Finova Investor Digest

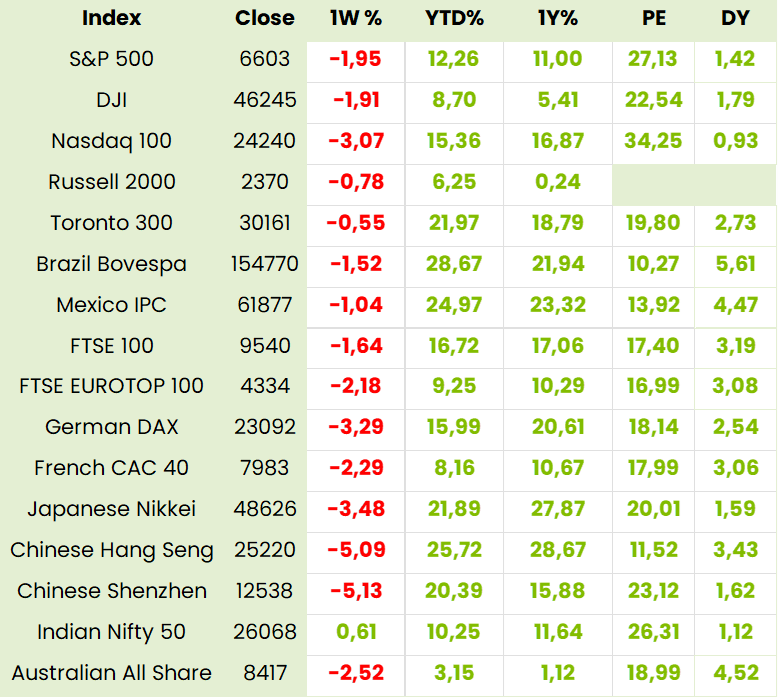

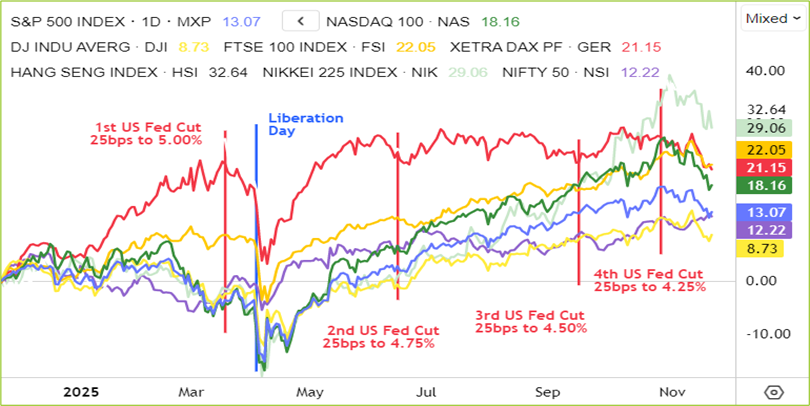

Global Indices, Currencies, Crypto & Commodities

Global Indices 1 year to Date

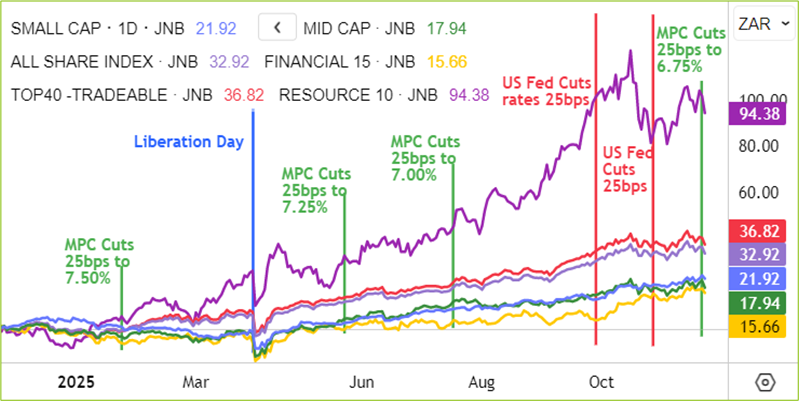

SA Indices

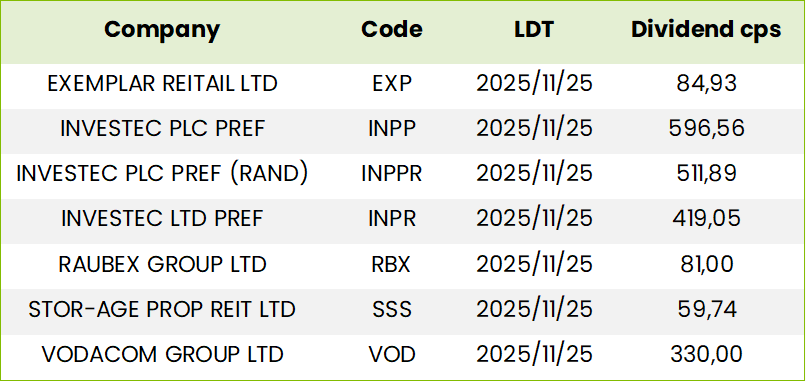

SA Upcoming Indicators & Dividends

SA Equity

WeBuyCars (WBC) Financial Results for FY25 (4493c)

HEPS: 224.6c (>100% from 91.7c FY24)

EPS: 224.1c (>100% from 91.5c FY24)

Revenue: R26.4bn (+13.1% from R23.3bn FY24)

EPS and HEPS surged due to higher volumes, improved net insurance results, lower finance costs, and cost efficiencies. The prior year’s base was depressed by once‑off costs and share issuance impacts, magnifying the rebound.

Expansion remained a strategic priority, with new supermarkets opened in Rustenburg and Vereeniging, adding 850 bays. Pietermaritzburg was relocated to a larger site, while facilities in George, Polokwane, Mbombela, Johannesburg South, Riverhorse Valley, Gqeberha and Germiston were expanded. National capacity rose to 12,911 bays. Monthly sales volumes exceeded 15,000 units in six of the last twelve months, with a record 16,294 units in Nov ’24. Competition intensified from Chinese brands such as GWM, Chery and Omoda, prompting pricing adjustments to maintain liquidity and inventory turns.

Management targets 23,000 vehicles per month by FY28, supported by ongoing investment in infrastructure and digital innovation. New supermarkets in Montana (Pretoria North) and Lansdowne (Cape Town) are scheduled for Nov and Dec ’25, each adding 1,300 bays. Construction has commenced in eMalahleni, with Richards Bay in planning.

