m (vs -R356m Dec ’24)

– Revenue: R14.2bn (-14% from R16.6bn Dec ’24)

– Gross Profit: R791m (+107% from R383m Dec ’24)

Revenue contracted on weaker infrastructure markets in Australia and New Zealand, but gross margin strengthened to 5.6% from 2.7%. Losses narrowed significantly, supported by strong Building and New Zealand operations. Cash rose to R3.4bn, with net cash at R2.8bn, while work in hand expanded to R38.6bn, driven by water, wastewater, and transport projects. McConnell Dowell will be retained, with risk-controlled growth prioritised, while Moolmans is under new leadership to resolve the unsustainable Tshipi contract. “Our commitment to ensuring the success of our three businesses remains unwavering and in line with the objective of ensuring a sustainable future for each.” – David Simpson, Interim CEO.

Comment: although the broader recovery is definitely under way with an encouraging outlook for infrastructure in New Zealand and the Pacific Islands the pace has been dogged by persistent issues in Mining, with Moolmans’ Tshipi contract as well, in the Infrastructural Division, with the Kidston Pumped Storage project in Queensland and the Jurong Regional Line project in SE Asia. The FY 25 operating loss before capital items of A$9.4bn (FY24 -$31bn) illustrates both the reasons for disappointment as well as turnaround potential. Building improved from A$9.2bn to AS23.2bn but Aveng infrastructure went from -A$26.5bn to a still negative -A$4.7bn and Mining from A$1.4bn to a mere A$0.2bn. Aveng Legacy cost still lingered at A$2.2bn (FY24 A$2.4bn) while Aveng Corporate, at A$8.0 bn, albeit down from A$12.7bn, still seems high. We believe the persistence of these challenges raises issues of management and it remains to be seen whether the yet to be appointed permanent CEO resolves them. Meanwhile, the tunaround potential remains substantial but, while this justifies a HOLD, we think other investors could afford to await further progress.

Sasol* (SOL) Interim Results for 6M Dec ’25 (14531c)

– HEPS: 927c (↓34% from 1413c)

– EPS: 38c (↓95% from 722c)

– Operating Profit: R4.6bn (↓52% from R9.5bn)

– Revenue: R122.4bn (flat y/y)

– EBITDA: R21.0bn (↓12% from R23.9bn)

Turnover was flat at R122.4bn, supported by 3% higher sales volumes, but weaker oil and chemical prices weighed on earnings. Secunda production volumes rose 10%, while disciplined cost control improved free cash flow to R0.8bn (first positive in four years). EPS collapsed 95% due to impairments, while HEPS fell 34%. “We are showing consistent progress in the implementation of our strategic initiatives…building resilience for the future.” – Simon Baloyi, CEO. FY Results due Jun ’26.

Comment: management confirmed that the Capital Markets Day strategy was on track and, as far as the recent geopolitically driven spurt in oil price is concerned, a hedging programme was in full swing. Apart from the fact that the Iranian attacks are in full swing which will benefit Sasol, possibly for a prolonged period, the long term case for investment, based on the successful implementation of long term strategy, remains in place.

AECI (AFE) Financial Results for FY25 (10970c)

– HEPS: 1,098c (↑53% from 718c)

– EPS: 357c (↑36% from 263c)

– Operating Profit: R1.53bn (↓1% from R1.55bn)

– Revenue: R32.18bn (↓4% from R33.5bn)

– Gross Profit: Not disclosed

– EBITDA: R3.41bn (↑12% from R3.05bn)

– Dividend: 228c per share (final 128c, ↓42% from 219c)

HEPS rose 53% while EPS increased only 36%, reflecting impairments excluded from headline earnings. EBITDA grew 12% despite revenue declining 4%, driven by AECI Mining’s record margins.

