A hybrid retirement solution combines two well know post-retirement vehicles (the life annuity and the living annuity) to hedge against risks, such as longevity, volatility, inflation and bequest risk. While a hybrid solution can reduce the impact of some of these risks, they still exist.

Last week’s Finova Insight unpacked these retirement risks in detail, click here to read more.

Fortunately, there are alternative hybrid solutions that many financial advisors overlook. Instead of relying solely on a life annuity which comes with limitations, a high quality bond allocation within a living annuity can replicate the structure of a hybrid solution, providing guaranteed income for a stress free retirement, and knowing your loved ones are taken care of.

Why Choose Bonds over a Life Annuity?

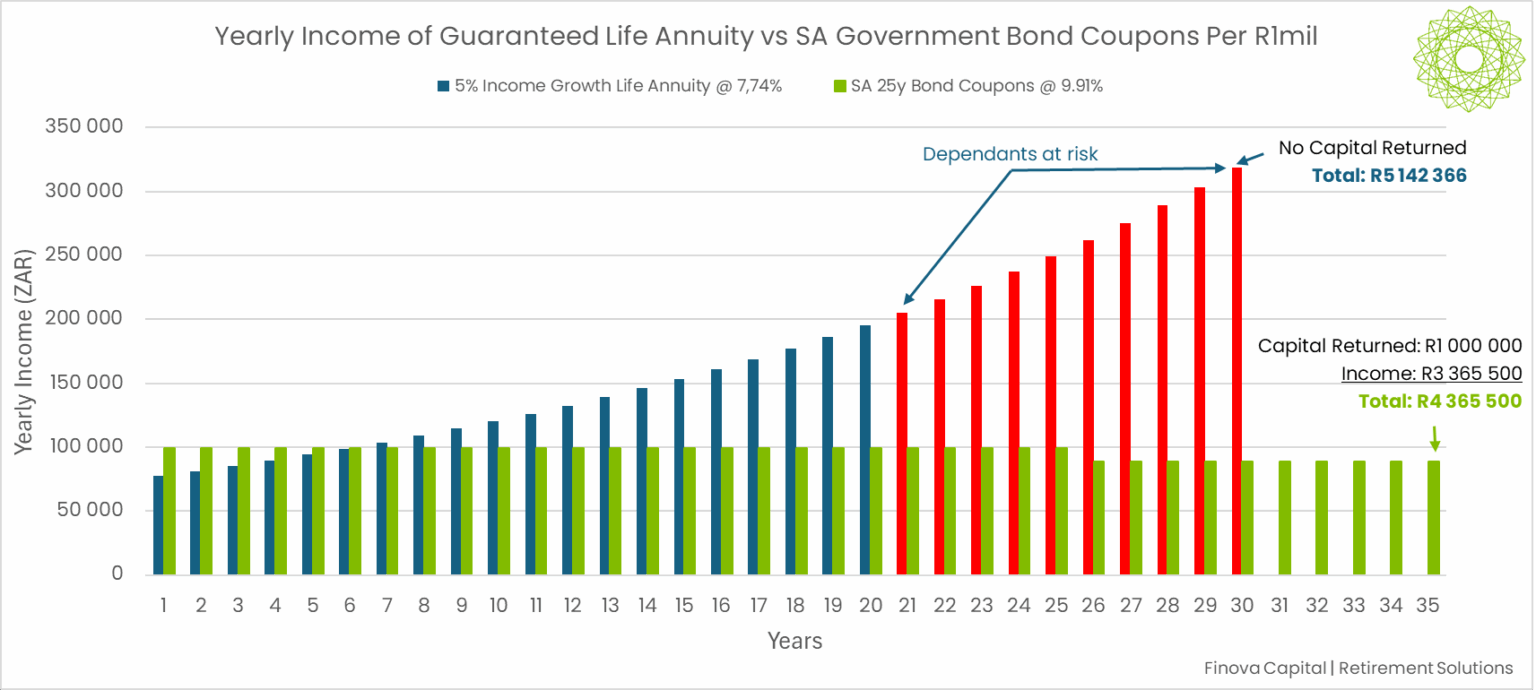

The chart below compares the annual income from a 20-year Guaranteed Life Annuity with 5% income growth (at 7.74%) to a 20-year South African Government Bond (at 9.%). Assuming retirement at 65 and a life expectancy of 95, the life annuity provides higher overall income, but after 20 years, longevity risk arises because if you pass hereafter, your dependants will not be entitled to any income. The bond, by contrast, returns your original investment at maturity, which can be reinvested into a new 5 or 10-year bond if you live beyond the initial guarantee, illustrating how it mitigates longevity risk.

The appeal of a life annuity lies in its guaranteed income for life, providing certainty and stability for retirees who value security over flexibility. However, most retirees have beneficiaries, a spouse, children or dependants, making bequest risk a key concern. If you pass away shortly after retirement, your income stops immediately and no capital passes to your heirs.

A bond allocation within a living annuity offers a compelling alternative. Quality bonds can replicate the income profile of a life annuity while returning capital at maturity. If you outlive the term, you can reinvest and continue drawing income. When you pass, the remaining capital stays within the policy and transfers to beneficiaries tax-free.

Why It’s Not One-Size-Fits All

The hybrid approach provides a framework for advisors, not a formula. The right balance between guaranteed and market-linked income depends on each retiree’s situation, including marital status, dependants, expenses, and other income sources.

Consider three examples:

- Single retiree with no dependants: Faces high longevity risk. A greater, or entire allocation to guaranteed fixed or escalating income is typically best, prioritising stability and with minimal management.