Comment: core Headline earnings was R917.6m up 15% and heps was 224.6cps for a trailing PE of 19.5x. As stated above the FY09/24 comparative Heps were distorted by once-off costs and other issues related to the listing and separation from Transaction Capital.

Despite the share price weakness since the trading statement on 28 October, which may have been related to confusion around this (Boxer also had issues on unbundling from Pick n Pay) the stock is priced at least for high teens growth. With new car sales having recovered by 15% after five flat years together with lower interest rates and inflation plus lower priced Chinese and other Asian makes entering and expanding the market, the outlook remains positive. So, whatever the carpark gives, WBC, will take! While legacy cars may lose market share the overall car park will grow and WBC expects its market share to grow from 10.5% to 13% in FY26. Investors can take advantage of the price retracement and safely ACCUMULATE.

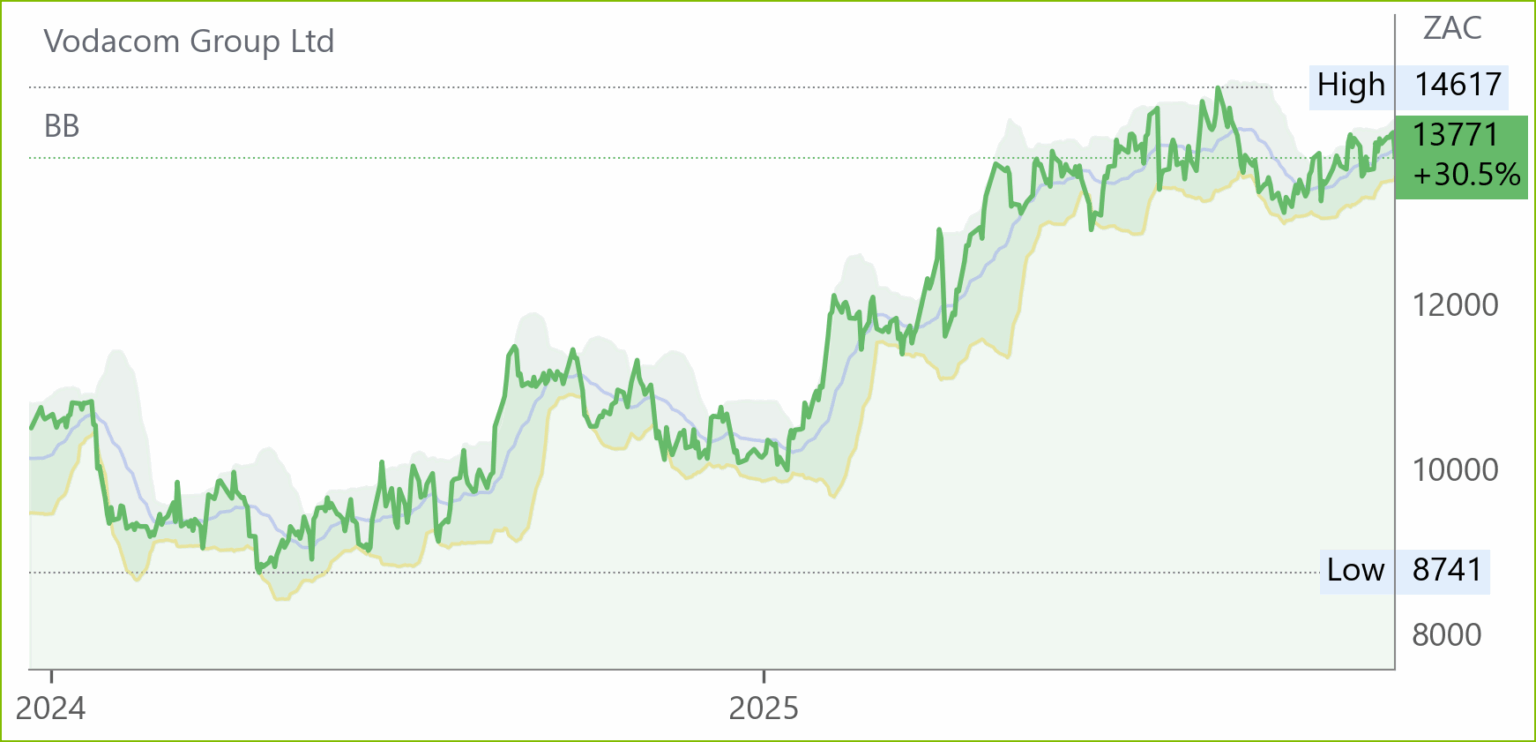

Vodacom (VOD) Interim Results for 6M Sep 25 (13771c)

HEPS: 467cps (↑32.3% from 353cps)

EPS: 472cps (↑33.3% from 354cps)

Revenue: R81.6bn (↑10.9% from R73.5bn)

EBITDA grew 14.7% to R30.5 billion

Interim Dividend: 330cps per share (↑15.8% from R285cps)

Vodacom delivered strong results, with HEPS and EPS up over 30% on service revenue growth, operating leverage, and cost discipline. EBITDA rose nearly 15% as financial services and data monetisation scaled. The group now serves 223.2m customers, including 93.7m financial services users, with M‑Pesa processing US$476.8bn annually. Egypt led with 42.3% service revenue growth, while South Africa remained stable, supported by prepaid LTE and 31.1% data traffic growth. Strategic partnerships with Airtel and Orange enhance rural connectivity, and virtual wheeling supports renewable energy. has partnered with Elon Musk’s Starlink to expand broadband in Africa, integrating satellite backhaul into its mobile network to boost rural coverage and performance which underpins Vision 2030 targets of 260m customers, 120m financial services users, and sustained double‑digit EBITDA growth.

Comment: SA Ebitda at R15,5bn was down 5.3% and comprised c.50% of the R30.5bn total while Egypt’s R9.5bn was 53.7% up and 31% of the total. International (DRC, Mozambique, Tanzania and Lesotho) was R5.9bn, comprised 19% and was up 35%. SA has the likes of Telkom, leveraging its legacy fibre, Cell C as well as 23 MVNOs (Cell C has 13 and MTN 9) nipping at the heels of the first mover giants Vodacom and MTN. Banks and retailers are also into fintech. Safaricom, in which Vodacom and the Kenyan Government each have has 35%, pushed its ebitda up 34% to R14.1bn with Mpesa going from strength to strength. Ethiopia grew customers by 84% to 11.1million and expects ebitda breakeven by FY27 with customers between 15 and 20 million. Bottom line: we believe CEO Joosub’s forecast of double digit ebitda growth is achievable thanks to burgeoning African growth while, at home, he slugs it out with competition but with the fibre enhancing 30% acquisition of Maziv to look forward to. On a 14.5x PE Vodacom can safely be BOUGHT for double digit growth thanks to its powerful African footprint.