AECI delivered stronger profitability despite softer revenue, supported by disciplined pricing and margin management. AECI Mining achieved record EBITDA of R2.7bn with margins at 15%, while Chemicals generated robust free cash flow. Net debt fell sharply to R465m after R2.2bn in asset disposals, improving gearing to 4%. Safety performance improved significantly, with TRIR down 35% and no fatalities. “I am encouraged by the outstanding progress being made across the Group as we strengthen our position for long-term success.” – Interim Group CEO.

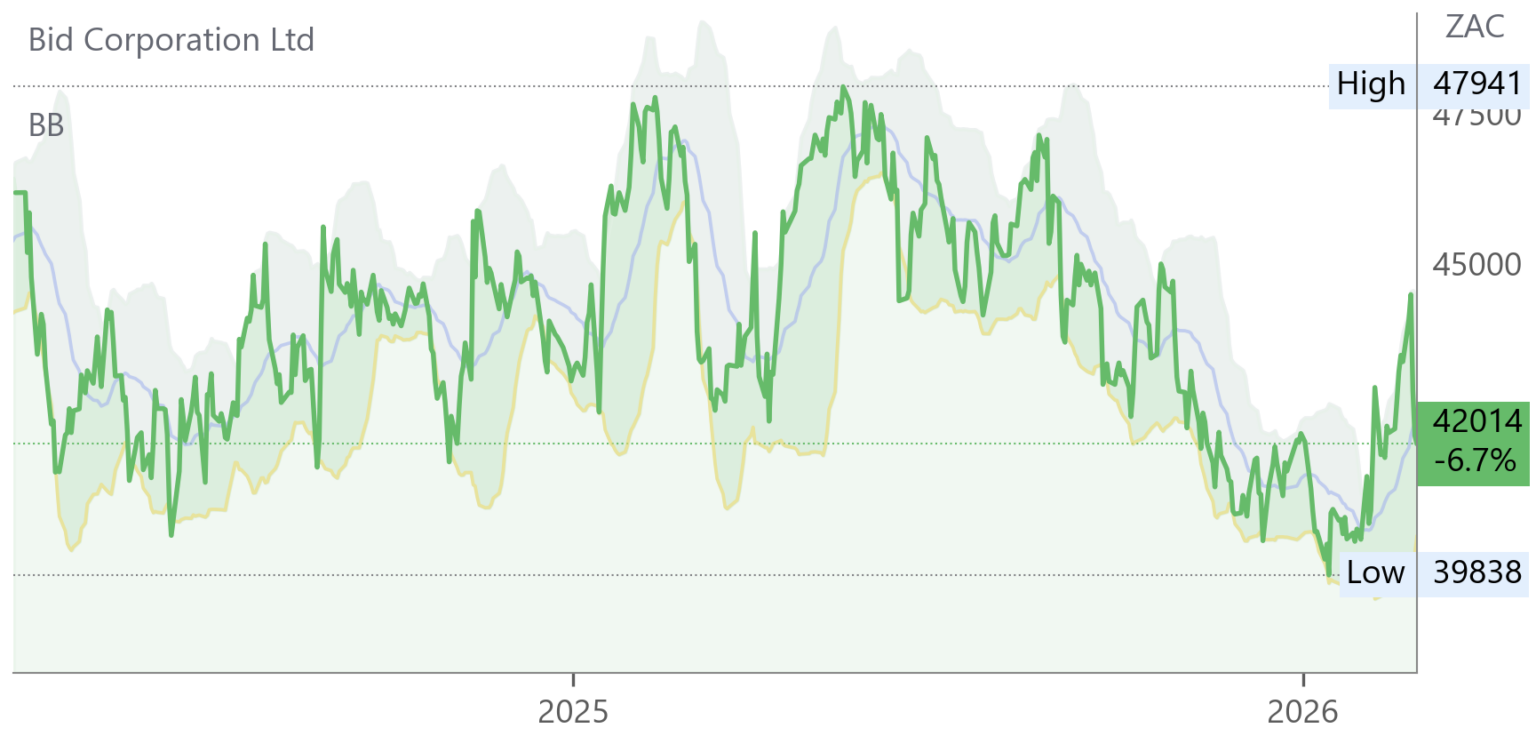

Bidcorp* (BID) Interim Results for 6M Dec ’25 (42014c)