- Married couple with children: Would likely prefer a balance between a bond allocation and market-linked income. This provides them stability while protecting their dependants in a tax efficient structure.

- High net worth retiree: Typically has existing investments, would benefit from a smaller allocation to fixed income to cover core expenses, and a larger allocation to market-linked income to optimise estate planning.

Even within these examples, variables such as capital commitment, number of dependants and life expectancy all weigh on the optimal allocation.

Understanding Specific Risks

Longevity, volatility, inflation and bequest risks remain central to retirement planning.

A bond allocation within a living annuity alters this risk profile slightly, bequest risk is mitigated, but longevity and interest rate risk become more relevant. In a rising yield environment, selling bonds before maturity can result in capital losses, and when yields fall, reinvestment risk emerges as future income may decline.

These same movements also create opportunity. Falling yields generate capital gains, while rising yields allow investors to lock in higher future income. This is where timing, duration management and professional oversight add meaningful value.

Liquidity and emergency planning are equally important. A combination of short and long-term bonds can mitigate these risks. Shorter maturities provide access to funds for healthcare or unexpected expenses, while longer maturities secure consistent income. This balance ensures flexibility and stability that a pure life annuity cannot offer.

Inflation risk, though universal, can be mitigated with inflation-linked bonds that preserve purchasing power and maintain real income over time.

How Finova’s Approach Sets Us Apart

Retirement success depends less on which product you choose and more on how it is structured to meet your needs. A hybrid approach is not a static product but a dynamic framework that evolves with your life and the market environment.

Finova’s retirement specialists design personalised retirement solutions, not off-the-shelf annuities. Each plan begins with a detailed review of your lifestyle, liabilities, dependants and time horizon.

Whatever your objectives, whether guaranteed income, flexibility, or legacy planning, the key to a successful retirement is a clear understanding of your position and the guidance of professionals who do the heavy lifting.

If you have not modelled your retirement yet, now is the time. Let Finova’s retirement team help you quantify your income potential, assess longevity risk, and optimise what you can leave behind.

Book a free “Retirement Consultation” with one of our retirement specialists to secure your retirement strategy built around you, not a product.

Sources:

MoneyWeb, Glacier, SA Economics