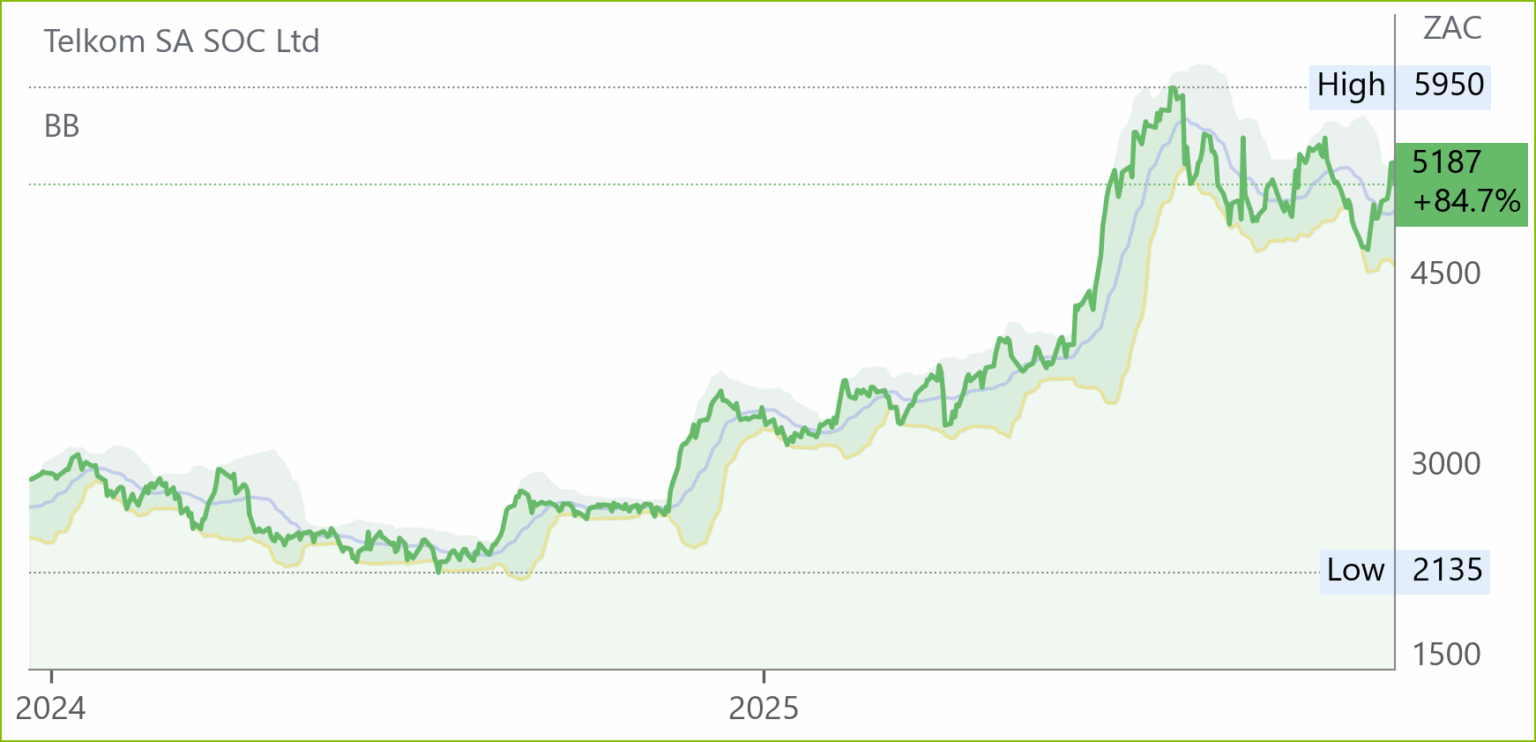

Telkom (TKG) Interim Results for 6M Sep 25 (5187c)

HEPS: 305.6c (+16.4% from 262.6c Sep 24)

EPS: 325.7c (+12.7% from 288.9c Sep 24)

Operating Profit: R1.6bn (+12.9% from R1.4bn Sep 24)

Revenue: R22.1bn (+3.4% from R21.4bn Sep 24)

EBITDA: R6.0bn (+7.4% from R5.6bn Sep 24)

Telkom’s data‑led strategy continued to deliver, with mobile service revenue up 7.9% and the subscriber base expanding 26.7% to 18.5m. Fibre connectivity reached 52%, while cloud services revenue grew 10.4%. EBITDA margins improved across Consumer, Openserve and BCX divisions. The disposal of Swiftnet in Jan ’25 sharpened focus on core operations. Free cash flow remained stable at R724m, reflecting disciplined cash generation.

Management remains cautious given subdued economic growth and intensifying competition in mobile and fibre. Strategic focus will remain on leveraging the extensive fibre footprint and expanding mobile offerings. The OneTelkom approach will sharpen competitiveness, while investment in infrastructure and digital services is expected to sustain momentum into FY26.

Comment: Telkom’s ebitda for 1H26 was up 7.4% while Vodacom’s declined by 5.3% and MTN’s by 4.3% in its 3Q.. In an interview with TechCentral, Telkom Consumer CEO Siya Lunga said the market leading mobile growth, due to Telkom’s data-led strategy, especially in the pre-paid market, was facilitated by its competitiveness at the infrastructure level. This was due to the close relationship between the mobile unit and the Openserve fibre business which provided the fibre backhaul needed to connect Telkom’s radio access network to the core of its network. Rivals such MTN and Vodacom typically lease this infrastructure from fibre network operators Dark Fibre Arica or use microwave. Lunga also pointed to the advantage of the uniformity in Telkom’s network whereas competitors such as Vodacom and MTN have multiple generations of radio access technology including 2G,3G and 5G. Such factors no doubt contributed to Vodacom’s 2022 interest in a bid and, conceivably, could do so again. (In the Vodacom Q & A Joosub said Vodacom was keeping its powder dry in case opportunities presented themselves. None of this means Telkom will enjoy the kind of massive growth that the African footprints of MTN and Vodacom give them but there is value and it certainly priced at least for a HOLD.