– HEPS: 1,325c (↑8.5% from 1,221c)

– EPS: 1,306c (↑16.6% from 1,120c)

– Operating Profit: R6.8bn (↑8.1% from R6.3bn)

– Revenue: R126.3bn (↑7.1% from R118bn)

– Dividend: 615c interim dividend (↑9.8% from 560c)

EPS rose faster than HEPS due to fewer non-recurring adjustments. Revenue grew 7.1% despite global uncertainty, while trading profit increased 8.1%.

Bidcorp delivered resilient growth in a volatile global foodservice market, supported by decentralised operations and strong digital commerce adoption. Cash generation rose 27% to R6.8bn, enabling a higher interim dividend. Expansion was driven by bolt-on acquisitions and organic growth across 31 countries. ESG integration and balance sheet conservatism remain central to strategy. “Our proven and scalable business model continues to deliver value in challenging conditions, positioning Bidcorp for sustainable growth.” – Group statement.

Comment: CEO Bernard Berson reminded analysts that because the group, which operates in over 35 countries over five continents, was so widespread it was very unlikely that there would be dramatic changes from one reporting period to another. It was also unlikely to alter the business model by, for example, “trading down” to cater for consumers when they were, as in many countries now, experiencing financial pressure. The fact that the model was nevertheless continuing to succeed, proved the validity of this strategy. By the same token, however, profits were geared to any improvement in economic conditions such as lower interest rates. The company maintains the boring consistency that Buffet liked and warrants a place in any long term portfolio requiring global diversification.

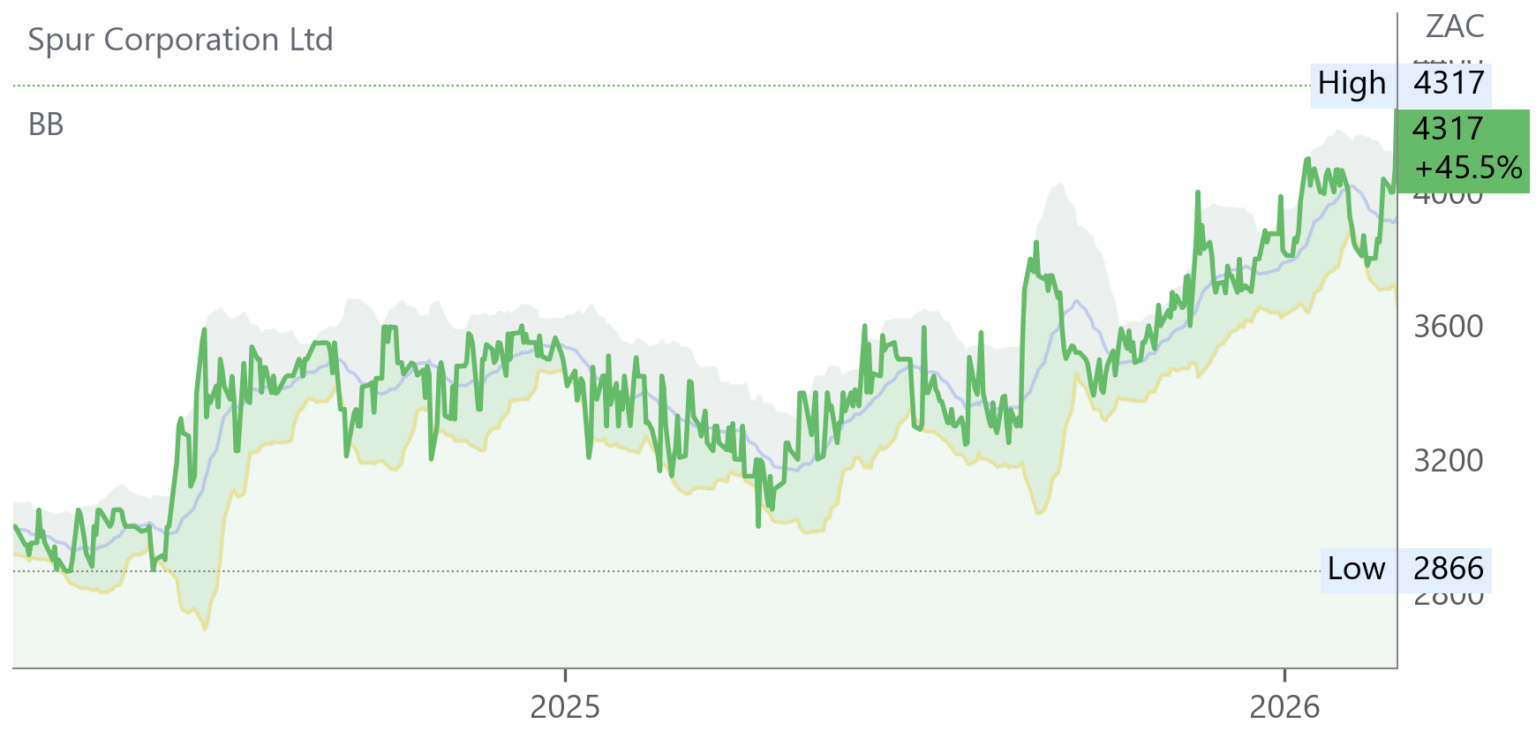

Spur (SUR) Interim Results for 6M Dec ’25 (4317c)

– HEPS: 202.57c (+13.6% from 178.3c)

– EPS: 203.61c (+13.9% from 178.7c)

– Operating Profit: R244.7m (+13% from R216.6m)

– Revenue: R2.2bn (+8.5% from R2.0bn)

– Dividend: 120c per share (interim, +13.2% from 106c)

Franchised restaurant turnovers rose 8% to R6.4bn, supported by new openings (29 in SA, 9 internationally) and 29 revamps. Cash generated from operations increased 21.1% to R217.5m, though cash balances declined due to share repurchases and higher dividends. Vuyokazi Henda was appointed executive director, strengthening marketing leadership.

Outlook stresses expansion with 42 new SA restaurants and 14 international openings planned for FY26. “Spur is well positioned to gain market share by offering distinctive dining experiences across categories and regions.” – Mike Bosman, Chairman.