Lewis (LEW) Interim Results for 6M Sep 25 (8300c)

HEPS: 648c (+16.8% from 555c)

EPS: 619c (+13.8% from 544c)

Operating Profit: R522m (+21.4% from R430m)

Revenue: R4.8bn (+11.3% from R4.4bn)

Gross Profit: R2.0bn (+11.0% from R1.8bn)

Dividend: 337c interim dividend (+12.3% YoY)

Operating profit surged 21.4% due to margin expansion and strong debtor portfolio quality. HEPS rose 16.8% as share repurchases amplified earnings leverage. Revenue grew 11.3% on higher merchandise and ancillary income. Gross profit strengthened 11.0% as credit sales growth lifted insurance and interest income.

Store footprint expanded to 958 outlets, with 40 new openings in H1, including 28 Real Beds stores. A further 15–20 stores are targeted for H2, mainly in specialist bedding brands.

Specialty brands UFO, Bedzone and Real Beds grew sales 9.1%, while traditional retail rose 6.4%. Comparable store sales advanced 2.3%. International stores, now 15.1% of the base, delivered 7.7% growth. Credit sales rose 8.0%, accounting for 70.3% of merchandise sales, while cash sales increased 3.7%. Strict credit criteria saw application decline rates at 41.2%. Debtors book grew 14.0% to R8.5bn, with satisfactory paying customers up to 82.7%.

Comment: on a trailing PE of 5.4x Lewis, the price of which has been side tracking for a year, is way undervalued and we maintain our BUY recommendation. After maintaining steady growth during the stagnant Twenties, it is anticipating meaningful recovery in consumer spending in the next few years and therefore continuing expansion

as its stores tally approaches the 1000 mark. Lower interest rates, restrained inflation plus the 1.8% GDP growth forecast in the MTBS, let alone real growth if only a modicum of the much talked policy reforms are implemented, will make for much stronger growth as consumers wallets extend beyond food and clothing. Lewis is engaging with the Competition Commission to oppose the sale of Shoprite’s furniture business to Pepkor on the basis that this will result in Shoprite having more than 50% of the market which will be bad for consumers as well as the manufacturing industry. Either way we will maintain our recommendation; it is just that Lewis would do even better if it succeeds in thwarting the deal.

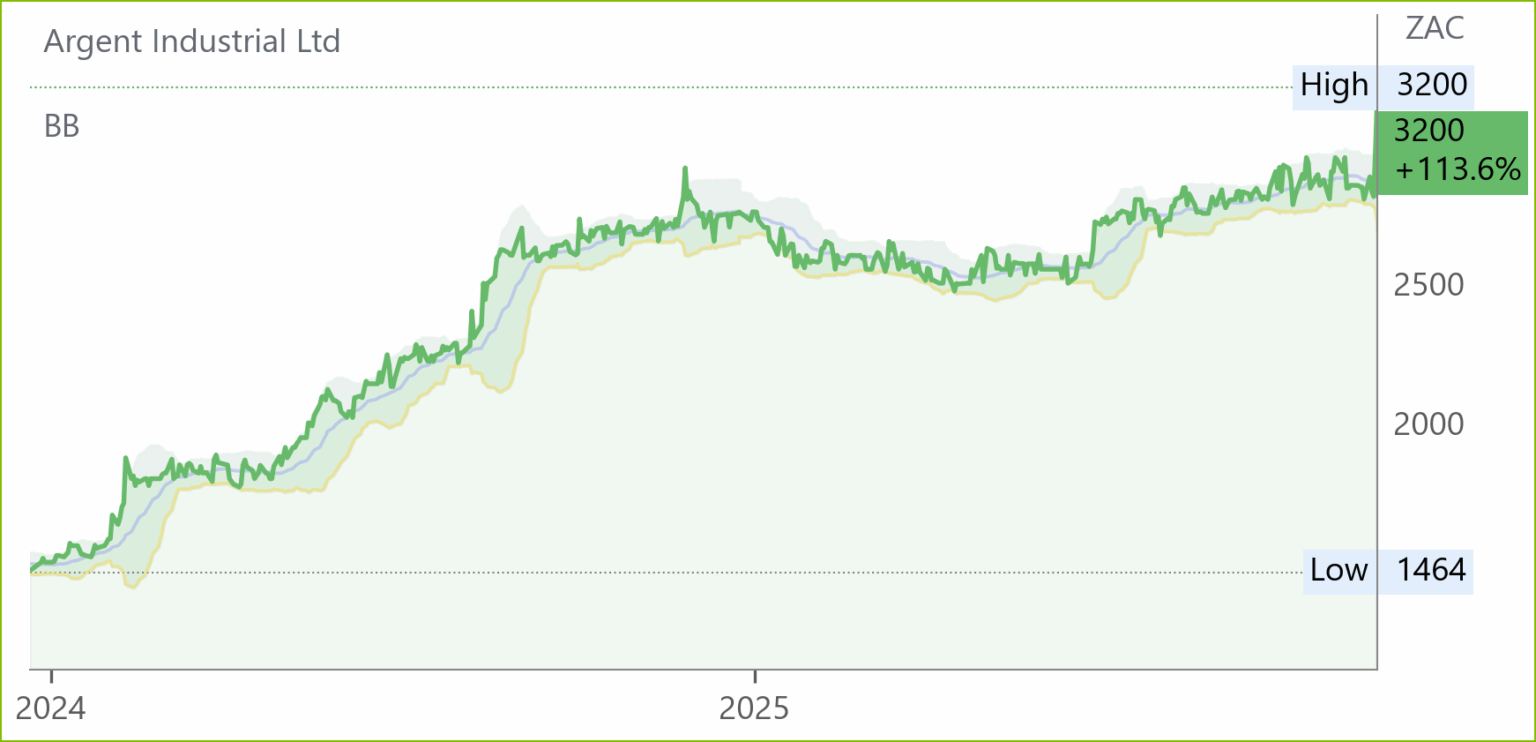

Argent (ART) Interim Results for 6M Sep 25 (3200c)

HEPS: 261.7c (+13.3% from 231.0c)

EPS: 263.3c (+13.7% from 231.7c)

Operating Profit: R195.4m (+11.4% from R175.4m)

Revenue: R1.42bn (+12.4% from R1.26bn)

EBITDA: R229.8m (+13.2% from R203.0m)

Dividend: 67.0c interim dividend (+11.7% YoY)

Argent delivered solid interim growth with HEPS up 13.3% and EPS rising 13.7%, supported by stronger trading volumes and improved margins. Revenue advanced 12.4% to R1.42bn, while operating profit grew 11.4% to R195.4m. EBITDA increased 13.2% to R229.8m, reflecting efficiency gains and disciplined cost control. Shareholders’ funds rose 10.7% to R2.0bn, with NAV per share up 11.9% to 3654.9c, strengthening the balance sheet. Chairperson noted: “We are committed to delivering sustainable shareholder value through disciplined capital allocation and operational excellence.” – Chairperson. Management expects continued demand from construction and manufacturing sectors, offsetting inflationary pressures on raw materials. Comment: but for the fact that it has industrial groups in the US, UK and Canada as well as SA, Argent could easily be mistaken for a classic SA Inc industrial stock like, say Hudaco. So, while the interims Heps growth of 13.3% is below the 4 year FYs 21-25 CAGR of 22.6%, CEO Treve Hendry’s bullish outlook “Our international order book remains strong. Domestic operations are robust with potential for further recovery. Attractive opportunities exist to allocate capital to strategic acquisitions further enhancing the group’s footprint. Argent Industrial is therefore well-positioned to deliver satisfactory results in FY2026 and into the long-term” points to a stock that has delivered consistently in the past and is undervalued now on a 6x trailing PE.