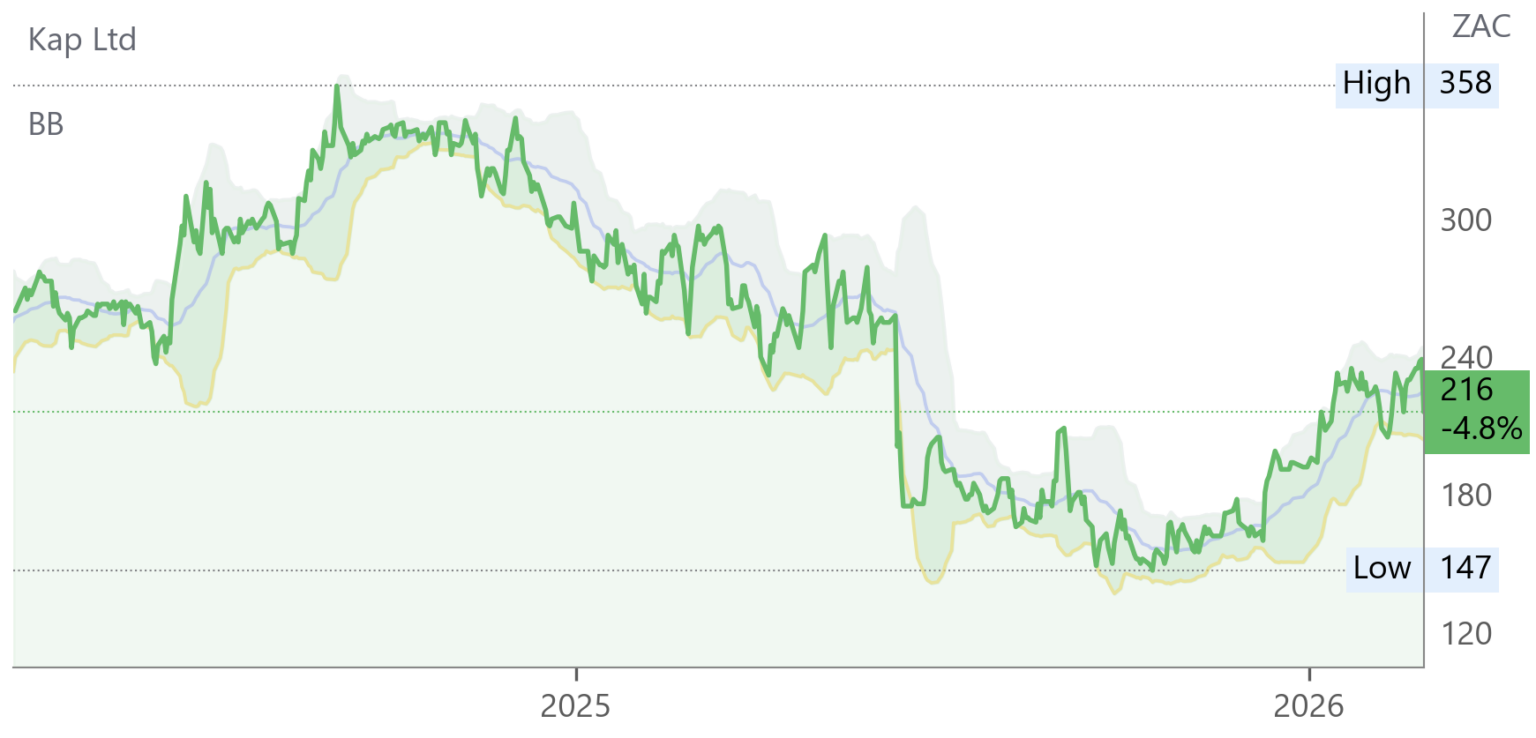

KAP (KAP) Interim Results for 6M Dec 25 (216c)

– HEPS: 22.7c (+32% from 17.2c)

– EPS: 20.8c (+28% from 16.2c)

– Operating Profit: R1 264m (+10% from R1 153m)

Revenue: R14 872m (-3% from R15 355m) softened due to weaker demand in certain segments, but operating profit rose on improved efficiencies. HEPS growth outpaced EPS by >30%, reflecting stronger underlying performance. Net asset value per share dipped slightly to 513c. Management maintained its conservative dividend stance, prioritising balance sheet strength. Results webcast scheduled for 26 Feb ’26.