Coronation (CML) Financial Results for FY25 (4707c)

HEPS: 474.3c (‑25% from 630.5c FY24)

EPS: 474.3c (‑25% from 630.5c FY24)

Revenue: R4.29bn (+10% from R3.91bn FY24

Dividend: 254cps (Final dividend, +11% YoY)

HEPS and EPS fell 25% due to the once‑off reversal of a SARS tax provision in FY24, which had inflated prior earnings. Excluding this, fund management earnings per share rose 12% YoY, reflecting stronger operating performance.

Coronation maintained resilience in a challenging environment, with assets under management supported by positive net flows and market recovery. The conclusion of the SARS matter removed a significant overhang, restoring clarity on tax obligations. B‑BBEE initiatives advanced, with subscription shares issued to trusts attracting a 10% trickle dividend. Management emphasised its client‑centric approach, with investment performance remaining competitive across flagship funds. KPMG provided an unmodified review conclusion, reinforcing confidence in governance and reporting standards.

Management remains focused on delivering sustainable long‑term value through disciplined investment processes and cost control. Dividend policy reflects confidence in cash generation.

Ninety One (NY1) Interim Results for 6M Sep 25 (4627c)

HEPS: 8.9p (+14% from 7.8p Sep 24)

EPS: 8.9p (+14% from 7.8p Sep 24)

Operating Profit: £102.2m (+10% from £93.3m Sep 24)

Dividend: 6.0pps (Interim dividend, +11% YoY)

AUM rose 19% YoY to £152.1bn, supported by £4.3bn net inflows, including £1.9bn from Sanlam UK. Staff shareholding increased to 32.7%, reinforcing alignment with clients. The Sanlam relationship is delivering early benefits, with the UK transaction completed in Jun ’25 and South Africa to follow. Competitive long‑term investment performance and technology platform investment strengthened positioning. “We see early evidence of a demand recovery for emerging markets and differentiated active investment management. We are well positioned for this.” – Hendrik du Toit, CEO.

Investec (INP) Interim Results for 6M Sep 25 (12200c)

HEPS: 36.7p (+0.3% from 36.6p)

EPS: 37.8p (+3.3% from 36.6p)

Operating Profit: £468.1m (-1.4% from £474.7m)

Revenue: £1.10bn (-0.6% from £1.10bn)

Dividend: 17.5p interim dividend (+6.1% YoY)

Investec reported EPS up 3.3% on stronger fee income and lower impairments, while HEPS was flat amid margin pressure from lower rates. Operating profit fell 1.4% as trading and investment income softened, with revenue down 0.6% on weaker net interest income, partly offset by client activity and annuity fees. Funds under management rose to £26.5bn in Southern Africa, with Rathbones contributing £113bn. Deposits grew 3.6% to £41.9bn and core loans advanced 6.1% to £33.7bn. Credit quality improved (CLR 35bps). Capital strength remained robust (CET1 SA 14.6%, UK 12.7%). Management guides H2 broadly in line, supported by book growth.

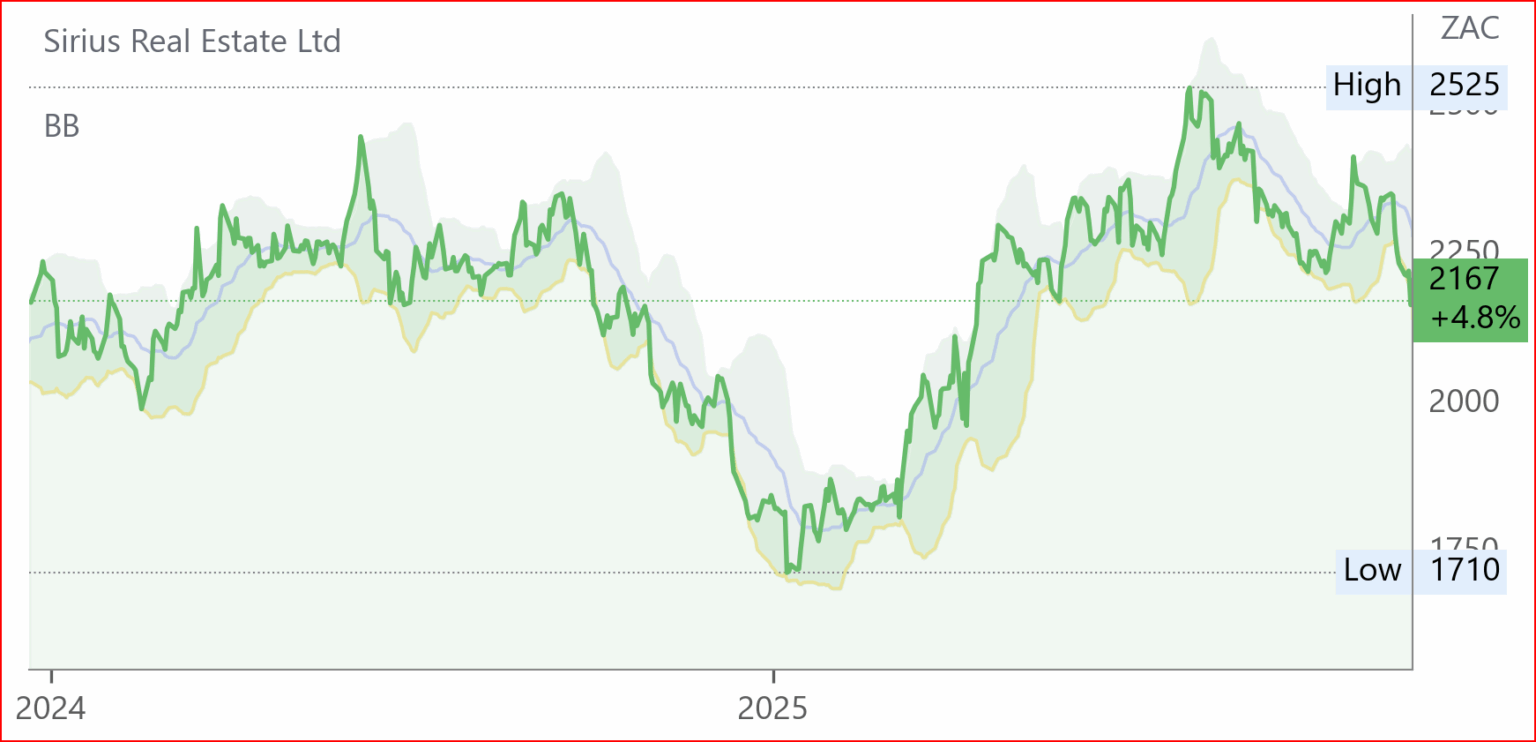

Sirius Real Estate (SRE) Interim Results for 6M Sep 25 (2167c)

HEPS: 2.84c (‑28.8% from 3.99c Sep 24)

EPS: 5.77c (+47.2% from 3.92c Sep 24)

Revenue (Rent Roll): €242.5m (+15.2% from €210.5m Sep 24)

EBITDA / FFO (Funds from Operations): €64.7m (+6.6% from €60.7m Sep 24)

Dividend: 3.18cps (Interim dividend, +4% YoY)

Sirius delivered a mixed interim performance, with EPS up 47.2% on profit after tax growth, valuation gains and deferred tax releases, while HEPS fell 28.8% due to €14.2m foreign currency translation losses on sterling reserves. Portfolio expansion included €295m in acquisitions, notably Hartlebury, strengthening UK BizSpace. Asset management initiatives added €14.4m in valuation uplifts, with tenant renewals and capex generating strong three‑year returns. Rent roll rose 15.2% YoY, supported by active leasing. Fitch reaffirmed a BBB rating with Stable Outlook. Management expects acquisitions to drive FFO and earnings growth, prioritising recycling mature assets into value‑add opportunities in Germany.

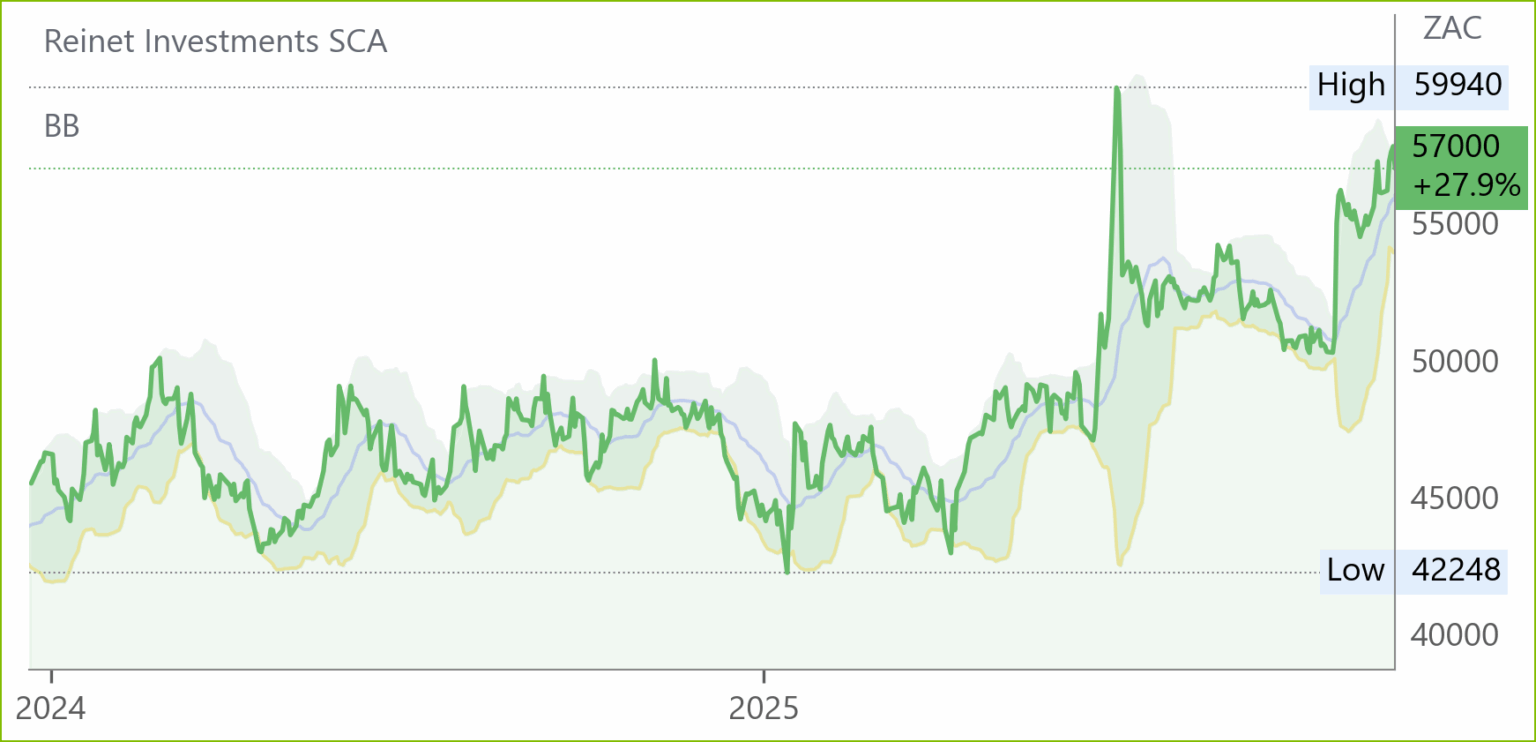

Reinet Investments (RNI) Results for 6M Sep 25 (57000c)

Dividend: 37cps (Interim dividend, paid Sep ’25)

NAV decreased 3.7% to €6.7bn from €6.9bn at Mar ’25, driven by lower valuations in certain investments and foreign exchange impacts.

Reinet reached agreement to sell its entire holding in Pension Insurance Corporation to Athora Holding, expected to close in 2026. Ordinary and special dividends of €303m were received from Pension Insurance Corporation during the period. Commitments of €298m were made to new and existing investments, with €7m funded. The dividend of €0.37 per share, totalling €67m, was paid in Sep ’25. Reinet’s NAV has compounded at 8.6% per annum since Mar ’09, including dividends.