Operating Updates & Trading Statements

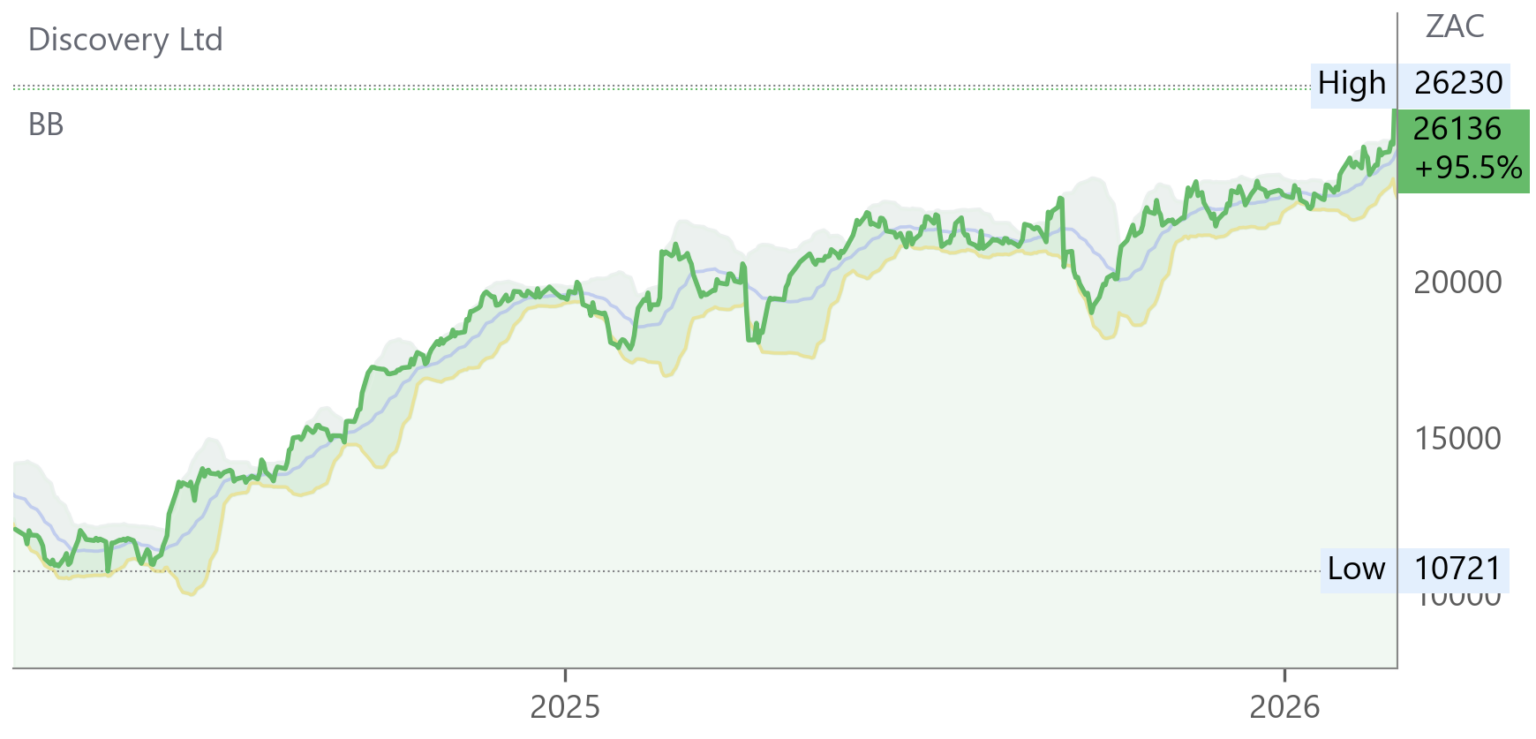

Discovery* (DSY) Operational Update & Trading Statement for 6M Dec ’25 (26136c)

– HEPS: 834–867c (+25–30% from 667c)

– EPS: 827–860c (+25–30% from 661c)

– Normalised HEPS: 843–877c (+24–29% from 680c)

– Operating Profit: +22–27% YoY

Discovery reported strong growth across all composites, with Discovery Bank turning profitable (R210–230m vs prior loss), Discovery Health absorbing a R125m concession while expanding new business, and Discovery Insure delivering margin gains. VitalityHealth nearly doubled operating profit, while Ping An Health benefited from equity market returns despite distribution changes.

Outlook emphasises scaling the Shared-value model and leveraging new partnerships. “Discovery is well positioned to deliver sustainable growth, supported by disciplined execution and innovation.” – Adrian Gore, Group CEO. Results due 3 Mar ’26.