The sale of Pension Insurance Corporation will provide liquidity for redeployment into new opportunities. The company remains positioned to benefit from diversified exposure across asset classes, with strong cash inflows supporting future commitments.

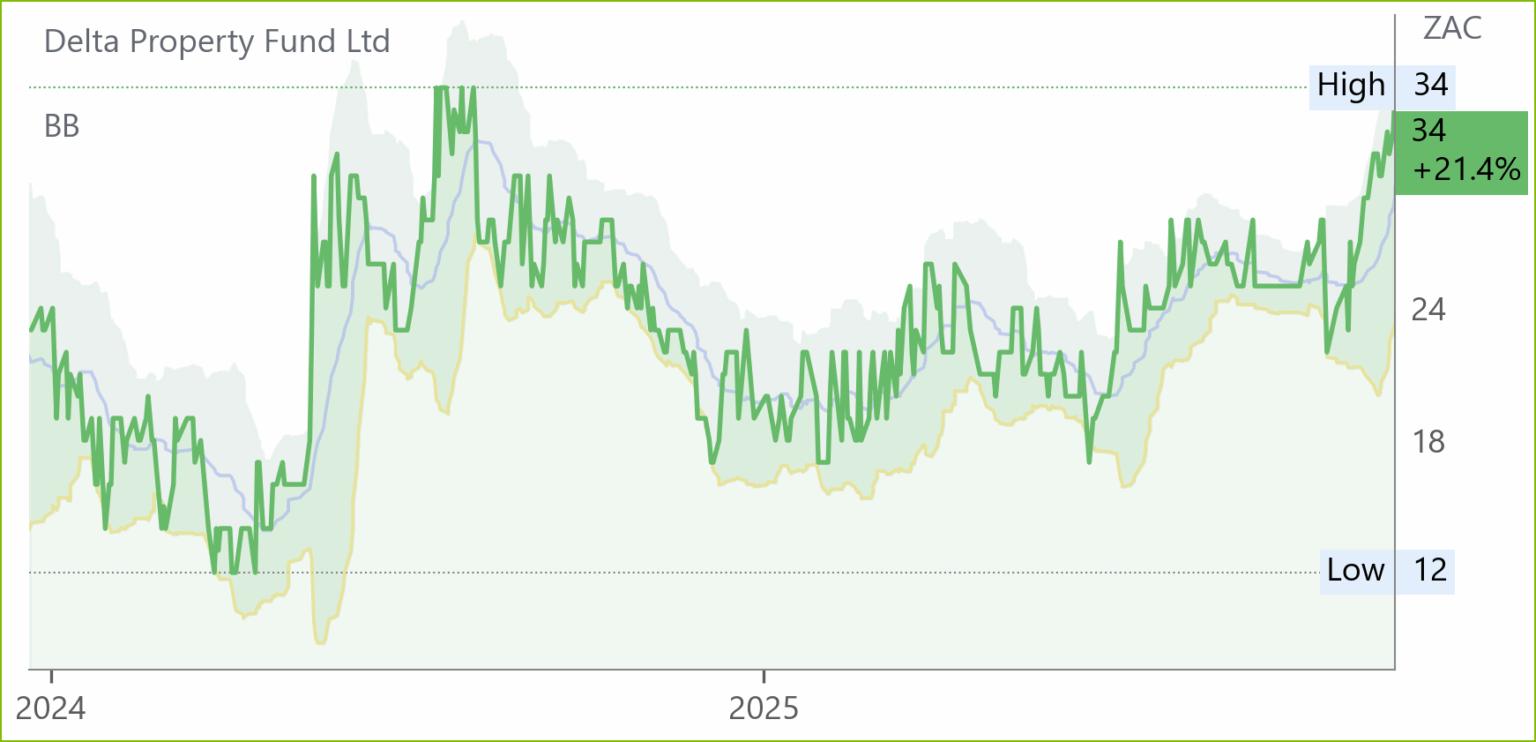

Delta (DLT) Interim Results for 6M Aug 25 (34c)

HEPS: 7.5c (+47.1% from 5.1c)

EPS: 7.1c (+73.2% from 4.1c)

Operating Profit: R50.7m (+71.9% from R29.5m)

Revenue: R578.2m (-0.9% from R583.7m)

Dividend: Nil interim dividend (HY24: Nil)

Delta delivered a stronger interim performance with EPS up 73.2% and HEPS rising 47.1%, driven by lower finance costs, tighter expense control and disposals of non-core assets. Operating profit surged 71.9% despite a slight 0.9% revenue decline, reflecting improved collections and reduced vacancies. Rental collections improved to 100%, vacancies fell to 29.7%, and R161m of properties were sold. Debt reduced to R3.7bn, lowering finance costs and strengthening liquidity. CEO Sibongile Masinga noted: “We remain focused on executing our strategic objectives, strengthening the balance sheet, and reducing vacancies.”- Sibongile Masinga, CEO. Results webcast scheduled for 25 Nov ’25.

Operating Updates & Trading Statements

Naspers (NPN) Trading Statement for 6M Sep 25 (116105c)

HEPS: 14 941c (↑20.8%–27.8% from 12 041c Sep 24)

EPS: 5 849c (↑30.2%–37.2% from 4 870c Sep 24)

Naspers delivered strong growth in consolidated ecommerce and equity-accounted investments, notably Tencent, with core headline earnings boosted by the exclusion of foreign currency translation losses. A five-for-one share split in Oct ’25 enhanced comparability, while the ecosystem expanded to nearly 100 companies serving 2 billion consumers worldwide. Management emphasised profitable growth and long-term foundations, supported by discipline, innovation and people focus. Chair Koos Bekker stated: “We are building the foundations for continued growth over a long period, serving billions of consumers worldwide and reinforcing our culture of discipline and innovation.”

Results due 24 Nov ’25.

Prosus (PRX) Trading Statement for 6M Sep 25 (113335c)

HEPS: 2 484c (↑20.1%–28.5% from 2 067c Sep 24)

EPS: 3 297c (↑28.1%–37.0% from 2 574c Sep 24)

Prosus reported strong growth in consolidated ecommerce businesses and equity-accounted investments, particularly Tencent, driving headline and core headline earnings higher. Core headline earnings benefited from the exclusion of foreign currency translation losses, while headline earnings included these effects. A gain on the sale of Tencent shares related to the share repurchase programme boosted EPS but was excluded from headline measures. The group emphasised profitable growth in the first half of FY26, supported by “The Prosus Way” culture of discipline, innovation and people focus.

Results due 24 Nov ’25.

MTN (MTN) Quarterly Update for 9M Sep 25 (17500c)

Revenue: R27.9bn capex deployed.

Group service revenue +22.6% YoY (Q3 +23.0%)

Group margin 45.0% (+6.7pp)

MTN Nigeria EPS and EBITDA surged over 100% due to stronger naira, price adjustments, higher smartphone penetration, and revised tower lease agreements. This turnaround restored positive retained earnings and net equity, enabling dividend resumption.

MTN crossed 300m customers across 16 markets, with active data users up 9.1% to 165.8m and MoMo monthly active users up 5.3% to 64.3m. Data traffic rose 26.6% to 17,876PB, while fintech transaction value grew 38% to US$342.3bn. Expansion included new fibre corridors and a greenfield data centre programme under Bayobab. Fitch reaffirmed strong liquidity, with net debt/EBITDA reduced to 0.4x. A landmark partnership with Microsoft will roll out AI‑powered learning tools across Africa from early 2026.

Management remains focused on prepaid recovery in South Africa, sustaining momentum in Nigeria and Ghana, and scaling fintech. Capex guidance for FY25 remains R33–38bn, with medium‑term targets unchanged.

Momentum Metropolitan (MTM) Operating Update for 3M Sep 25 (3601c)

Operating Profit: Normalised headline earnings R1.76bn (+N/A vs R1.07bn Sep 24)

Revenue: PVNBP R22.4bn (+8% from R20.6bn Sep 24)

Normalised headline earnings rose 64% YoY, supported by disciplined execution, positive market variances, and excellent short‑term insurance underwriting. Value of new business fell 26% to R146m, mainly due to lower life annuity sales in Momentum Investments, partially offset by improvements in other segments.

Momentum Retail delivered NHE of R254m, aided by contractual service margin releases and positive mortality experience. Momentum Investments achieved NHE of R310m, though VNB declined due to lower‑margin annuity mix. Metropolitan Life reported NHE of R248m with improved persistency and mortality experience. Momentum Corporate grew NHE to R427m, supported by group risk and FundsAtWork. Guardrisk and Momentum Insure delivered strong underwriting profits, while Momentum Health grew membership 6% to 1.35m. Momentum Africa exited Ghana in Sep ’25, boosting focus on Namibia, Lesotho and Botswana.

Old Mutual (OMU) Voluntary Operating Update for 9M Sep 25 (1365c)

Loans and advances declined by more than 100% YoY due to the sale of underperforming loan books and stricter credit criteria, alongside competitive buy‑offs in East Africa. Other metrics showed marginal changes, with gross written premiums up 5% and net client cash flow broadly flat.

Gross flows were stable at R169bn, with strong inflows in Namibia, Uganda, Kenya and Malawi, countered by weaker Old Mutual Investments inflows. Net client cash flow was impacted by R7.8bn offshore indexation outflows. Gross written premiums grew 5%, driven by Old Mutual Insure and ONE Financial Services Holdings, while Africa Regions faced lower renewals and discontinued Nigeria operations.

City Lodge (CLH) Operational Update for 4M Oct 25 (500c)

City Lodge delivered stronger trading in the first four months of FY26, with occupancy up 4.6 points to 62.0% and November occupancy rising 8.0 points to 65.0%. Average room rates tracked inflation, while food and beverage revenue grew 16% and surged 32% in November. Demand peaked at 90.7% occupancy during the G20 summit. Regional performance was mixed, with Namibia buoyant, Mozambique improving despite added capacity, and Botswana showing early recovery signs. Refurbishment and IT upgrades are underway, supported by a strong balance sheet and R144.9m share buyback. Management expects festive season demand to sustain momentum into 2026.

Life Healthcare (LHC) Trading Statement for FY25 (1199c)

HEPS: Expected +97.5c to +102.0c (vs 91.1c FY24, +7% to +12%)

EPS: Expected +92.2c to +96.8c (vs 92.2c FY24, flat to +5%)

Revenue: Growth +5.5% to +6.5% YoY

EBITDA: Normalised +4.5% to +5.0% YoY (like‑for‑like +6.6% to +7.1%)

Earnings were impacted by the R2.9bn fair value adjustment to the Piramal liability linked to the LMI disposal, which reduced EPS and HEPS. Excluding this, pro forma EPS rose 7% to 12%, reflecting stronger acute and complementary services performance.

Acute business revenue grew ~5%, with occupancy at 69.7%. Complementary services revenue surged 24.7% on acquisitions, while healthcare services declined 7.5% after losing government contracts. Renal dialysis margins diluted overall profitability, though improvements were made in H2. Impairments of ~R210m were recognised for underperforming units. Results due 27 Nov ’25.

NEPI Rockcastle (NRP) Business Update for 9M Sep 25 (10000c)

Net operating income €461.3m (+12.3% YoY; LFL +4.4%)

NOI rose 12.3% YoY, supported by rental uplifts, indexation, renewable energy revenue (+23%), and disciplined cost control.

Tenant sales grew 3.5% LFL, while footfall dipped 0.6%. Average spend per visitor rose 9% overall, aided by Polish acquisitions. Occupancy cost ratio fell to 12.7%, with retail vacancy at 1.6% and collections at 99%. Leasing momentum remained strong, with 1,098 leases signed YTD, including Primark, Nike and Sports Direct. A €500m green bond issue was oversubscribed, strengthening liquidity. Development pipeline exceeds €870m, including major projects in Romania, Poland, Hungary and Bulgaria. First Romanian PV project (54MW) completed, with further renewable rollouts underway.

Management reaffirmed FY25 guidance for distributable earnings per share growth of 2.5–3% YoY, maintaining a 90% payout ratio. Liquidity remains robust with €421m cash and €690m undrawn facilities.

Snippets

Jubilee (JBL) secured Competition Tribunal approval for the sale of its South African chrome and PGM operations to One Chrome, with Reserve Bank and audit clearance pending. Completion is expected by end‑2025, after which focus shifts solely to Zambian copper projects while retaining Tjate platinum investment. Termination rights apply if conditions are unmet by 31 Dec ’25.

Pick n Pay (PIK) founding Ackerman family sold 64m shares at R25.50 each in an accelerated bookbuild, raising R1.6bn. Their voting interest fell from 49% to 36.8%, ending majority control but retaining anchor shareholder status. Gareth Ackerman will retire as chair after 14 years. The sale supports debt reduction and turnaround efforts