SPAR* (SPP) Trading Update for 18W to Jan ’26 (6980c)

– Revenue: +2.1% y/y

– Gross Profit: Declined (Southern Africa margins under pressure)

Black Friday promotions squeezed profit margins in a challenging market with low food inflation, and are now faced with a R169m lawsuit from a prominent KZN family. SAP system headaches persist and to add to woes CEO Angelo Swartz resigned last week. Southern Africa turnover up 0.9% and Ireland +6.1%. SPAR Health grew strongly (+23%), while Build-it fell (-2.4%). Disposal of UK operations (AWG) is progressing without further impairments or cash injections. Management expects margin recovery in H2 FY26 as corrective actions embed. “Management’s focus remains firmly on the accelerated execution of margin restoration initiatives, balance sheet resilience and operational stability across the network.” – Board statement. Results due 10 Jun ’26

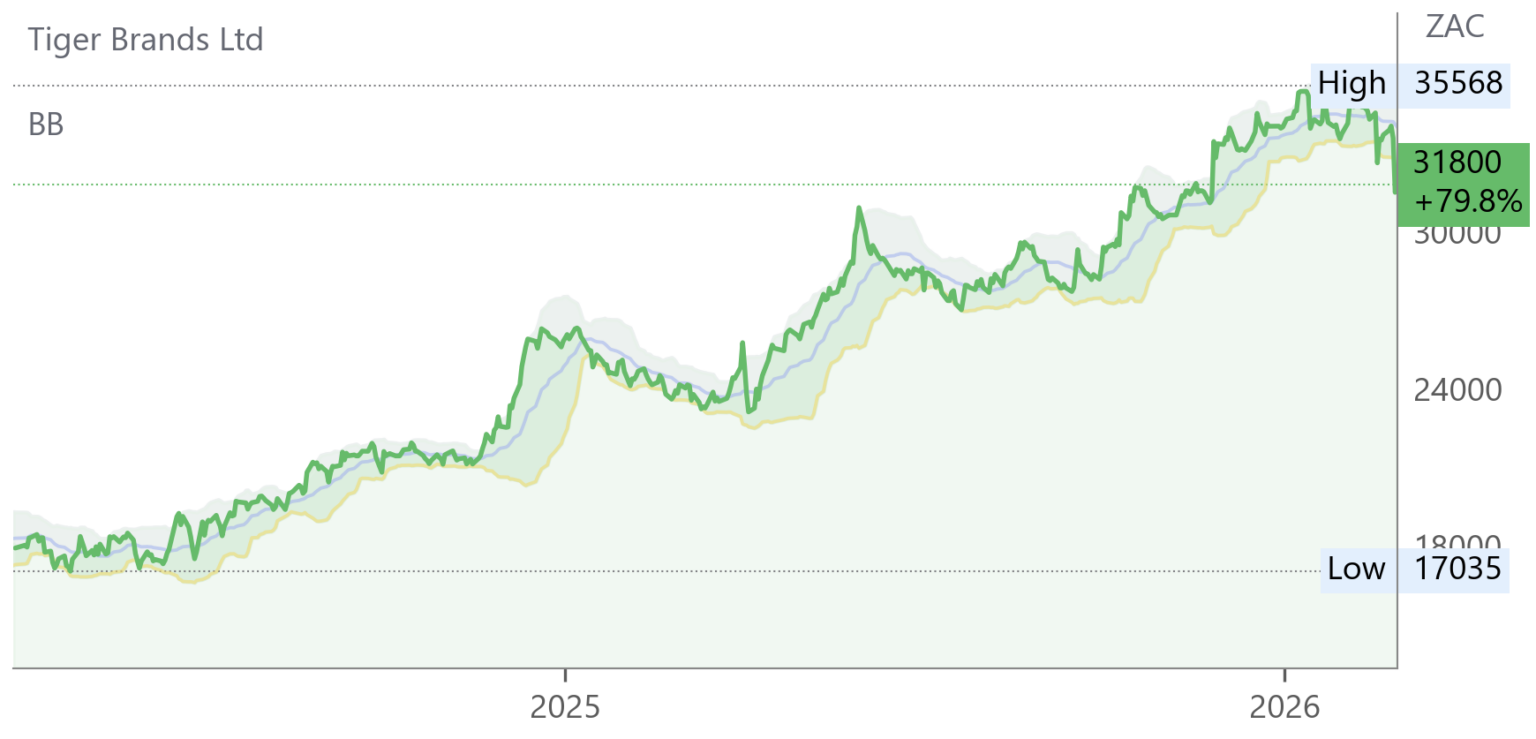

Tiger Brands (TBS) Trading Update for 4M to Jan ’26 (31800c)

Revenue from continuing operations rose 1%, supported by 2% volume growth, offset by 1% price deflation. Adjusted revenue grew 2% with strong gains in Culinary and Milling & Baking, while Personal Care remained under pressure. Operating profit improved, maintaining a double-digit margin through efficiency and logistics optimisation. Portfolio optimisation advanced with completion of Randfontein operations disposal and pending Chococam sale. Engagements continue on the listeriosis class action, with adequate insurance cover in place.

Outlook highlights focus on portfolio shaping, cost leadership, and brand rejuvenation. “Tiger Brands is well positioned to ensure continued performance delivery against this backdrop, driven by relentless focus on execution.” – Noel Doyle, CEO. Results due 1 Jun ’26.

Grindrod* (GND) Trading Statement FY25 (1860c)

HEPS: 176.1c–183.6c (>100% from 46.7c)

EPS: 306.3c–313.8c (>100% from 47.1c)

Earnings surged on one-off net profits of R902.8m from forex translation reserves linked to the Matola terminal buy-up and marine fuel JV exit. Core HEPS rose 15%–20% to 172.8c–180.3c, supported by record throughput at Matola (9.9mtpa) and Maputo (15.2mtpa). Results due 6 Mar ’26.

Metair (MTA) Trading Statement for FY25 (479c)

HEPS: 185c–195c (+76% to +86% from 105c)

EPS: 28c–35c (–82% to –77% from 155c)

Operating Profit (EBIT): R1.07bn–R1.11bn (+96% to +103% from R546m)

Revenue: R17.4bn–R17.9bn (+53% to +58% from R11.4bn)

Hesto’s consolidation boosted revenue and margins, while AutoZone’s recovery phase weighed on aftermarket EBIT. A €20.2m (R413m) fine against Rombat and a R300m capital loss from Hesto’s accounting impacted EPS. Restructuring improved resilience, with OEM margins rising to 7.5–8.5%. Liquidity strengthened through debt refinancing and cash sweep programmes. “Margins have improved through restructuring and optimisation, with profitability increasing as recovery initiatives take hold.” – Board statement. Results due 11 Mar ’26.

Snippets

*Nedbank (NED) confirmed progress on its proposed acquisition of c.66% of NCBA. The Kenyan Capital Markets Authority granted an exemption from making a mandatory takeover offer for 100% of NCBA shares, fulfilling a key condition. Irrevocable undertakings have now risen to 77.54% of NCBA shareholders, strengthening support for the deal. Remaining conditions must still be met before completion.

Nedbank additionally confirmed the Ecobank disposal triggered IFRS recycling of cumulative FX and fair value losses, reducing EPS sharply to 1 625–1 733c (down 52–55% YoY). HEPS remained resilient at 3 667–3 740c (+1–3%), with NAV per share rising 3–5% to 24 760–25 241c. ROE eased slightly to 15.3–15.5%. Results due 3 Mar ’26.

ASP Isotopes (ISO) announced a strategic collaboration between Quantum Leap Energy (QLE) and South Africa’s Necsa to advance High Assay Low Enriched Uranium (HALEU) production. The agreement covers siting, design, and operation of an enrichment facility at Necsa’s Pelindaba site, leveraging QLE’s proprietary enrichment technology and Necsa’s nuclear expertise to meet rising global demand for HALEU fuel for next-generation reactors.

Transpaco (TPC) announced that the Competition Commission has prohibited its proposed acquisition of Premier Plastics Group, which was due to take effect from 1 Jul ’25. The deal involved acquiring all issued shares from the sellers. Transpaco is reviewing the Commission’s response and considering available options, with shareholders to be updated in due course.